10oct07-Hitchen - RAeS Human Factors Group

advertisement

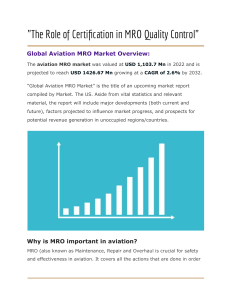

Airclaims Global Reach Local Presence Rapid Response Adding Value - An Insurer’s Viewpoint David Hitchen Aviation Surveyor Maintenance Related Claims….. Setting the Scene • Insurance for aircraft maintenance activities: • Hull All Risks Policy – taken out by airline to cover physical hull damage. • Hangar-keepers Policy - taken out by MRO to cover for physical damage to aircraft when under their care custody & control. • Products Policy – taken out by MRO to cover for physical damage to aircraft when in service – resulting from a maintenance error. • Contract wording essential in establishing liability. • Policy wording essential in establishing coverage. The Current Market-place • Downwards pressure on premium rates continues • Due mainly to reducing worldwide loss levels • Also a result of increased competition within Insurance Markets both in London (still the largest market) and overseas due to increased capacity worldwide. • Insurers exposure increasing • Average fleet value increasing. • Maintenance activity levels at MROs increasing globally in line with the expansion of commercial aviation and a growth in outsourcing – increase in Low Cost Carriers. Airclaims’ Role in Market • Essentially providing technical expertise to Insurance Market using a worldwide team of 50 plus surveyors. • Majority of work relates to technical handling of insurance claims on all aircraft types – from minor ramp handling incidents to total losses. • Additionally undertake risk survey activities for Insurers on Operators, Maintenance Organisations and Airports. • Provide technical expertise to Aviation Lawyers in support of legal subrogation activity. Safety Management Systems – Insurance Implications. • Aviation is highly regulated in most parts of the world with safety being a critical consideration. • Insurers assessment of a particular risk covers many aspects of the organisation in question: • • • • • • Operational Environment Facilities. Activities. Structure and management philosophy. Previous loss records – number / cost. Future planned activities – expansion etc. Safety Management Systems – Insurance Implications cont… • Relevant Factors • Market conditions – supply & demand • Historical relationship – e.g. value of established ties between Insurer and Insured • Existence and maturity of a Safety Management System. • The SMS will not in itself attract a lower premium. • More likely to have an effect on the premium when considered within the entirety of the risk. Practical Experience – A Case Study. • The risk in question, an MRO, was in the process of Policy renewal with 2 consecutive years with a high number of claims. • MRO had been taken over by a new company who wished to include the risk in their current policy. • Insurers in question were concerned about the loss record of MRO however had a long historical relationship with parent company. • Airclaims were commissioned to undertake a Risk Survey of the MRO to provide reporting to Insurers and parent company. Claims History • Numerous (in excess of 20) small attrition type claims which amounted to approximately US$3.5M of losses over 2 year period. • 2 substantial losses with safety implications one of which was an engine fire on take-off that the on board extinguishers failed to contain, second was a thrust reverser cowling failure on landing. Both related to maintenance errors. Combined cost of these two claims alone US$3.8M. The Serious Side ….In Flight Events. Original Company Structure • Traditional Airline Engineering department that had developed into an MRO. • Airline accounted for 80% of workload for many years. • Safety maintained along lines of old style Quality Department with Regulatory Audits. • No Safety Management System and gradual reduction in investment through cash flow issues leading to low morale. Regulatory Audits. • Tended to be very focussed on certain process issues but did not address the big picture. • Partly a box ticking exercise albeit they did raise a number of non-conformances that were addressed by MRO. • Aircraft damage issues were not generally seen as airworthiness problem as defects all rectified and certified correctly therefore safety not considered to be affected. • More serious losses were investigated by authorities with recommendations being made. New Management • The parent company appointed a new management team. • Turning the business around from a commercial point of view extremely important for long term security of organisation. • This commercial vision had safety and SMS at its heart as the moral and business benefits were clearly understood by new owners. • Reducing loss record and hence premium seen as essential. Risk Survey • Undertaken over 7 day period at MRO’s two key business centres. • Planned, pre-arranged survey gave management team an opportunity to assess and address many key issues prior to site visit. • Risk survey and policy renewal seen as a prime instigator in improving processes from a safety point of view. • Meeting held with workforce prior to survey to explain the business imperative to improving safety. Survey Process • Intention of survey is not to replicate regulatory audit. • Look at big picture issues regarding management structure, facilities, culture and safety initiatives. • In depth review of critical processes, particularly training and qualifications, safety awareness, health and safety and production/capacity control. • Access to highest level management and freedom to alter survey schedule as required. • Feedback presentation at end of survey. Survey Report • Survey Report including key recommendations submitted. • Report designed to accurately reflect state of organisation highlighting both positives (SMS etc) and any negatives. • Provided a datum for future assessment of organisation particularly in response to recommendation. • Gave Insurers an independent assessment of the organisation, confirming the effectiveness of safety initiatives being implemented such as SMS. Conclusions • The involvement of Insurers in assessing the business activities of the organisation reinforced the already instigated safety initiatives. • Using the Insurers and hence the financial viewpoint added strength to the message being put to the MRO’s production staff in addition to confirming the Management’s commitment. • Tangible results have been seen in a dramatic reduction in claims, only 2 in 9 months. • Involvement of Insurers contributed to improved safety culture and processes within organisation. Thank you for listening The information used in this presentation has been assembled from many sources, and whilst the utmost care has been taken to ensure accuracy, the information is supplied on the understanding that no legal liability whatsoever shall attach to Airclaims Limited, the Airclaims Group Holdings Limited, its subsidiaries, their officers, or employees in respect of any error or omission that may have occurred.