Employee Ownership - Scottish Enterprise

advertisement

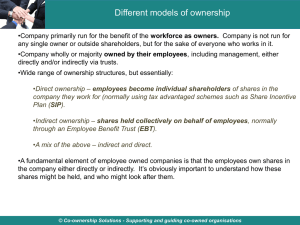

Expert Briefing Session Employee Buyouts - Ewan Hall, Baxendale 4 February 2014 Employee Buyouts Objective • Understand the key decisions and elements involved in a transition to employee ownership • No two are alike, but there are common themes Ask questions at any time! 3 Ownership Agenda / What’s Happening • Baxendale • Why an Employee Ownership Transition? • Differences from a “conventional” exit • Structuring the Deal: Price / Funding / Protections / Taxation / Leadership / Engagement • Structuring the Post-Transition: Ownership / Governance / Engagement and Communication • The Future • Final Thoughts 4 Ownership Baxendale • Employee ownership specialists • Advise on alternative ownership models • 13 year track record of offering advice, funding and support • Worked with more than 80 private and public sector organisations – often with their existing advisers • Sold domestic boiler company to employees in 1983 • Believe that employees should share in wealth they have created, have a real voice in company 5 Ownership Sample Structure of a Transition • The parties: Company: the organisation that is to transfer into employee ownership. Owner(s): who own the company at the outset. Employees: who may acquire some or all of the shares. Employee Benefit Trust: which may acquire some or all of the shares 6 Ownership Sample Structure of a Transition • The parties cont.: Share Incentive Plan: where employees are to acquire shares directly, this is often done through a SIP. Bank / Funder: funds the transition, usually secured on the assets of the company (may be the owner). 7 Ownership Parties 8 Ownership Funding 9 Ownership Payment to Owner and Share Transfer 10 Ownership Why an Employee Ownership Transition? 1. Employee Driven Transition 2. Owner Driven Transition 3. Hybrid (e.g. owner’s vision, but process driven by employees) • • • • 11 Reasons may influence structure Role of Advisers Role of Co-operative Development Scotland Role of Sector Ownership Why Employee Ownership? • The Owners: 12 Control exit Succession Legacy Realise price / value of business Ownership Why Employee Ownership? • The Company: 13 Continuing independence Values of business are maintained Business can stay in current location Productivity and innovation Ability to recruit talent Ownership Why Employee Ownership? • The Employees: 14 Ability to share in rewards Financial stake in business Control of destiny Future succession clear Ownership Why Employee Ownership? • Society: 15 Faster job creation Sustain jobs in local community Greater income equality Health benefits Ownership Differences from ‘conventional’ exit • Conventional Exits: 16 Trade Sale Management Buyout Family Succession Listing Ownership Differences from ‘conventional’ exit • Control: No third parties (apart from maybe funders) affecting the decisions and timetable. • Legacy: An objective is often to secure the legacy of the business / owner. • Due diligence: Should be limited. • Post-transfer structure: usually more important. 17 Ownership Differences from ‘conventional’ exit • Fairness: Objective may be for all to benefit rather than an individual or small group of individuals. • Timing: Can take longer than a conventional exit. • Owner involvement post-transfer: Owners often involved post-transfer, even if only in a non-executive capacity. 18 Ownership Structuring the Deal • • • • • • • 19 Price Funding Protections for Sellers Protections for new owners Taxation Leadership Engagement and Communication Ownership Price • • • • • 20 Usually commercial valuation But not always arm’s length negotiation Expectations of Sellers – becoming more realistic? HMRC? May need to revisited over the course of the process No agreement on price – no deal Ownership Funding 1. Lender: Third party funder (bank, specialist lender) provides funds, usually secured on the assets of the company. 2. Employees: Perhaps through SIP. Could be given incentives to invest early (e.g. bonus shares). 3. Seller: Deferred consideration / staggered exit. If used, need to consider protections for Seller. 4. The Company: Company cash. Will also fund the repayment of any Lender or Seller finance. 