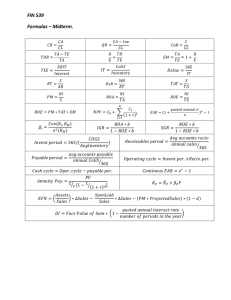

3BE322 – Corporate Finance Textbook Notes Week 2 CF statement: 3 components 1. Operating activities 2. Financing activities: focuses on how a firm raises capital and pays it back to investors through capital markets Paying cash dividends Adding or changing loans Issuing or selling more stock 3. Investing activities Changes in assets Change in equipment Indirect CF: actual cashflows do not need to be known Direct CF: actual cashflows are known amounts Changes in working capital = currents assets – current liabilities Operating CF: net income + non-cash expenses – change in working capital Depreciation is added back to CF statement since it is a non-cash expense and is recorded (removed) on the income statement Depreciation is no cash flow Cash flow = net income +/- revenue expenses, credit transactions Example from HW: Week 2: Textbook notes Chapter 1: Goals and Governance of the Firm Corporations need real assets to carry on business. To buy them the corp sells claims on the assets and on cash flow they will generate called financial assets or securities Investment decision = purchase of real assets. How to spend decision Financing decision = sale of financial assets. How to raise capital decision Capital budgeting/capital expenditure (CAPEX) decisions made my financial manager: include major projects approved for investment tangible (new stores) and intangible (marketing, R&D) Vary in timeline for returns. Longer timeline requires larger profit. Shareholders are equity investors who contribute to equity financing Capital structure decision: decision between equity financing or debt financing Debt financing Borrow from banks Borrow by issuing bonds Which country should it borrow from? How long should it borrow for? Debt has its advantages but too much debt can lead to bankruptcy. Risky with interest rates Equity financing (2 ways) Issue new shares of stock (investors give up cash for these shares) Take cash flow generated from existing assets and reinvest the cash in new assets Extra cash held by corp is either held in reserves for future or paid back to shareholders Shareholders will vote to invest in a project if the return is higher than what they would make if invested personally on the stock market, for similar risk Hurdle rate or cost of capital is the minimum acceptable rate of return or opportunity cost of capital o the minimum rate of return or profit a company must earn before generating value Opportunity cost of capital is the expected return that investors can achieve in financial markets at the same level of risk. Payout decision: decision to pay dividends or repurchase shares Market capitalization = market value Corporation: a legal entity -pay taxes, can’t vote, formed based on articles of incorporation -shareholder have limited liability – can’t be held personally liable for corp -board of directors choose top management -can live forever in principle -Shareholders are the owners but cannot control what managers do except through the BOD Closely held corp means shares are not publicly traded. Different from a public company CFO’s: deeply involved with financial policy and financial planning, constant contact with CEO Treasurer: below CFO. Responsible for short term cash management, currency trading, financing transactions and bank relationships Controller: below CFO. Manages company’s internal accounting systems and oversees preparation of financial statements and tax returns Shareholder’s financial objective: Maximize the current market value of shareholders investment in the firm Should firms be managed for shareholders or all stakeholders? -will differ depending between different countries Agency problem: arise when managers (agents) work for principals (shareholders) Agency costs occur when 1. Managers do not attempt to maximize the firms value 2. Shareholders incur costs to monitor the managers and constrain their actions Subprime: mortgage loan made to home buyers with weak credit Corporate governance Legal and regulatory requirements o Managers have a legal duty to act responsibly and in the interest of investors Compensation Plans o Incentive schemes that produce big returns to managers if shareholders gain, but are valueless is they do not Board of Directors o Elected by the shareholders and has duty to represent them. More than half now are independent to the corp (have no managerial duty or affiliation) Monitoring o Monitored by security analysts Takeovers Shareholder pressure Chapter 28.1-28.2: Financial Analysis Balance sheet sections are listed most liquid to least Long term assets MV is not shown. Recorded as original cost minus fixed annual depreciation Net working capital = Current assets – current liabilities Income Statement How profitable the firm has been over the past year EBIT = Revenues (Net Sales – COGS) – Expenses – Depreciation Week 3: Textbook Notes Chapter 28.3-28.8: Financial Analysis Market capitalization= stock price x shares outstanding Book value will show shareholders cumulative investment in the company Market value added = MV of firms shares (revenue) – what shareholders have invested (cost) Market-to-book ratio: how much value has been added for each dollar that shareholders have invested Used to compare companies of different sizes and capital Market value performance drawbacks MV of company’s shares reflect investors expectations for future performance Can’t look up the MV of privately owned companies whose shares are not