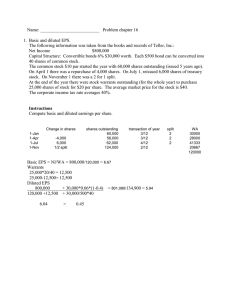

Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ IAS 33 EARNING PER SHARE IAS 33 applies to: - Entries whose ordinary shares or potential ordinary shares are publicly traded or that are in the process of issuing shares in the public. - Entries that voluntarily chose to disclose. When both parent and group information are presented together, only the earnings per share for the group are required to be disclosed. Definitions of key terms (IAS 33) Ordinary share; An equity instrument that is subordinate to all other classes of equity instrument. Potential Ordinary share Basic earning per share: 1. BASIC EPS Basic EPS is: profit/(loss) attributable to ordinary equity holders Weighted average no. of ordinary shares outstanding during the period. Shares If there have been no changes in the share capital of the company during the period then the weighted average is just the number of shares in issue throughout the period. IAS 33 is primarily concerned with how to deal with changes in share capital during a period. The principal objective is to keep consistency between the numerator and denominator. Dilution The reduction in earnings per share or increase in the loss per share resulting from the assumption that potential ordinary shares will materialize. Anti dilution An increase in earning per share or a reduction loss per share resulting the assumption that potential ordinary shares will materialize. Ordinary shares An “ordinary share” participates in profit for the period only after other types of shares, such as preferred shares, have participated. Presentation of earnings per share An entity should present on the face of the income statement both basic and diluted earnings per share for profit or loss from continuing operations attributable relative to the ordinary equity holders of the parent and for profit or loss attributable to the ordinary equity holders of the parent by each class of ordinary shares with different rights. Basic earning per share: 2. BASIC EPS Basic EPS is: profit/(loss) attributable to ordinary equity holders Weighted average number of ordinary shares outstanding during the period CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 1 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ - Earning are calculated as Amounts attributable to the ordinary shareholder in respect of profit or loss from continuing operations and net profit or loss. After all expenses including taxes and minority interest. After cumulative preference divided for period whether declared or not After non-cumulative preference share dividend declared for period. After other adjustments relating to preference shares. Number of ordinary shares - Number of ordinary shares at the beginning of the period are added to the number of shares issued during the period less the numbers it shares bright back in the period. - Shares issued and bought basic are multiplied by a time weighting factors dependent on when the event took place. - Shares are included from the date the consideration is receivable. - Partly paid shares are included as fraction shares to the extent that they are entitled to participate in dividends during the period relative to a fully paid ordinary share. New Issues of ordinary share Types (1) Full paid issued at market price (2) Partly paid issued at market price (3) Bonus issue/capitalization issue/scrip issue share freely for executives shareholders free of charge. They are of consideration received Number any adjustment regarding to time is done. But also number of share prior year should be added back. (4) Right Issue Capitalization or Bonus issue and share split/reverse share split. - These two types of event can be considered together as they have a similar effect. In both cases, ordinary shares are issued to existing shareholders for no additional consideration. The number of ordinary shares has increased without an increase in resources. This problem is solved by adjusting the number of ordinary shares outstanding before the event for the proportionate change in the number of shares outstanding as if the event had occurred at the beginning of the earliest period reported. Right Issues Rights issues are normally made at less than the fall market price. A rights issue combine the characteristics of an issue at full market price with a borrow issue. The knighted average included the bonus element for the full year plus the fall price element on a time apportioned basis. There are five stages to the processes: 1st calculate theoretical ex-rights price. 2nd calculate bonus element of the issue 3rd calculate the full price element this will be a balancing figure. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 2 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ 4th calculate the weighted average number of shares in issue for this year. 5th calculate especially for the current year. 6th Re-calculate (or restate) the ESP for the prior year. DILUTED EPS; Many companies issue convertible instruments, options and warrants that entitle their holders to purchase shares in the future at a below market price. When there shares are eventually issued, the interests of the original shareholders will be diluted, the dilution will not always occur because there are more shares in issue, but also because these share will have been issued at below market price. - This may affect investors buy or sell decisions, and so IAS 33 requires entities to disclose a diluted EPS and as well as basic EPS. The diluted EPS is calculated EPS is calculated using current earnings but assuming that the worst possible future dilution has already happen. Example of dilutive factors (a) Convertible bonds and convertible preference shares. (b) Option and warrant (c) Party paid share (d) Contingently issuable shares i.e. Shares issuable if certain conditions are met. Convertible bonds and convertible Preferences shares The EPS will be affected in two ways Earnings will be increased, because