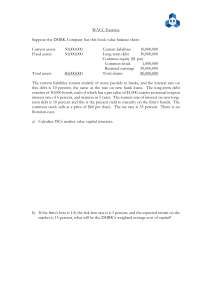

Chapter 1: 1. Three major advantages and two disadvantages of the corporate business form? a. Advantages i. Limited Liability protects owners from losing more than they invest ii. Can achieve large size due to marketability of stock iii. ownership is readily transferable. b. Disadvantages i. Double taxation because both corporate profits and dividends paid to owners are taxed, although the dividends are taxed at a reduced rate ii. Subject to more government regulation 2. According to the textbook, what is the primary objective of a corporation and what is the ultimate benchmark for measuring this objective? a. The primary object is shareholder wealth maximization and benchmark for measuring this objective is stock price 3. What are the three elements that affect the corporate’s value? a. Its size of the expected future cash flow, b. The timing of cash flows counts, c. the risk of the cash flows matters 4. Name three ways in which businesses can raise money from external sources when they need it for expansion or project funding. a. Direct Transfer b. Through Investment Bank c. Through Financial Intermediary 5. While interest rate actions by the Federal Reserve captures most headlines, what is the most common method for the Federal Reserve Board to try to influence the economy and what does that action entail? a. Establish or set up the target rates for the federal reserve. b. Change the interest rate or the discount rate which is charged to the banks when the business cycle changes. Sensitivity: Internal Chapter 2: 6. Three major component of Cash flow Statements a. Operating Activities It includes the adjustment of net income by adding back the item which has no cash flow impact to business like depreciation. b. Financing Activities. It includes borrowing, debts and dividend which has cash inflow and outflow impact. c. Investing Activates. It includes the purchasing, acquisition and sale of equipment’s land building which impact cash flow of the business. 7. Rao Corporation Net operating Working Capital = Current assets required in production - Noninterest-bearing current liabilities Current assets required in production = Current assets - short-term investment Current assets required in production = $130 - $30 Current assets required in production = $100 Noninterest-bearing current liabilities = Accounts Payable + Accruals Noninterest-bearing current liabilities = $20 + $20 Noninterest-bearing current liabilities = $40 Net operating Working Capital = $100 - $40 Net operating Working Capital = $60 8. TSW Inc Free cash flow = NOPAT - Net investment in operating capital Net investment in operating capital = Total operating capital completed year - Total operating capital last year Net investment in operating capital = $2500 - $2000 Net investment in operating capital = $500 Sensitivity: Internal Free cash flow = $925 - $500 Free cash flow = $425 9. Bae Inc. Net operating profit after tax = Earnings before interest after taxes. Net operating profit after tax = $455 Sales Costs Depreciation EBIT Taxes (35% of EBIT) Net operating profit after tax 2,000.00 (1,200.00) (100.00) 700.00 (245.00) 455.00 10. HHH Inc. Sales $12,500 Operating cost including depreciation ($7,025) EBIT $5,475 investor-supplied operating assets (or capital), $18,750 WACC 9.50% Income Tax Rate 40% EVA = EBIT(1 – T) – Investor Capital x WACC EVA = $5,475 (1-40%) - $18,750 x 9.5% EVA = $3,285.00 x $1,781.25 EVA = $1,503.75 Sensitivity: Internal Chapter 3. 11. How much debt must the company add or subtract to achieve the target debt ratio? Target amount of debt – Present Debt = Amount of debt the company must add or subtract to achieve the target debt ratio. A. B. C. D. Total assets = $625,000 Present debt = $185,000 Target debt ratio = 55% Target amount of debt = $625,000 X 55% Target amount of debt = $343,750 Amount of debt the company must add or subtract to achieve the target debt ratio = Target amount of debt – Present Debt Amount of debt the company must add or subtract to achieve the target debt ratio = $343,750 $185,000 Amount of debt the company must add or subtract to achieve the target debt ratio = $158,750 12. Credit Period Sales Receivables DSO (($60,000 x 365)/$425,000) DSO – Credit Period = days early or late 51.53 – 45 = 6.53 days late 13. What was its profit margin on sales? Net Income / Sales = Profit Margin $23,000/$320,000 = 0.071875 = 7.19% Sensitivity: Internal 45 $425,000 $60,000 51.53 14. What was the firm's times interest earned (TIE) ratio? Sales $435,000 Operating Cost $362,500 EBIT ($435,000 - $362,500) $72,500 Interest EBIT / Interest Expenses = Time Interest Earned Ratio $72,500/$12,500 = 5.8 Sensitivity: Internal $12,500