traded. Income statement does not include cost of capital as an expense… so we use EVA to measure profit EVA = (after-tax interest + net income) – (cost of capital x capital) Economic value added: profit after deducting ALL costs, including costs of capital More assets to work with, opportunity for greater EVA Penalizes managers who keep too much cash ROC : total profits the company has earned for its debt and equity holders, divided by the amount they have contributed Use after-tax interest and net income. Subtracted the tax shield on debt to calculate the income that the company would have earning with all-equity financing May use average total capital ROC = (after-tax interest + net income) / total capital Book rates of return: ROC, ROA, ROE WACC includes an adjustment for the interest tax shield Picks up tax advantages of debt financing ROE = (net income) / (equity) (EAT) / (E) ROA = (after-tax interest + net income) / (total assets) (EBIT) / A ROIC Return on invested capital (NOPAT)/C => Net Operating Profit After Tax One factor of profitability? How it efficiently it uses its many types of assets : Asset turnover ratio = (sales) / (total assets at start of year) How much sales are generated from each dollar of total assets Measures how hard the firm’s assets are working. A low ratio means the firm is not efficiently using its assets to generate sales. Want a larger # Retail aims for 2.5 or more and utilities aims for 0.25-0.5 Inventory turnover ratio = (COGS) / (Inventory at start of year) Efficient firms will only hold a relatively small level of inventories of raw materials and finished good, and turn over those inventories rapidly A low ratio would indicate weak sales and excess inventories. High rate means goods are sold faster. Between 5-10 is ideal. For industries with perishable goods it will be higher. Average days in inventory = (inventory as start of year) / (daily cost of goods sold) How many days of output are represented by inventories “DSI”: used for efficiency of sales. High DSI can mean firm is not properly managing its inventory or inventory is difficult to sell Receivables turnover = (sales) / (receivable at start of year) Receivables are sales for which the firm has not yet been paid If customers are quick to pay, turnover will be high High ratio often indicates an efficient credit department. Could also mean they have strict fast credit policy which could hinder sales Average collection period = (receivables at start of year) / (average daily sales) Average length of time it takes customers to pay their bills Smaller # is better. Small period would indicate efficient credit department or strict policy Profit margin = (net income) / (sales) It is useful to add back the debt interest to net income for firms using some debt financing => operating profit margin Operating Profit margin = (after-tax interest + net income) / (sales) Du Pont System ROA = asset turnover x operating profit margin Helps to identify constraints firms may face in achieving higher return on assets Dupont without leverage portion Leverage ratios show how much financial leverage a firm can take on Long-term debt ratio = (long-term debt) / (long-term debt + equity) “long term capital” Decimal answers show how many cents to the dollar High ratios (above 1) can mean the company may be overleveraged and could default on loans Long-term debt-equity ratio = (long-term debt) / (equity) High ratio is generally not good. High ratio could mean the company will have difficulty paying off its debts. Lower ratio means larger equity financing (less risky?) Total debt ratio = (total liabilities) / (total assets) Debt ratios make use of book values rather than market values Lower ratio is better but need to have some debt. High ratio could make it hard to borrow money Times-interest-earned ratio = (EBIT) / (interest payments) Banks prefer to lend to companies whose earnings cover interest payments with room to spare However, doesn’t tell us if the firm has enough cash to pay off its debt as it comes due Cash coverage = (EBIT + depreciation) / (interest payments) Adding back depreciation since it is not a cash expense. EBIT + dep is cash available Useful to determine the amount of cash available to pay interest expense Leverage on the return of equity: Raising cash by borrowing increases interest payments and reduces profit. On the other hand, if a firm borrows instead of issuing equity , it has fewer equity holders to share profits with. Du Pont: ROE version Product of the two middle term is the return on assets First and fourth terms do depend on the debt-equity mix Credit analysts and bankers look at several measures of liquidity, to ensure the firm has the cash to repay them These measures can quickly become outdated since liquid assets change so frequently High levels of liquidity may also indicate sloppy use of capital. EVA may help because it penalizes managers who keep more liquid assets than they need Net working capital to total assets ratio = (Net working capital) / (total assets) Current assets include cash, marketable securities, inventories and AR Shows the amount of additional funds available for financing operations Current Ratio = (current assets) / (current liabilities) Changes in current ratio can be misleading. o EX: firm borrows large sum from bank and invests in marketable securities. CL and CA both rise. So NWC is unaffected but the ratio is affected. Sometimes preferrable to net short-term investments against short-term debt when