the finance costs will cease on conversion. Earnings will be divided amongst more equity shares. Generally, conversion will decrease the EPS. Options and warrants to subscribe for shares. - Options and warrants normally give their holders the right to purchase shares in the future at below market price. IAS 33 Breaks down the future issue in to two components. An issue of shares at full markets price. This will not dilute will dilute the interests of the other shareholders interests. A free issue to the warrant/option holders for no consideration. This will dilute the interest of the other shareholder. Partly paid shares. Some times partly paid shares are only entitled to a proportion of their dividend. These partly paid shares will be treated as a fraction of an ordinary share when calculating basic EPS. Future payments will increase proportion of shares entitled to a divided. If the share price has risen since the date of issue then the cash received will be less than the market rate at the time. This will dilute the interests of the existing fully paid shareholder. Contingently issuable shares. - Some times shares are issued as reward if specific performance criteria are yet. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 3 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Example, the CEO nights receive one millions shares if profits exceed a certain amount. These shares will diluted the interest of other shareholder, but they are only included In the calculation of diluted EPS if. - The performance criteria have been yet and. - The shares have not yet been issued. (a) The order in which dilutive factors should be allowed for. Any entity were have several dilutive instruments. When combined as a group. Some of these instruments may become out dilutive. The diluted EPS should take into account those instruments which dilute the EPS. These instruments can be identified by: (b) Ranking the instruments in order of extra earnings from each new shares. (c) Calculating the diluted EPS starting with the lowest increments EPS. Disclosure An entity should disclose the following: (a) The earning used for basic and diluted EPS. These earning should be reconciled to the net profit or loss for the period. (b) The weighed average number of order shares used for basic and diluted EPS. The two average should be reconciled to each other. Criticism of EPS as a performance measure Performance measure EPS is used by investors and it does affect the market price of shares. However has several important limitations as a performance measures. (a) It ignores inflation apparent growth in earnings may not be real growth. (b) Past performance may not be good indication for future performance. (c) Earning may be affects by entities choice of accounting policies. This makes inter-company campus. a) Contingently issuable shares i.e. shares issuable of certain conditions are yet. Companies difficult Dilution Some commendations think that the TAS 33 requirements for calculating diluting EPS are too complicated. Question 1 Goodwill Company Limited is a listed company which prepares the Financial statements of 31st December. Goodwill Income Statement for the year ended 31st December 2011. Tshs. Sales Cost of Sales Gross profit Other incomes From continuing operations CPA(T) Zachayo N Leonard 0657174882, 0717782882 Tshs. 9,000,000 (5,400,000) 3,600,000 2,200,000 Page 4 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ From discontinuing operations 1,200,000 7,000,000 Operating Expenses Salaries & Wages Profit before interest & Tax Interest on long-term loans: Profit before tax Income tax Net profit for the year 2,400,000 1,200,000 The capital structure at 1st January 2011 were as follows: 8% cumulative preference shares: 30,000 ordinary shares @ Tshs. 2,000 Fully paid up Share premium Reserves (3,600,000) 3,400,000 (360,000) 3,040,000 (360,000) 2,680,000 7,250,000 60,000,000 1,250,000 1,300,000 70,300,000 Required: Calculate the basic EPS (i) Assuming no new issue of ordinary share for the year ended 31st December 2011. (ii) Assuming that 12,000 ordinary shares issued at the market price and full paid up on 1 st July, 2011. (iii) Assuming that after new issue of shares as (ii) above and on 12 th August, made the bonus issue of 9,000 ordinary shares. (iv) Assuming the company made the issues of ordinary shares as (ii) and (iii) above. And on 1st October 2011 made the right issue of 1 new ordinary shares for every 3 held at Tshs. 1,200/= each while the market price of share on 31st September 2011 was Tshs. 2,400. (v) Assuming in additions to above, on 31st October, 2011 made a new issue of 6,000 ordinary shares at market price of Tshs. 2,500 and paid Tshs. 2,000. Question 2 (NBAA MAY 2012) A statement showing the retained profit of Pyuza Ltd for the year ended 31 st December, 2004 is set out below: Tshs. Profit before tax Tshs. 2,530,000,000 Less: Income tax expenses (1,127,000,000) 1,403,000,000 Transfer to reserve (230,000,000) 1,173,000,000 Dividends: Paid preference interim dividend 138,000,000 Paid ordinary interim dividend 184,000,000 Declared preference final dividend 138,000,000 Declared ordinary final dividend 230,000,000 690,000,000 CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 5 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Retained profit 483,000,000 On 1st January, 2004 the issued share capital of Pyuza Ltd was 4,600,000; 6% preference shares of Tshs. 1,000 each and 4,120,000 ordinary shares of Tshs. 1,000 each. Required: Compute the Earnings Per Share (on basic and diluted basis) in respect of the year ended 31 st December, 2004 for each of the following situations. Each of the three situations in (a) - (c) below is to be dealt with separately: Assume where appropriate that the income tax rate is 30%: (a) On the basis that there was no change in issued share capital of the company during the year ended 31st December, 2004'. (4.5 marks) (b) On the basis that the company made a rights issue of Tshs. 1,000 