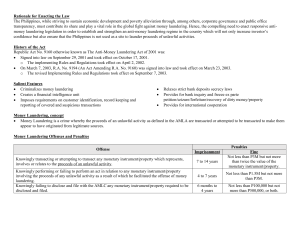

")