21 Ownership Funding • Can have an impact on timing • When you involve third parties you lose an element of control over timetable No agreement on price – no deal 22 Ownership Protections for Seller • Reasons for protections: − Deferred Consideration − Discounted Price − Protection of Legacy (e.g. preserving skills in a particular area; the name above the door) 23 Ownership Protections for Seller • Possible protections: − Veto rights − Right to be a director / trustee − Non-embarrassment provisions − Security − Pre-emption rights − Right to re-purchase shares / convert debt • Must be balanced against allowing freedom for the business and new owners 24 Ownership Protections for New Owners • May require warranties – especially if paying a full price. • May depend on the extent to which the employees are familiar with all aspects of the business. • Flexible repayments? 25 Ownership Taxation • Capital Gains Tax • Income Tax • Inheritance Tax • See Masterclass later in the year 26 Ownership Leadership • Not everyone will buy into / understand the transition from the beginning • Successful transitions almost always require individuals who will take the lead in the process. This could include: The current owner Elected representatives New management team 27 Ownership Leadership • Will also be important going forwards to maximise the benefits of employee ownership. • Note that leadership does not always mean someone who is in charge – the individual needs to understand the objectives and will commit time and energy to the transition. • Can sometimes be closer to a cheerleader role. 28 Ownership Engagement and Communication • Pre-transition - will vary with the circumstances • Vital post-transition to maximise advantages of employee ownership • Pre-transition, will often depend on the expected involvement of the employees (e.g. are they part funding the transition?) • Elected / nominated working group is common 29 Ownership Engagement and Communication • Employees will usually realise something is happening • They may have been thinking about succession at the same time as owners (or even before) • Beware inadvertently making misleading statements – especially regarding timetables 30 Ownership Structuring the Post-Transition • Ownership • Governance • Engagement and Communication 31 Ownership Models of Employee Ownership • Direct Employee Ownership • Indirect Employee Ownership • Combined Direct and Indirect Employee Ownership 32 Ownership Direct Share Ownership 33 Ownership Direct Share Ownership 34 Ownership Direct Share Ownership • All the shares in the organisation are held directly by the employees 35 Ownership Advantages • Direct Ownership: employees actually own the organisation • Economic Benefits: all the economic benefits of share ownership go to the employees • Simplicity: usually a simple concept to grasp • Control: the employees control the organisation 36 Ownership Disadvantages • Checks and balances: no third party to look to the long term and future employees • Sustainability: how does ownership transfer? • Administration: share transfers etc. 37 Ownership Implementation • How to put shares in the hands of employees? Employees pay full value for the shares Employees pay discounted value for the shares (tax implications) Use HMRC approved share scheme, e.g. Share Incentive Plan Share Options Issue partly paid or unpaid shares (tax implications) 38 Ownership Implementation • What, if any, criteria should be applied when determining if and when an employee can acquire shares? • What rights should attach to shares and to shareholders? 39 Ownership Indirect Share Ownership 40 Ownership Direct Share Ownership • All the shares are held on behalf of the employees, usually in a trust for the benefit of the employees 41 Ownership Advantages • Sustainability and Stability: Ownership is fixed and stable • Economic Benefits: The trust can provide economic benefits to employees (although not always very tax efficient) • Simplicity: One shareholder • Long term: Trustees usually have responsibility to look long term • Forum: Trust can act as forum for employees • Tax: Should Qualify for the new CGT relief 42 Ownership Disadvantages • Is it employee ownership?: No employees own any shares • Economic Benefits: Capital value remains locked in trust – what incentive is there to increase it? • Connection: Will employees feel remote from ownership? • Administration: A tax return will need to be filed for the trust each year 43 Ownership Implementation • Key issue is establishing the trust and its remit: Trustees Powers Discretion of trustees Assets on a winding up Jurisdiction