ordinary shares on 1st October, 2004 in the proportion of 1 for every 5 shares held, at a price of Tshs. 1,200. The market price for the shares at close of trade on the last day of quotation cum rights was Tshs. 1,780 per share. (10 marks) (c) On the basis that the company made no new issue of shares during the year ended 31 st December, 2004 but on that date it had in issue Tshs. 1,500,000; 10% convertible loan stock 2008 – 2011. This loan stock will be convertible into ordinary Tshs. 1,000 shares as follows: 2008: 90 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock 2009: 85 Tshs. 1,000 shares for the Tshs. 100,000 nominal value loan stock 2010: 80 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock 2011: 75 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock. (5.5 marks) (Total = 20 marks) Question 3 ABC Company Limited during the year ended 31st December, 2010 made a profit before tax and interest of Tshs. 48,400,000. At 1st January, 2010, the company had Ordinary share capital 104,000 ord. Share @ Tshs. 1000 10% Debenture 12% 10,000 cumulative prefers shares @ Tshs. 1000 Tshs. 104,000,000 Tshs. 24,000,000 Tshs. 10,000,000 On 1st July 2010 made the right issue for 2 new ordinary shares for every 3 ordinary shares held at Tshs. 800. The market price on 30th June 2010 was Tshs. 1,200. On 1st October, 2010 made new issue of 48,000 ordinary issue at the market price of Tshs. 1300 and until 31st December 2010 on Tshs. 975 were paid up. On 31stDecember, 2010. The company had the share options for 24,000 ordinary shares at Tshs. 1200. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 6 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ And 12% cumulative preference share convertible as Tshs. 1000 into 1 ordinary shares. Given the average price per share for the year was Tshs. 1500. Corporate tax rate assuming at 25% Required: Calculate, Basic EPS and diluted EPS. Question 4 During the year of income ended 31st December 2010 the company made profit after interest and tax of Tshs. 18,600,000 but before. Payments of Pref. Share dividend Payment of ordinary share dividend General Reserves appropriation Tshs. 2,400,000 Tshs. 1,200,000 Tshs. 1,500,000 On 1st January, 2010 had 24,000 ordinary shares of which new issue of 10,000 ordinary shares were made on 1st April, 2010 at the market price and full paid up. Followed by bonus issue on 10th July, 2010 for 4500 ordinary shares: On 31st December 2010 The company had 8% convertible bond = Tshs. 25,000,000 and Tshs. 10,000 nominal value convertible into 1 ordinary shares. Share option for 12,000 shares at Tshs. 600/- while the average market price during the year was Tshs. 1,000. Assuming Tax Rate = 30% Required: Calculate Basic EPS and diluted EPS. Question 5 Extracts of Niagara’s consolidated income statement for the year to 31 March, 20x3 are: Sales Cost of sales Gross profit Other operating expenses Finance costs Impairment of non-current assets Income from associates Profit before tax Taxation Profit for the period Shs. 000 36,000 (21,000) 15,000 (6,200) (800) (4,000) 1,500 5,500 (2,800) 2,700 CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 7 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Attributable to: Shareholders of the parent Minority interests 2,585 115 2,700 The impairment of non-current assets attracted tax relief of shs. 1 million which has been included in the tax charge. Niagara paid an interim ordinary dividend of 3c per share in June 20x2 and declared a final dividend on 25 March, 20x3 of 6c per share. The issued share capital of Niagara on 1 April, 20x2 was: Ordinary shares of 25c each shs. 3 million 8% Preference shares shs. 1 million The preference shares are non-redeemable. The company also had in issue shs. 2 million 7% convertible loan stock dated 20x5. The loan stock will be redeemed at par in 20x5 or converted to ordinary shares on the basis of 40 new shares for each shs. 100 of loan stock at the option of the stockholders Niagara’s income tax rate is 30%. There are also in existence directors’ share warrants (issued in 20x1 which entitles the directors to receive 750,000 new shares in total in 20x5 at no cost of the directors. The following share issues took place during the year to 31 March, 20x3. 1 July 20x2; a rights issue of 1 new share at shs. 1.50 for every 5 shares held. The market price of Niagara’s shares the day before the rights was shs. 2.40. 1 October 20x2; an issue of shs. 1 million 6% non-redeemable preference shares at par. Both issues were fully subscribed. Niagara’s basic earnings per share in the year to 31 March, 20x2 was correctly disclosed as 24c. Required: Calculate for Niagara for the year to 31 March, 20x3: (i) The dividend cover and explain its significance (ii) The basic earnings per share including the comparative (iii)The fully diluted earnings per share (ignore comparative); and advise a prospective investor of the significance of the diluted earnings per share figure. Question 6 (NBAA) (a) An Earnings per share are one of the most quoted statistics in financial analysis, coming into prominence because of the widespread use of the price earnings ratio as an investment decision-making yardsticks. Required: CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 8 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Apart from other disclosures, explain why there is a need to disclose diluted earnings per share in financial statements. (5 marks) (a) Wazalendo Limited is a listed company. On 1 st November 2003 its issued share capital was 10,000,000 ordinary shares of Tshs. 600 each and 4,000,000 4%preference shares of Tshs 1,000 each. During the year ended 31 October 2004, the company made a rights offer to its shareholders of three new ordinary shares of Tshs 600 each for every 10 existing ordinary shares held. The offer was fully taken up by shareholders who purchased the new shares for Tshs 3,000 each on 1st May 2004. The fair value of each ordinary share on 30th April 2004 was Tshs 4, 