CH02

advertisement

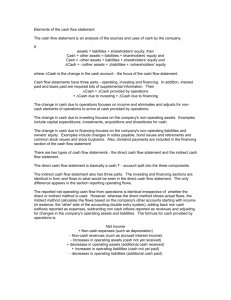

Financial Statements of Limited Companies - Balance Sheet Session Summary (1) learning objectives financial statements the three key financial statements the main elements of the balance sheet the main elements of the profit and loss account the main elements of the cash flow statement Session Summary (2) a typical horizontal balance sheet format capital and reserves or shareholders’ equity liabilities the relationship between risk and return assets a vertical format balance sheet valuation of assets Learning Objectives (1) explain the differences in accounting treatment of capital expenditure and revenue expenditure identify the financial information shown in the financial statements of a company: balance sheet; profit and loss account; cash flow statement construct simple financial statements outline the structure of the balance sheet of a limited company classify the broad balance sheet categories of shareholders equity; liabilities; assets Learning Objectives (2) outline the alternative balance sheet formats prepare a balance sheet evaluate some of the alternative methods of asset valuation appreciate the limitations of the conventional balance sheet Capital Expenditure and Revenue Expenditure Revenue expenditure relates to expenditure on those items where the full benefit of making that expenditure is received within the current accounting period Capital expenditure relates to the cost of acquiring, producing or enhancing fixed assets, the full benefit of which is received within future accounting periods Financial Statements (1) Limited companies are required to periodically prepare three main financial statements: balance sheet profit and loss account cash flow statement Financial Statements (2) Financial statements are required for the shareholders the Registrar of Companies and are also used by, for example analysts potential investors customers suppliers The Three Key Financial Statements The Main Elements of the Balance Sheet The Main Elements of the Profit and Loss Account The Main Elements of the Cash Flow Statement A Typical Horizontal Balance Sheet Format Capital and Reserves or Shareholders’ Equity capital share premiums retained earnings Liabilities current, or short-term, liabilities short-term financial debt trade creditors (or accounts payable) accruals long-term liabilities long-term financial debt long-term trade creditors (or accounts payable) provisions The Relationship Between Risk and Return Assets (1) fixed assets tangible fixed assets intangible fixed assets financial assets current assets Assets (2) stocks debtors (or accounts receivable) cash prepayments A Vertical Format Balance Sheet (1) A Vertical Format Balance Sheet (2) fixed assets (FA) + current assets (CA) – current liabilities (CL) – long-term liabilities (LTL) =equity (E) FA + (CA – CL) – LTL = E Valuation of Assets (1) valuation of items within the balance sheet is covered by the Companies Act 1985/1989, accounting concepts and standards problems arise from differences in approach, and alternative methods used to value the different categories of assets and liabilities: fixed assets brand names goodwill research and development costs stocks debtors foreign currency transactions Valuation of Assets (2) There are limitations to the conventional balance sheet arising not only from the fact that it is an historical document, but from inconsistencies in its preparation due to differences between companies and industries employment of various asset valuation methods off-balance sheet financing window dressing