Fiscal Policy

advertisement

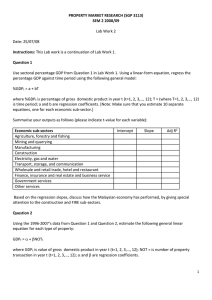

Fiscal Policy DebtEnd This Year DebtEnd Last Year General DeficitThis Year General Expenditure / OutlaysThis Year General Revenue / IncomeThis Year General DeficitThis Year General DeficitThis Year General BalanceThis Year IMF Fiscal Indicators Figure 2. Sovereign Bond Yield Spreads over German Bunds (Basis points) 1800 1600 C ountries w ith Program s Supported by EU /IMF 1400 1200 G reec e 1000 Crisis spreads to other countries 800 Irelan d 600 Po rtug al 400 Ro man ia 200 Latv ia 0 J an -10 Ap r-10 J ul-10 O c t-10 J an -11 Ap r-11 J ul-11 450 IMF Fiscal Monitor Selected European C ountries 400 350 300 Sp ain 250 Background Reading 200 150 Italy 100 50 Belg ium Neth erlands Fin land 0 J an -10 Ap r-10 J ul-10 O c t-10 J an -11 Ap r-11 J ul-11 Sources: Bloomberg L.P.; Datastream. Note: 10-year sovereign bond yields. Can you run a deficit every year? Debtt Debtt 1 General Deficitt 1 GDP GDPt (1 g ) GDPt-1 GDPt Debtt Debtt-1 GDPt GDPt-1 Debtt 1 (1 g GDP ) Debtt 1 General Deficitt 1 GDP GDP (1 g ) GDPt-1 (1 g ) GDPt 1 GDPt General Deficitt g GDP Debtt-1 GDPt (1 g GDP ) GDPt-1 Sustainable Deficit If General Deficitt g GDP Debtt-1 GDP GDPt (1 g ) GDPt-1 then Debt-to-GDP ratio stays stable. If > then deficit is “unsustainable” A growing economy allows the government to borrow some money every year and still keep debt in line with overall GDP Primary Deficit Simplified Government Budget Primary Expenditure (Total Expenditure less Interest Paid) - Primary Revenue (Total Revenue less Interest Income) Primary Budget Deficit + Net Interest Payments on Existing Debt General Budget Deficit Sustainable Primary Deficit General Deficitt Primary Deficitt Net Interestt GDPt GDPt GDPt ~ Net Interestt Debtt-1 i GDP GDPt (1 g ) GDPt-1 Average Interest • If Primary Deficitt g GDP i Debtt-1 GDPt (1 g GDP ) GDPt-1 then Debt GDP stays stable. Primary Balance % of GDP Types of Taxes Taxes on Value Added and Imports + Taxes on Income and Wealth (Income Taxes, Corporate Profits Tax, Capital Gains Taxes, Property Taxes) + Social Security Contributions Total Taxes Greece Germany 40 40 35 35 30 30 25 % of GDP 25 % of GDP 20 15 20 15 10 10 5 5 0 2000 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2001 2002 2003 2004 2005 2006 2007 2008 2009 Revenue Statistics Comparative tables http://stats.oecd.org/Index. aspx Tax Revenues Types of Expenditure Consumption Expenditure Goods expenditure + Compensation of Gov’t Employees measured in GDP + Gross Capital Formation + Social Benefits & Transfer Payments Primary Expenditure Consequences of Deficits Austerity Inflation Default Austerity and the Output Gap YP P 1 P* 1. Economy in LT equilibrium 2 Y* Recessionary Gap SRAS 2. Government imposes austerity program – cuts spending, AD transfers, inceases AD′ Ytaxes 3. AD Curve shifts inward. Austerity has a negative effect on business cycles. IMF Deficits and Inflation Government generates revenues by printing new money (referred to as seignorage). Government facing borrowing constraints may be forced to rely on inflation tax for deficit financing and real returns to owning money. Explain the link between deficits and inflation. 19 70 19 71 19 72 19 73 19 74 19 75 19 76 19 77 19 78 19 79 19 80 19 81 19 82 19 83 19 84 19 85 19 86 19 87 19 88 19 89 19 90 Israel 1970-1990 Inflation 400 350 300 250 200 150 100 50 0 Israel 1970-1990 Surplus (% of GDP) 5.00% -5.00% -10.00% -15.00% -20.00% -25.00% -30.00% 1990 1989 1988 1987 1986 1985 1984 1983 1982 1981 1980 1979 1978 1977 1976 1975 1974 1973 1972 1971 1970 0.00% Default and Restructuring Argentina 1999-2002 BBC Story IMF Study Argentina GDP 5.4E+11 5.2E+11 5E+11 4.8E+11 4.6E+11 4.4E+11 4.2E+11 4E+11 1997 1998 1999 2000 2001 2002 2003 2004 2005 Stabilization policy In an economy subject to shocks to aggregate demand (animal spirit shocks, external shocks, asset market shocks), the economy will have a self-correcting mechanism. However, if this self-correction mechanism takes a long time to work, then government may use policy to speed adjustment. ◦ Use expansionary policy to close a recessionary gap ◦ Use contractionary policy to close an inflationary gap Demand Driven Recession Counter-cyclical fiscal policy YP P P* 3 1 2 Y* Recessionary Gap SRAS w/ 1. Economy in LT equilibrium 2. Demand shifts in 3. Government increases AD spending to shift the AD curve back AD′ Y Demand Driven Expansion Counter-cyclical fiscal policy YP P SRAS 3. Government cuts spending to shift the AD AD′ curve back 1 3 Y* 1. Economy in LT equilibrium 2. Demand shifts out 2 P* w/ AD Inflationary Gap Y Lags and Fiscal Policy Administrative lags for fiscal policy may likely be large. Except in absolute dictatorships, government will have mechanisms for building a consensus for expenditures. Adjusting this consensus will be time consuming. If lags are too long, stabilizing government spending or transfer payments may have a destabilizing effect, shifting out demand after the economy has already recovered. Tax Smoothing Governments in most economies issue debt to make up for shortfalls in revenues in relation to spending. Budget Deficit = Outlays – Revenues Tax collection is cyclical so the budget deficit tends to be counter-cyclical. Maintaining a balanced budget over the cycle means raising taxes in a recession an cutting taxes in a boom which makes the business cycle more extreme. Learning Outcomes Use growth rate of GDP, interest rates, and the debt to GDP ratio to identify the sustainable general and primary deficit level. Use AS-AD model to identify the effects of fiscal policy on the output gap and the inflation rate.