150. At 31 October 2004, the ordinary shareholders of Wazalendo also held options, exercisable between 1 November 2007 and 1st May 2008 to purchase 1, 200,000 ordinary shares at Tshs 2,800 per share. No options were issued during the year ended 31 st October 2004. the average fair value of the ordinary shares during the year was Tshs. 4,200 each. The company paid an ordinary dividend of Tshs 1,040,000,000 and a preference dividend of Tshs 160,000,000 during the year to 31st October 2004. Wazalendo’s draft profit and loss account for the year ended 31 st October 2004 shows the following: (Tshs. 000,000) Operating profit 4,525 Interest payable (329) Profit on ordinary activities before taxation 4,196 Taxation (1,279) Profit on ordinary activities after taxation 2,917 Minority interests (132) Profit for the financial year 2,785 Required: (i) Calculate the basic earnings per share for Wazalendo for the year ended 31 st October 2004. (5 marks) (ii) Calculate the diluted earnings per share for the year ended 31 st October 2004 (5 marks) (iii) Prepare the earnings per share disclosure note for the year ended 31 st October 2004. (5 marks) (Total = 20marks) Note: comparative figured are not required Question 7 XYZ Company during the year ended 31st December 2012. Made profit before interest and tax of Tshs 66,500,000. Provisions for tax is made at Tshs.. 16,000,000. Capital structure of the company of at 1st January, 2012 made of the following:10% Debentures Tshs. 45,000,000 8% Cum Pref. shares @ shs. 100 Tshs. 125,500,000 Ordinary shares @ Tshs. 250 Tshs. 300,000,000 Profit and Loss Tshs. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 9 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ 3,500,000 Tshs. 474,000,000 Required: Calculate basic EPS a) Assuming that there was no change in issued share capital made during the year ended 31 st December, 2012 b) On the basis that the company made a new issue of 400,000 ordinary shares at the market price and full paid on 31st March, 2012. And followed by new issue of 200,000 ordinary shares at the market price but 50% paid up on 30th June, 2012 and the balance remained unpaid to 31st Dec 2012, while bonus issue of 1 for every 5 held were issued on 15 th February, 2012. c) On the basis that the company made only right issue of 2 new ordinary share for every 5 shares held at Tshs. 200/= at 30th June, 2012, and the market price on 20th June, 2012 was Tshs. 270/=. Question 8 NBAA May 2016 Daima Plc has 1,500,000 ordinary shares in issue and profits after tax of TZS.1,250,000,000 (all from continuing operations) for the year ended 30th September 2015. The company also has the following convertible stock: TZS.400,000,000 of 10% loan stock, each TZS.1,000,000 of stock having the right to convert into 2,000 ordinary shares. TZS. 100,000,000 of 12% loan stock, each TZS.2,500,000 of stock having the right to convert into 200 ordinary shares. In additional, it has 500,000 TZS.1,000 10% convertible cumulative preference shares. Each convertible to 1.5 ordinary shares. The tax rate is 30%. Required: Calculate the basic and diluted Earnings per Share for the year ended 30th September 2015. (15 marks) (Total: 20 marks) Conveniently Diluted EPS Dilution is a reduction in Earnings per share or an increase in loss per share resulting from the assumption that convertible instruments are converted, that options or warrants are exercised, or that ordinary shares are issued upon the satisfaction of specified conditions. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 10 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Diluted Earnings per share means an EPs that is reduced due to increase in the number of shares (the denominator) without a proportionated increase in the earnings. (The numerated) A potential ordinary shares, is a financial instrument or other contracts that may entitle it’s holder to ordinary shares. These are ordinary shares likely to come into existence as the results of financial instrument or contracts Why diluted EPS calculated? Diluted EPS provides additional information which is relevant for the existing as well as the potential investors. Existing shareholders will know what the EPS could be in future, on the shares held by them. Accordingly they can decide whether to hold the shares or to sell them. Potential shareholders can decide whether to buy or not using diluted EPS. In general diluted EPS provides the warning signal for both existing shareholders and potential ordinary shareholder Dilutive factors (1) Convertible bonds (2) Convertible preference shares (3) Share options & warrants (4) Partly paid –up shares. Question 9 XYZ Co. has 120,000 Tshs 100 ordinary shares in issue and profits after tax of Tshs 9,600,000/= for the year ended. 31st Dec 2015. Assume corporate tax to be 30% Calculate diluted EPS in the following each situations separately. (a) Assume the company has 10% convertible debenture of Tshs 25,000,000/= and every Tshs 1250 Convertible into 2, Tshs 100 ordinary shares. (b) Assume that the company has 12% convertible preference shares of Tshs 20,000,000 and every Tshs 625 shall be convertible into one ordinary shares. (c) Assume that the company has 40,000 Tshs 100 shares options exercisable at Tshs 125 while average market price per share during the year ended 31 Dec 2015 was Tshs 200. (d) Assume all the conditions above exist at 31st Dec 2015 calculate diluted EPS Question 10 (a) Given the capital structure of the company XYZ Co on 1st Oct 2010 made up of the following 8% debentures 150,000,000 10% Cum. Pref. shares @ Tsh 100 200,000,000 Ordinary share capital @ Tsh 200 500,000,000 CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 11 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ During the year ended 31st Sept 2011. The company made profit before interest & tax of Tshs 122,000,000 Assume tax rate = 20% Required Calculate basic EPS (b) If on 31st Dec 2010 the company issue share ordinary shares; 500,000 shares at market price and