Tariffs - SWAP-bfz

advertisement

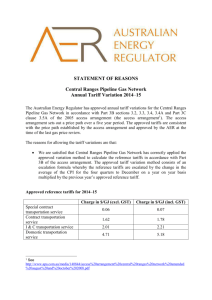

COST REFLECTIVE TARIFFS: A Prerequisite For Financial Sustainability of a Water Utility Innovative Water Sector financing .7th – 12th November 2011, Mombasa Kenya. Eng. PETER NJAGGAH WASREB, Kenya Contents Why the need for a water tariff? Tariff Types Setting a water tariff Tariff design Water an economic or financial good?. Implementation and Monitoring. Conclusion. Water tarriff : a contraversial Topic? Why Water Tariff? Important economic instrument for: improving water use efficiency, enhancing social equity securing financial sustainability of WSPs. Sustainable Water Management Price < Costs? • What effects? – 1 Quality will fall – 2 Not sustainable – 3 Kills entrepreneurship – 4 Affects other projects – 5 Demand too high Basic balance: Sustainability Levels of service Quantity, Quality Income Infrastructure Tariffs Subsidy O&M Capital 6 Tariffs = Opex + Dep(CapManex)+ Cost of Capital Operating Expenditure – Labour – Chemicals – Power – Materials – Equipment – Overheads • Communications Capital Mtce Expenditure – Depreciation • Above ground – Infrastructure Renewals Cost of Capital • Loans -> Interest • Equity -> Dividends: Incentive & Rewards for risk - ‘profit’ KENYAN WATER SERVICES SECTORTariffs Types Wasreb recognizes that WSP differ by category and size, and has developed different requirements accordingly. Type 1: Full coverage of Operations and Maintenance costs is still not achieved. Type 2: Full coverage of Operations and Maintenance cost achieved, but repayment of debts is pending. Type 3: O&M costs are covered between 100% and 150% and repayment of debts is achieved or ongoing. Options for Calculating Tariffs • Leave tariffs as they are, hope for the best • Aim for full recovery of operation and maintenance costs. Set a tariff to recover operation and maintenance costs plus depreciation (capital maintenance) • • Set tariffs to recover operation and maintenance costs plus full amortization (interest payments and repayment of ‘principal’) of the capital costs . The Water Utility Example BALANCE SHEET INCOME AND EXPENDITURE ACCOUNT ASSETS EMPLOYED Fixed Assets Development Expenditure 2002 '000s OPERATING INCOME Sale of Water Miscellaneous OPERATING EXPENSES Chemicals Divisional adminstration Electricity Maintenance Salaries and wages OPERATING SURPLUS Depreciation 2001 '000s 5903 137 6040 4506 131 4637 33 644 455 175 564 1871 31 455 448 119 464 1517 4169 3120 933 588 FINANCE CHARGES Interest payable Less: interest receivables 2212 -404 1686 -461 SURPLUS FOR THE YEAR 1428 1307 Total Tariffs (should) = Opex + CURRENT ASSETS Stores Accounts receivables Consumer Divisional Other Short term deposits Bank and cash balances CURRENT LIABILITIES Accounts payable General Divisional HQ Interest payable Loan repayments due within one year Consumer deposits Dep (CapManex) + Cost of Capital NET CURRENT ASSETS NET ASSETS FINANCED BY Consumer Capital Contributions General Reserve Capital Reserve Long Term Loans 2002 '000s 2001 '000s 30367 27559 706 123 122 578 433 1318 4126 973 7551 352 440 932 4544 172 6562 1872 1135 737 1314 16 5074 1972 729 690 1097 14 4502 2477 32844 2060 29619 893 2516 3563 6972 892 1927 3137 5956 25872 32844 24369 30325 Tariff Objective(1) Tariffs should be: • Conserving – Structure of tariff should influence consumption to the extent that customers will purchase enough to satisfy their neds without being wasteful • Adequate – A level of resources must be produced which will enable financial commitments to be met Tariff objective(2) • Fair – This level of revenue must be allocated between consumer groups in a fair and equitable manner having particular regard to the needs of the poorer members of the community • Enforceable and Simple – The tariff should be simple to administer and enforce and easy for customers to understand CAFES Tariffs – The Practice • Flat rates/area charges/property charges • Metering (metering costs - 25%?) Fixed Charges ? • Block Pricing (increasing/decreasing) • Prices for the poor: – – – – – – Lifeline blocks (15m3?6m3?) Free Allowances (South Africa) Cross Subsidies (10 times ? 20 times?) Multi-users losing out Paying at standposts/kiosks Direct subsidies (Chile) Water tariffs design(1). Is water an economic or financial good? • The Dublin Declaration said that ‘water is an ‘economic good’ – not a financial good • How should we treat it as an ‘economic good’? • Does it relate to a ‘financial good’ ? Is water an economic or financial good? • Financial analysis details what has to be paid for in cash terms by a sponsoring agency, government department, customer, consumer or householder for any project and for subsequent outputs or services. • Economic analysis describes the total resource cost of a project to a country or region including potentially under-valued items such as voluntary labour and pollution Profile of Water Tariff in Kenya Average Tariff and Lowest Block Tariff per WSP Category Tariffs Bigger WSPs tend to have lower tariff due to: Lower operational costs. 129 140 120 100 80 60 40 20 0 111 83 78 64 40 Average Tariff Lowest Block tariff Very Large Medium Small and Large Large customer base leading to cross subsidy, hence ability to address needs of the poor(lower block tariffs) without compromising their commercial viability. CONCLUSIONCost Reflective Tariff is a Prerequisite for: Financial Sustainability of a WSP leading to improved and efficient service delivery. Making access to drinking water affordable for different income groups.- tariffs should not be too high to drive consumers to unsafe alternatives . Sending appropriate price signals to users about the relationship between water use and water scarcity; Acessing Market finance 19 THANK YOU FOR YOUR ATTENTION