Value - Analyst Reports

advertisement

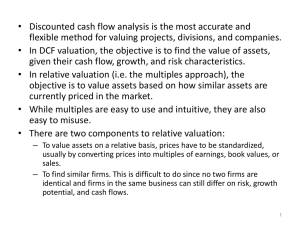

“I Will Return!!” (not GEN MacArthur) A Charter Class member returns to speak on PE Valuation Bruce B. Bingham, FASA, FRICS 23 September 2013 Getting Started – Definitions • Value – A useless word by itself. • Fair Market Value (“FMV”) – Amount at which property would change hands between a willing buyer and a willing seller where neither is acting under compulsion and when both have reasonable knowledge of the relevant facts. • Fair Value – Statutory standard of value used in courts usually involving dissenting shareholders’ litigation. • Going Concern Value – Assumes the business continues as a viable operating enterprise, including intangibles such as trained workforce, licenses and operating procedures. • Investor Value – Value to a particular buyer/investor considering his or her specific personal circumstances, knowledge of the transaction and potential synergy. • Total Capital Value – Value of Fair Market Value of 100% of the equity plus the market value of long term debt. Usually used in calculating performance ratios. • Liquidation Value – Value from piecemeal sale of assets. (Opposite of Going Concern Value). Can be orderly or forced. Typically low end of value spectrum. • Book Value – An accounting term for the value of total net assets minus total liabilities on the balance sheet. Intangibles usually excluded. • Minority Value – Value reflecting an ownership position of less than 50%. Frequently expressed as a discount. • Control Value – Additional value inherent in a legally controlling interest, reflecting the power of control. Frequently expressed as a premium. • Marketable Value – Value of an equity assuming a pre-established market in which that equity can be exchanged. • Non-marketable Value: – Decreased value due to the limitation in the marketability of an equity. Opposite of Freely Traded Value. Usually expressed as a discount. 1 Getting Started – Key Questions • What definition of value? • What is being valued? • Premise of Value? • Valuation Date v. Report Date • Type of Report? • Distribution? 2 Approaches – Cost Approach • Premise – Value equals FMV of Assets Minus FMV of Liabilities • Mechanics – Value Each Tangible and Intangible Asset – Subtract Market Value of Liabilities Advantages Drawbacks - Useful for asset intensive businesses profit - No consideration of "going-concern" or - Preferred by lenders - Intangibles defensible, but difficult - Facilitates purchase price allocation - Cumbersome valuation process - Excluding intangibles, can represent "liquidation" value - Lack of information 3 Approaches – Market Approach • Premise – The value of the target can be estimated by looking at prices paid for minority or controlling interests in the public marketplace – Ex-Ante approach • Mechanics – Identify "comparable" companies – Calculate multiples and adjust for target company – Apply multiples to adjusted subject company financial statements – Produces minority, marketable value – Apply premiums or discounts as appropriate Advantages Drawbacks - Value based on actual prices paid for comparable companies - Does not take into account synergies - Use of hard numbers - Focuses on historical results - Multiple multiples - Multiple multiples can lead to a divergence of indicated values - Requires estimation and application of premiums and discounts 4 Market Approach - Nuances • Guideline Company or Representative Transactions • Multiples Relevant to Industry Being Valued. • TIC or Equity Multiples? • Comparable Company Medians or Averages? • Haircuts to multiples. • Adjustment from Minority, Freely Traded Basis. • For Transaction Comps, Lookbacks before 15 September 2008 • Forward Multiples? An IB tact that mixes approaches 5 Income Approach – Premise and Mechanics Overview • Premise – The Value of the target can be estimated by forecasting the future financial performance of the business and identifying the cash flow that the business generates – Forward-looking approach • Mechanics Overview – Forecast the target company's financial performance (income statement, statement of changes, and balance sheet) – Identity the cash flow-negative or positive-in each forecasted fiscal year – Estimate the value of the target at the end of the forecast period (terminal value) – Estimate the target's risk-adjusted cost of capital – Discount the forecasted cash flows and the terminal value amounts by the cost of capital – Subtract actual borrowings at valuation date (long-term and short-term) to estimate the value of the business to its owners 6 Income Approach – Advantages & Drawbacks • Advantages – The DCF method forces you to translate future benefits from a business into hard dollars. – The DCF method forces you to understand the target's business – The DCF method allows one to identify the expected cash flow that may be used to service debt – You can reflect the impact of the business cycle in the DCF analysis • Drawbacks – It is difficult to forecast with any degree of accuracy. You can compensate by developing different operating scenarios and measure their impact on value. – Certain key assumptions can wildly alter DCF values – It is difficult to value the target at the end of the forecast period – DCF value, including synergies, may result in the buyer overpaying for the target 7 Income Approach - Nuances • Hockey stick projections • “Reasonably Objective Basis” • Perpetual Growth Rate • Projection Period • WACC – Beta – Company Specific Risk Premium – Baa as a Proxy for Cost of Debt – Tax Adjusted Cost of Debt 8 Conclusion of Value • Risk in Market Approach v. Risk in Income Approach • BBB’s Cherry-Picking Postulate: If information exists with which to apply an approach to value, then you better use it (or explain why not). • Use experience and professional judgment in reconciling your indications of value from the various approaches. • No formulas or averages. Explain basis for weighting. 9