was full paid on the allotment stage. But on 31st March 2011, the company made another issue of 500,000 shares at market price of Tshs 300/= only Tshs 150 was paid until on reporting date 31st Sep 2011. Also the company made bonus issue on 30th June 2011 for one Tshs 200 ordinary share for every five Tshs 100 ordinary share held on 1st Oct 2010, utilizing general reserves Required Calculate basis EPS (c) Assume XYS Co made only eight issue on 31st March 2011 for Tshs 100 ordinary share for every seven Tshs 200 ordinary shares held at Tshs 200. If market price before right issue was Tshs 300 Calculate basis EPS (d) Consider part (c) above. - On 31st Sep 2011, the company held the share options of 400,000 shares of exercise price of Tshs 240 given average market price was Tshs 300 - And the company held, the convertible 8% debenture Tshs 150,000,000 convertible Tshs 1000 nominal value for six Tshs 200 ordinary shares. 12% Cum pre shares convertibles as Tshs 1000 nominal value for eight, Tshs 200 ordinary shares. Assume corporate tax rate 20% Calculate Dilute EPS CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 12 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ QUESTION 11 IAS 33: Earning per share sets out the requirements for calculating and disclosing the basic earnings per share figure for quoted entities. The following figures appeared in the Consolidated Statement of Profit or Loss and Other Comprehensive Income of Precious Plc for the year ended 31 st July 2016, together with comparative for 2015: Profit before taxation Taxation on profit Profit for the year Other comprehensive income-revaluation gain on land Total comprehensive income for the period Profit for the year attributable to: Owners of the parent On-controlling interest Profit for the year Total comprehensive income for the year attributable to: Owner of the parents Non- controlling interests Total comprehensive income for the year 2016 400 (75) 325 30 355 2015 300 (60) 240 10 250 280 45 325 210 30 240 310 45 355 220 30 250 The following figures are taken from Precious’s Statement of Financial Position as at 31 st July 2016, together with comparative for 2015: 2016 2015 Equity share capital of TZS 0.50 each 460 200 4% Preference shares-non-redeemable, non-cumulative 100 100 Share premium 215 60 Retained earnings 688 570 Other equity reserves 90 60 Non-controlling interests 85 40 Total equity 1,638 1,030 During the year ended 31st July 2016, the following changes took place to the issued share capital of Precious Plc: i. 100 million equity shares were issued in conjunction with the acquisition of another business. These issued at full market price at date of issue, 1 st November 2015 ii. 150 million ordinary shares were issued for cash to existing shareholders on 1 st February 2016. The issue price was TZS 1.50 per share, which represented a discount of 25% on the traded price immediately before the issue (TZS 2). CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 13 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ iii. On 31st July 2016, a bonus issue of 270 million shares was completed, capitalizing TZS 135 million of retained earnings. Also on this date, the preference dividend due for the year, and an equity dividend of TZS 23 million were paid. Required: (a) Discuss the significance of the Earning Per Share (EPS) figure to the analysis of company performance. Why is it important to have an accounting standard in this area? (b) Applying the requirements of IAS 33: Earning Per Share to the information above, calculate the EPS for the year 31 st July 2016 and the comparative figures for 2015 to be reported in the 2016 financial statements. The EPS figures originally reported in 2015 was TZS 0.525. (20 marks) SUGGESTED ANSWER (a) Significance of the earnings per share figure. Earnings per share (EPS) is one of the most widely watched measures of company performance. As such it is the measure that is subject to most intense efforts to maximize its level and its growth. It is superior to other measures on many levels, but has some limitations also. EPS gives a way to measure a company’s profits relative to the number of shares in issue. It is argued that as owners hold equity shares, it is more relevant to them to know how much profit each share has earned than to know the overall profit figure. EPS feed into the price/earnings ratio, one of the most important stock market measures of value. This gives an estimate of the number of years it would take for an investment in an equity share to return itself in earnings terms, assuming current performance continues into the future. It is essential that such an important measure of performance have clear guidelines regarding its calculation. IAS 33 Earnings per Share gives us a standardized method of calculating both earnings, and the number of shares. Many investors feel that other measures are more appropriate, and that the IAS 33 published, as the IAS 33 figure gets equal or greater prominence. There is a danger in relying on a single measure of performance, as no single measure can encapsulate all aspects of an entity’s performance. Also, there is a danger that EPS, may be seen by unsophisticated investors as a definite exact number, when in reality it is subject to all the accounting estimates and judgment that are necessary in preparing a set of financial statements. Despite these fears, it is generally agreed that IAS 33 gives a very fair method of calculating EPS, and that the consistency it offers is of value to the investor and analyst. (b) Earning relevant to 2016 EPS calculation In class Profit for the year (attributable to owners of the parent) CPA(T) Zachayo N Leonard 0657174882, 0717782882 TSHS (Million) 280 Page 14 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Less preference dividends (100*4%) IAS 33 earnings (4) 276 Number of equity share in issue (weighed average) for year ended 31 July 2016. Date 1 Aug 2015 1 Nov 2015 1 Feb 2016 31 July 2016 31 July 2016 No. of