Chapter 17

McGraw-Hill/Irwin

Sharing Firm Wealth:

Dividends, Share

Repurchases, and Other

Payouts

Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

1

Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved

Introduction

• Taxation of capital distributions

– Different treatments for capital gains versus dividends

and interest payments

– Differing tax rates for shareholders

17-2

Dividends versus

Capital Gains

• Use the constant growth formula to choose

between paying cash dividend or stock

repurchase

17-3

Dividends versus

Capital Gains

Firms that pay out high percentages of current

earnings have less capital to fund future

growth

17-4

Dividends versus

Capital Gains

• Firms that keep more retained earnings have less

to pay current dividends

• Recommend firms retain earnings to extent they

can make project investments with as high return

as investors could earn elsewhere at similar risk

17-5

Dividend Irrelevance Theory

• Modigliani and Miller

• In perfect world the decision to pay or not to

pay dividends does not matter

17-6

Dividend Irrelevance Theory

• Reminder: The “perfect world” assumes

– No taxes

– No transaction costs

– Perfectly competitive markets

– Completely rational investors

17-7

Dividend Irrelevance Theory

• In M&M’s “perfect world,” paying dividends reduces

each share’s value by the dividend amount

• If the firm chooses not to pay dividends, investors

who want dividends can sell their shares to realize

income not supplied by dividends

17-8

Dividend Irrelevance Theory

• In 2003, tax rates on capital gains and most

dividends lowered

• Dividends now more attractive relative to

capital gains

17-9

Why Some Investors Favor

Dividends

• Bird-in-the-hand theory

– Dividends less risky, more attractive to risk-averse

investors than future capital gains

• Bird-in-the-hand fallacy

– Most investors invest dividends in similar firms

– Firm’s risk profile determined by asset cash flows

not dividend payout policy

17-10

Why Some Investors

Favor Capital Gains

At the same tax rates, capital gains have

potential tax advantages over dividends

– All shareholders pay taxes on dividends

– Only selling shareholders incur taxes on realized

capital gains when a growing firm retains earnings

17-11

Other Dividend Policy Issues

• Tangible effects

– Risks

– Taxation

– Cash flow timing

• Also intangible effects

17-12

The Information Effect

• Firms hesitate to increase dividends unless

they can be maintained

• Analysts interpret dividend increases as

positive signal about firm’s future cash flows

17-13

The Clientele Effect

• Investors (clientele) have different desires

about taxability and timing of firm payouts

• Payout policies of different firms attract

different investor groups

17-14

Corporate Control Issues

• Shareholders with large stakes in the firm may

dictate dividend payout policy

• Closely-held companies may retain more

earnings as owners try to minimize the effect

of double taxation

17-15

Real-World Dividend Policy

• Basic dividend policy

– Pay out surplus cash flow as dividends after

investing in positive net present value projects

17-16

The Residual Dividend Model

• Also known as the free cash flow theory of

dividends

• Assumes that cash flow, beyond that needed

to invest in positive NPV projects, is paid out

as dividends

17-17

Extraordinary Dividends

• Firms divide dividends into two classes to

manage

1) Ordinary dividends (relatively low)

2) Extraordinary dividends (periodic, extra)

• Firms forego extraordinary when needed

17-18

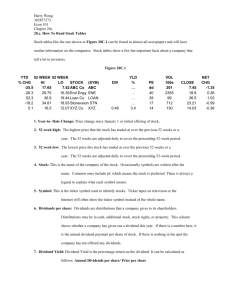

Dividend Payment Logistics

• Declaration date

– Board of directors announces intention to pay a

dividend

– Firm records the liability on its books

• Ex-dividend date

– The first day that shares trade without dividend

attached

17-19

Dividend Payment Logistics

• Record date

– Firm identifies the owners of record to begin

addressing payments

– Record date is set several business days after exdividend date to allow time for registration

process

• Payment date

– Firm sends out the dividends

17-20

Effect of Dividends on Stock Prices

• Stock prices increase as the next dividend

approaches

• Stock prices fall by the present value of the

dividend once the stock goes ex-dividend

17-21

Stock Dividends

and Stock Splits

• Both increase shares outstanding without

changing total market value of owner’s equity

• Both will decrease the stock price

17-22

Stock Dividends

• Pro-rata distribution of new shares to current

stockholders

– Example: A 20 percent stock dividend would

increase the number of shares held by each

shareholder by 20 percent

17-23

Stock Splits

• Company exchanges new shares for old shares

• Each old share usually converts into more than

one new share

17-24

Stock Splits

• Alter par value of firm’s stock on company’s

books

• Do not cause shift in owner’s equity accounts

17-25

Effect of Splits and Stock

Dividends on Stock Prices

• Firms want shares to trade in price range

– Stock dividend or split brings stock price back in

range

• Investors like to trade in 100 share “round

lots”

17-26

Stock Repurchases

• Firm buys shares of own stock on stock

exchange like any investor

– Open-market stock repurchase

– May take months or years

17-27

Advantages of Repurchases

• Can offer an efficient way to return money to

shareholders

• Reduction or cessation of repurchases not

seen as a negative

17-28

Disadvantages of Repurchases

• Can make firm vulnerable to litigation from selling

shareholders

– Management may have undisclosed information about

good future prospects for firm

• Overpayments for shares result in share dilution

• IRS penalties if proven the repurchase was primarily

to avoid dividend taxation

17-29

Effect of Repurchases on

Stock Prices

– Advantages outweigh the disadvantages

– Repurchasing companies produce significant

excess returns for several years after repurchase

17-30