Letter of Wishes / Recommendation 44 Ownership Hybrid 45 Ownership Hybrid 46 Ownership Hybrid 47 Ownership Advantages • Direct ownership: Employees actually own shares. • Economic Benefits: Can accrue to employees. Trust will sometimes waive right to dividend to maximise the dividend to employees. • Sustainability: Ownership of a block of shares is fixed and stable. The EBT will sometimes have a fixed minimum shareholding. • Tax: Should qualify for new CGT relief if EBT holds >50% 48 Ownership Advantages • Long Term: The trustees usually have an obligation to look to the long term interests of the employees. • Forum: The EBT can act as a forum for employees. • Buying and Selling Shares: The EBT can buy and (maybe) sell shares. Very useful when acquiring an ex-employee’s shares. 49 Ownership Disadvantages • Complexity: Especially with a SIP when you will have two trusts. • Administration: Record internal share market, tax returns for trusts. • Value of the business: A significant part of the value of the business will be locked in the trust. 50 Ownership Implementation • See previous models • Should the EBT have a minimum shareholding? • Should there be a limit on individual employee’s shareholdings? • If the EBT holds the majority of the shares, should it also have a majority of the voting rights? 51 Ownership Governance • Allocation of powers / decision-making within the organisation. • Accountability. • Can facilitate Engagement. 52 Ownership Conventional Model 53 Ownership Employee Ownership 54 Ownership The Parties • • • • • • • 55 Employees Directors Shareholders Employee Benefit Trust / Trustees Supervisory / Representative Body Seller? Founders / Founding Family? Ownership The Powers • Default powers exist for: Shareholders (ultimate controllers of the company) Directors (day to day control of the company) • Within some limits, you can amend these default powers to grant greater or lesser powers to these groups – and grant new powers to other groups (e.g. employees) 56 Ownership The Powers • There is no definitive list of powers (they will vary), but issues to consider include: Who appoints directors? Who appoints trustees? Are certain decisions so fundamental to an organisation that everyone should be involved (e.g. a sale of the business)? But avoid management by committee – you need an effective management structure 57 Ownership The Powers • Majority / Unanimous / Super majority vote? • Consent from more than one body? • Opportunity for consultation / discussion prior to decision? • Quorum for meetings • Should there be a permanent block on certain decisions? • Confidentiality 58 Ownership Engagement and Communication • Vital to maximise the benefits of employee ownership • Can have a number of roles: Awareness Education Transparency / Trust Accountability / Governance Inclusiveness / Partnership 59 Ownership Engagement and Communication • Detail will vary, but some broad principles: Time: will be needed Proactive: should not be passive Structure / Responsibility: formally allocate responsibility to certain bodies / individuals Two-way: communication should work both ways Dynamic: usually needs to be able to evolve and change over time Confidentiality: consider if applicable 60 Ownership The Future for the Organisation • The importance of flexibility • Revisit structures and models in the future • But: consider whether certain elements should be immovable – or subject to special consents should one generation of employees be able to ‘cash out’ at the expense of earlier and future generations? 61 Ownership The Future for the Sector • £70m of tax reliefs from the government in 2014 • Employee Ownership Day • Evidence showing the benefits growing • 2012 / 13 – Number of EO businesses increased by over 10% • Objective of 10% of GDP 62 Ownership Final Thoughts • Extremely flexible model • There can be a degree of complexity involved • No two will be alike • Beware the tax tail (or any other tail) wagging the dog • The importance of leaders / cheerleaders 63 Ownership Ewan Hall ewan.hall@baxendale.co.uk 07880 382 102 http://www.baxendaleownership.co.uk/ 64 Ownership Future Briefing Sessions • Funding the employee buy-out, 9 April 2014 , Glasgow • Tax implications in employee ownership, 7 May 2014, Glasgow • Employee share ownership, 10 September 2014, Edinburgh • Governance in the employee owned business, 5 November 2014, Glasgow For more information visit: www.cdscotland.co.uk