Share (m) 400 +100 = 500 +150 = 650 +270 = 920 Total Time TERP Weight Weighting 3/12 2/1.885 3/12 2/1.885 6/12 Bonus Issue W. Av. No. Weighting 920/650 920/650 Of share 150.17 187.72 920/650 460.00 N/A 797.89 1 Feb 2016: rights issue at discount – calculation of Theoretical Ex – Rights Price (TERP) No. of share in issue prior to rights issue 500 Tsh.2.00 Tsh.1,000 (m) No. of share issued during right issue 150 Tsh.1.50 Tsh.225 Total no. of shares after rights issue 650 Tsh.1.885 Tsh.1,225 All shares in issue prior to the rights issue are weighted by a bonus fraction equal to the ex-rights price (prior to the rights issue) divided by the TERP (2.00/1.885) 31 July 2016: bonus issue – calculation of bonus fraction No. of share in issue prior to bonus issue 650 No. of shares in issue after bonus issue 920 Bonus fraction = 920/650 Weighted average number of shares in issue for year ended 31 July 2016 = 797.89 Million Basic EPS 276/797.89 Tshs.0.3459 Previous year’s EPS figures need to be restated to reflect the distorting effect of issues of shares below market value. This is achieved by multiplying the previously calculated EPY by the inverse of the bonus fraction. 2015 EPS restated Tshs0.525*1.885/2*650/920 = Tshs 0.3496 CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 15 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ QUESTION 12 On I st June 2016, the chief executive of Marhaba Company (Marhaba), Mr. Mandaro, retired from the company. The ordinary share capital at the time of his retirement was 6 million shares of TZS. 1,000 each. Mr. Mandaro owns 52% of the ordinary shares of Marhaba and the remainder is owned by employees. As an incentive to the new management, Mr. Mandaro agreed to a new executive compensation plan which commenced after his retirement. The plan provides cash bonuses to the board of directors when the company's earnings per share exceeds the normal earnings per share which has been agreed at TZS.500 per share. The cash bonuses are 20% of the profit generated in excess of that required to give an earnings per share figure of TZS.500. The new board of directors has reported that the compensation to be paid is TZS.360 million based on earnings per share of TZS.800 for the year ended 31 st May 2017. However, Mm Mandaro is surprised at the size of the compensation as other companies in the same industry were eithér breaking even or making losses in the period. He was anticipating that no bonus would be paid during the year as he felt that the company would not be able to earn more than normal earnings per share of TZS.500 Mr. Mandaro, who had taken no active part in management decisions, decided to take advantage of his role as non-executive director and demanded an explanation of how the earnings per share of TZS.80() had been reached. His investigation revealed the following information: i. The company received a grant from the government of TZS.5 billion towards the cost of purchasing a non-current asset of TZS.15 billion. The grant had been credited to profit or loss in a total and the non-current asset had been recognized at TZS. 15 billion in the Statement of Financial Position and depreciated at a rate of 10% per annum on the straight line basis. The directors explained that current thinking by the International Accounting Standards Board (IASB) was that the accounting standard on government grants was conceptually wrong because it misstates the assets and liabilities of the company and hence, they were following approach which has recently been advocated in a recent discussion paper. ii. Shortly after Mr. Mandaro had retired from the company, Marhaba made an initial public offering of its shares. The sponsor of the issue charged a fee of TZS.300 million. The fee was paid by issuing 100,000 TZS. 1,000 ordinary shares at a market value of TZS. 120 million and by cash of TZS.180 million. The directors had charged the cash paid as an expense in the Statement of Profit or Loss. Further, they had credited the value of the shares issued to the sponsor in the Statement of Profit or Loss for the year as they felt that the shares were issued for no consideration and that, therefore, they should offset the cash paid by the company. The public offering was made on I st August 2016 and involved vesting four million ordinary shares of TZS. 1,000 at a market price of TZs.l,200 per share (exclusive of the sponsor's shares). Mr. Mandaro and other current shareholders decided to sell three million of their shares as part of the offer, leaving one million new shares to be issued. The cost of issuing shares are to be regarded as an element of the net consideration. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 16 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ iii. Marhaba had made a 1 to 4 right issue on 30 th June 2017. The cost of the share was TZS. 1,600 per share and the market price was TZS.2,000 per share before the right issue. The directors had ignored this transaction because it occurred after the year end but they intend to capitalize retained earnings to reflect the bonus element of the rights issue in the financial statements for the year ending 3 1 st May 2018. The financial statements for the previous year have not yet being approved. The directors had calculated earnings per share for the year ended 3 1 st May 2017 as follows: Profit after tax TZS.4.8 billion Ordinary shares of TZS. 1 ,000 6,000,000 Earnings per share TZS.800 Mr. Mandaro was concerned over the way that earnings per share had been calculated by the directors ånd also he felt that some of the above accounting practices were at best unethical and at worst fraudulent. He therefore, asked your technical and ethical advice on the practices of the directors. Required: a) Draft a report summarizing the correct treatment of the matters above and advise Mr. Mandaro as to whether earnings per share has been accurately calculated by the directors. Include in your report a revised calculation when this differs from the directors' calculations. b) Briefly discuss whether or not the directors may have acted unethically in the way they have calculated earnings per share. SUGGESTED ANSWER Advice to Mr. Mandaro on the calculation of Earnings per share From: Consultant Introduction: Basis of calculating EPS Earnings per share (EPS), is a widely used measure of financial performance. Detailed guidance on its calculation and on presentation and disclosure issues is given in IAS 33 Earnings per share. Basic EPS calculation is obtained by diving profit attributable to ordinary shareholders (numerator) to weighted average number of ordinary shares outstanding during the period (denominator). While the denominator is relatively difficult to manipulate, the selection of accounting policies designed generally to boost the earnings figure, may be possible and hence earnings per share may be manipulated. The analysis of the observations noted is as follows: (i) Government grant IAS 20 Accounting for government grants and disclosure of government assistance allows two methods of accounting for government grants. Net the grant off against the cost of the asset and depreciate the net figure Carry the grant as a deferred credit and release it to income over the life of the asset. The grant should therefore be removed from the statement of profit or loss and other comprehensive income. Only TZS 500 million (TZS 5 billion ÷ 10 year) should be credited to income; the balance of TZS 4.5 billion should be shown as a deferred credit or deducted from the cost of the asset. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 17 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ (ii) Share Issue In the calculation of EPS, the directors have used the number of shares in issue when Mr. Mandaro retired from the company (6 million). They have not taken into account the new issue of shares made at the initial public offering. The number of new shares issued is one million plus the sponsor’s shares of 100,000. This needs to be time apportioned (the shares were in issue for ten months) and added to the denominator of the EPS calculation. The treatment of the issue costs is also incorrect. IAS 39 states that transaction costs, defined as incremental external costs directly attributable to an equity transaction, should be accounted for as a deduction from equity. It was therefore incorrect to credit the value of the shares to profit or loss and likewise incorrect to charge the cash paid as an expense in profit or loss. The accounting entries should have been as follows: Dr. Retained earnings/share premium TZS 300 million Cr. Cash TZS 180 million√ Share capital TZS 100 million√ Share premium TZS 20 million √ (iii) Rights Issue The right issue took place after the company’s year-end. The proceeds of the rights issue were not available for use during the accounting period. It would not therefore be appropriate to adjust EPS to reflect any part of the rights issue. However, an adjustment needs to be made for the bonus element in the rights issue, since this is deemed to affect the number of shares, and hence EPS for all accounting periods. The bonus element is = The theoretical ex right price (TERP) is: Initial holding: 4 x 2,00 = 800 Rights issue: 1 x 1,600 = 1,600 5 9,600 TERP = bonus shares are = = TZS 1,920 * No. of shares in issue Revised EPS calculation i/ Revised earnings Profit per directors (1) Government grant taken to deferred income Credited to income in year (2) Cash paid TZS million 4,800 (5,000) CPA(T) Zachayo N Leonard 0657174882, 0717782882 500 180 Page 18 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ Shares issued to sponsor Revised earnings Revised number of shares Per directors Additional shares issued = 1,100,000* 10/12 Bonus shares (2000/1920-1)*6,916,667 Total Revised number of shares Revised EPS (360 mill/7,204,861 (b) (120) 360 6,000,000 916,667 6,916,667 288,194 7,204,861 TZS 49.97 It is not always easy to determine whether creative accounting of this kind is deliberate or whether it arises from ignorance or oversight. The assessment of whether directors have acted ethically is often a matter of the exercise of professional judgement. In factual term when the correct accounting treatment is used, an earnings per share of TZS 800 is converted into a mere TZS 50 per share. Since the directors are entitled to a cash bonus for an EPS of above TZS 500, there would appear to be a strong incentive for them to select accounting policies designed to boost it. The directors’ explanation for their treatment of the government grant, issue of shares and rights issues may simply reflect lack of knowledge on the part of directors, rather than unethical accounting. It is more likely, therefore, that the directors were confused about the appropriate treatment and should be allowed the benefit of any doubt. However the possibility of deliberate manipulation cannot be completely ignored. Conclusion On the facts of the case, accounting standards have not been followed, and generally in a manner likely to boost EPS. Accusations of fraud should not be made hastily without taking legal advice. As suggested in (i) above, in practice there should be internal controls to ensure that the directors should be made aware of their responsibility for the accuracy and fairness of the financial statements and obligation to apply accounting standards. CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 19 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ QUESTION 13 Parapanda is a listed company. On 1st November, 2006 its issued share capital comprised of 10 million ordinary shares of shs. 6 each and 4 million – 4% preference shares of shs. 10 each. During the year ended 31st October 2007 the Company made a rights offer to its shareholders of three (3) new ordinary shares of shs. 6 each for every ten (10) existing ordinary shares held. The offer was fully taken up by shareholders, who purchased the new shares for shs.30 each on 1st May, 2007. The fair value of each ordinary share on 30 th April 2007 was shs. 41.50. On 31st October 2007, the ordinary shares of Parapanda Company also held options exercisable between 1st November 2009 and 1st May 2010 to purchase 1,200,000 ordinary shares at shs. 28 per share. No options were issued during the year ended 31 st October 2007. The average fair value of the ordinary shares during the year was shs. 42 each. Parapanda Company limited paid an ordinary dividend of shs. 10,400,000 and a preference dividend of shs. 1,600,000 during the year to 31 st October 2007. Parapanda Company Limited Income Statement for the year ended 31st October 2007. Operating profits 45,250,000 Interest payable (3,290,000) Profits on ordinary activities before tax 41,960,000 Tax (12,790,000) Profits on ordinary activities after tax 29,170,000 Minority interest (1,320,000) Profit for the year 27,850,000 Required: (a) Calculate the basic earnings per share for Parapanda Company Limited for the year ended 31st October 2007. (9 marks) (b) Calculate the diluted earnings per share for the year ended 31st October 2007. (7 marks) CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 20 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ QUESTION 14 a) Dabaga Inc was incorporated on January 1, 2012, with an equity of TZS 4.0 million. The statement of financial positions of the entity at the beginning and end of the first financial year were as follows: Beginning TZS. 000 Assets Property , plant and equipment Inventory receivables Equity and liabilities Share capital Accumulated profit Borrowings End TZS. 000 60,000 30,000 50,000 140,000 50,000 40,000 60,000 150,000 40,000 100.000 140,000 40,000 10,000 100,000 150,000 The statement of comprehensive income for the first year reflected the following amounts: TZS. 000 Revenue 800,000 Operating expenses (750,000) Depreciation of plant and equipment (10,000) Operating profit 40,000 Interest paid (20,000) Profit before tax 20,000 Income tax expenses (10,000) Profit after tax 10,000 The rate of information was 120% for the year. The inventory represents two months` purchases, and all statement of comprehensive income items accrued evenly during the year. Required: Restate the above financial statements (the statement of comprehensive income and statement of financial position) using reliable price index in such a hyperinflationary situation. (8 marks) (Total 20 marks SUGGESTED ANSWER The financial statements can be restated to the measuring unit statements of financial CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 21 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ position date using reliable price index, as follow: Statement of Financial Position Recorded Tshs. 000 Assets Property, plant and equipment Inventory (calculation a) Receivables Equity and liabilities Share capital Accumulated profit Borrowings Restated Tshs. 000 Calculations 50,000 40,000 60,000 150,000 110,000 41,905 60,000 211,905 2.20/1.00 2.20/2.10 40,000 10,000 100,000 150,000 88,000 23,905 100,000 211,905 2.20/1.00 Balancing Statement of comprehensive income Recorded Recorded Tshs. 000 Tshs. 000 Revenue (calculation b) 800,000 1,100,000 2.20/1.60 Operating expenses (750,000) (1,031,250) 2.20/1.60 Depreciation (calculation c) (10,000) (22,000) 2.20/1.0 Interest paid (20,000) (27,500) 2.20/1.60 Income tax expenses (10,000) (`13,750) 2.20/1.60 Net profit before restatement gain 10,000 5,500 Gain arising from inflation adjustment 18,405 Balancing figure Net profit after restatement gain 23,905 Calculations: i) Index for inventory ii) Inventory purchased on average at November 30 Index at the date = 1,000 + (1.20 x 11/12) = 2.1 Index for income and expenses iii) Average for the year = 1.00 + (1.20/2) = 1.60 Index for depreciation Linked to the index of property, plant and equipment = CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 22 Cornerstone Financial Consultants. CPA Reviews ___________________________________________________________________________ QUESTION 15 A statement showing the retained profit of UPTAKE Ltd for the year ended 31 st December 2004 is set out below. Tshs. Tshs. Profit before tax 2,530,000,000 Less: Income tax expenses (1,127,000,000) 1,403,000,000 Transfer to reserve (230,000,000) 1,173,000,000 Dividends: Paid preference interim dividend 138,000,000 Paid ordinary interim dividend 184,000,000 Declared preference final dividend 138,000,000 Declared ordinary final dividend 230,000,000 690,000,000 Retained profit 483,000,000 st On 1 January, 2004 the issued share capital of UPTAKE Ltd was 4,600,000;6% preference shares of Tshs. 1,000 each and 4,120,000 ordinary shares of Tshs. 1,000 each. Required: Compute the earnings per Share (on basic and diluted basis) in respect of the year ended 31 st December, 2004 for each of the following situations. Each of the three situations in (a) – (c) below is to be dealt with separately: Assume where appropriate that the income tax rate is 30% (a) On the basis that there was no change in issued share capital of the company during the year ended 31st December, 2004. (4.5 marks) (b) On the basis that the company made a rights issue of Tshs. 1,000 ordinary shares on 1st October, 2004 in the proportion of 1 for every 5 shares held, at a price of Tshs. 1,200. The market price for the shares at close of trade on the last day of quotation cum rights was Tshs. 1,780 per share. ( 10 marks) (c) On the basis that the company made no new issue of shares during the year ended 31st December, 2004 but on that date it had in issue Tshs 1,500,000; 10% convertible loan stock 2008 – 2011. This loan stock will be convertible into ordinary Tshs. 1,000 shares as follows: 2008: 90 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock 2009: 85 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock 2010: 80 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock 2011: 75 Tshs. 1,000 shares for Tshs. 100,000 nominal value loan stock (5.5 marks) CPA(T) Zachayo N Leonard 0657174882, 0717782882 Page 23