calculating current ratio Quick (Acid test) ratio = (cash + marketable securities + receivables) / (current liabilities) Cash Ratio = (Cash + marketable securities) / (current liabilities) Same as quick ratio except it removes receivables – only most liquid assets A low cash ratio may not matter if a firm can borrow on quick notice Doesn’t really matter if a bank actually borrowed or just has the guaranteed line of credit when it needs to do so Doesn’t take into account firms “reserve borrowing power” Interpreting financial ratios Varies from industry to industry Limit comparison to firms main competitors Prepare common size financial statements Lecture Week 2: Financial Analysis Sources of Data Accounting records and financial statements Managerial accounting Rating agencies o rating agencies are very important o Offer a lot of information which reflect behaviour Markets Analysts What are we interested in? Efficiency/Profitability Activity o Typically sales to assets. How active you are with your assets Leverage Liquidity o Sufficient cash Market opinion Methods and techniques Horizontal analysis – an asset class over time. Analyzing the BS horizontally Vertical analysis – the structure by one year. Analyzing the BS vertically Ratios – measures DuPont and decomposing of measures EVA MVA Absolute vs. relative measures, other techniques o What is visible percentages and then to compare it to the whole picture. $500 2021 goes to $1000 in 2022. This is a 100% increase, but really the revenue is $3M so it is not relative? Quality of data (inputs) is crucial for good analysis and general judgement -GIGO: garbage in garbage out Profit absolute measures: EAT: Earnings after tax (net profit/loss) EBT: Earnings before tax (gross profit/loss) EBIT: Earnings before interest and tax (gross profit unaffected by interest and interest tax shield) NOPAT = EBIT*(1-T) … Net operating profit after tax (net profit unaffected by interest, sometimes called NOPLAT … Net operating profit less adjusted taxation EBITDA: Earnings before interest, tax, depreciation and amortization Profitability ratios: ROE = EAT/E… Return on equity ROA = EBIT/A … return on assets ROS = EAT/S … return on sales ROIC = NOPLAT/C … return of invested capital, where C = D+E Liquidity ratios: L1 = CA/Payables L2 = (Cash + Receivables)/Payables L3 = Cash/Payables o Where CA is Current Assets Activity ratios: TA = S/A … Turnover of Assets TFA = S/FA … Turnover of Fixed Assets TCA = S/CA … Turnover of Current Assets TI = S/Inventory … Turnover of Inventory Leverage ratios: D/E D/A D/C=D/(C+D) E/C=E/(E+D) Interest cover ratio = EBIT/Interests Where C is Capital Invested = D+E Market measures P/E = spot price of the stock / EPS EPS = Earnings per shares = EAT/# of stocks MVA = Market value of stock – book value EVA – Economic Value Added Economic value added (sometimes called economic profit , “EP”) EVA=NOPLAT – WACC*C … excess of the net operating profit over investors expected cost of capital. Equivalent counting of EVA. DuPont Decomponing Lecture Week 3: Short term financial management and working capital management working capital management Basic terms Working capital = current assets . They are the same thing Net working capital= current assets – payables Noncash working capital = current assets – cash Non cash net working capital = current assets – cash – payables Current assets and its units Short term liabilities => mostly payables Elementary notes Cash cycle – industry x retail Typical reasons of delaying of cash cycle Accounting items of STL and CA x items coherent with NWC meaning What is the optimal level of NWC? The less the better? Or not? Why is the NWC estimate relevant in long term planning, financing and valuation We need a feasible financial plan of our strategic option in question NWC estimate affects FCF (free cash flow) estimate and therefore NPV Inventory Management Inventory formation – time and space discrepancy between claiming and item and its availability Major factors determining amount and structure – industry, competitors strategy, organizational architecture, capital costs, choice of fixed and off-balance assets.. Models for inventory optimizing 1. Models for managing one homogeneous inventory item 2. Managing heterogeneous set of items Inventory management and optimism models in independent demand situations 1. Inventory under conditions of certainty a. Basic model b. Impact of the delay and impact of not continuous consumption c. Looking for the optimal delivery volume (Baumol Model) d. Impact of quantity discounts on optimal delivery volume 2. Inventory under conditions of uncertainty a. Particular reasons of volatility b. Looking for the total volatility and safety inventory Inventory management levels and optimization – variables and levels Optimization => Baumol model Presumptions: o Existence of 2 groups of supply-related costs HC – inventory holdings costs RPC – inventory replenishment costs o Optimisation lies in minimising of TC function (total costs), for independent variable q (delivery volume) Receivables Management Determinants of receivables: output market characteristics, competitive strategy – ex: sales conditions Sales conditions o Advance payment o Payment delivery o Provision of commercial credit o Combination of the above Options 3 and 4 lead to receivables Receivable management – tools New customers x loyal customers – condition differentiating Supplier credit limits (2 levels – before due date and after due date) Payment conditions (interests on delayed payment) Invoicing and documents evidencing existence of receivables and good records in general (about customer payment habits, age of receivables, status of receivables) Sale of the receivable Collection agency – helps (in a similar way as a lawyer) recover receivables on commission Insurance company – insures a credit up to a certain amount and according to the level of credit risk Factoring company – takes over the receivable paying you its amount less interest and fee for taking over responsibility for recovery. It sometimes also takes over the risk of non-payment Impacts of bad debts Loss of: Costs of merchandise VAT paid on sales Corporate income tax paid Margin (to cover overheads & generate profit) Loss reduction: Reduction of corporate income tax by creating a provision Impact of lately paid receivables Loss of capital costs used to finance receivables Liquidity management Objectives: Ensure liquidity – permanent ability to pay due liabilities at low cost (real and opportunity costs) Individual objectives o Due liabilities are paid on time o Elimination of loans and financial assets concurrence o Financial asset yield interest o Short-term financing costs are minimised, return on financial assets maximised Theoretical approaches – Baumol Model Similar as for inventory – it is de facto extended version for cash balance management Presumptions o You hold cash reserve o You hold government bonds o You sell bonds when the reserve runs out o Costs related to cash reserve (cost of holding) represent lost interest on bonds o Costs related to order (cash replenishment) represent a fixed administration expense related to one sale of bonds (regardless of the sale volume) More important to know the concept/principle and outcome of optimization rather than the specific math and formulas Advance payments: ex: customized order Week 4: Textbook Notes Chapter 30: Working Capital Management Working Capital is short term assets and liabilities Net Working Capital = current assets – current liabilities Current assets include Cash and short-term securities Account receivables Inventory Cash manager has 2 principal problems 1. How much cash the firm needs to retain and therefore how much can be invested in interest bearing securities 2. Ensure cash payments are handled efficiently a. Deposited as quickly as possible Inventories Raw materials, work in process, finished goods Inventory trade off: between carrying costs and order costs o Smaller orders have less carrying costs but more frequent order costs May not meet unexpected increase in demand o Larger orders have greater carrying costs for storage but fewer order costs Ordering more than the stores immediate needs Economic order quantity: optimal order size Carrying costs: cost of storing goods + cost of capital tied up in inventory Manage inventory levels by waiting until they reach some minimum level and then replenish them by ordering a predetermined quantity When carrying costs are high and order costs are low it makes sense to order in larger quantities less frequently Inventory levels do not rise in direct proportion to sales “Just-in-time approach” or “made to order” Credit management B2B is bulk of unpaid bills or trade credit Remainder of accounts receivable is consumer credit 5 sets of questions for management of trade credit 1. How long are you going to give customers to pay their bills? Are you prepared to offer cash discount for prompt payment? 2. Do you require some formal IOU from the buyer or do you just ask him to sign a receipt? 3. How do you determine which customers are likely to pay their bills 4. How much credit are you prepared to extend to each customer? Do you play it safe by turning down any doubtful prospects? Or do you accept the risk of a few bad debts as part of the cost of building a large regular clientele 5. How do you collect the money when it becomes due? What do you do about reluctant payers or deadbeats? COD = cash on delivery CBD = cash before delivery Progress payments Different industries have different payment periods. Consumer durables may be a month, perishable goods may be a week. Longer periods for low-risk businesses, large accounts, longer to check quality of goods or if goods are not easily resold. “2/10, net 30” is a term to refer to offering cash discount for sooner payments. 2% discount if paid in 10 days from total 30 days Often frequent bought items will all be due as “one bill” at EOM (end of month). “8/10 EOM, net 60” Clear commitment from the buyer before you deliver goods can be done through a commercial draft Bankers acceptances and irrevocable letter of credit are common for overseas trade Conditional sale means that the seller owns the goods until they are fully paid off by the buyer. Failure of payment allows seller to reposes goods. EX: car sales in instalments Credit analysis: How to find out of customers will pay 1. Customer history of payment with seller 2. New customers => look at financial statements of buying firm, seek views of a specialist in credit assessment (example risk rating agencies), ask buyers bank for a credit check Credit decision This is for NON-REPEAT ORDERS Should offer credit if the expected gain from doing so is positive Where p= probability customer will pay, (1-p) is default, PV = present value of order For repeat orders – even if there is default on the first order you may still grant credit again on a second order to secure a repaying client Sometimes a client will pay, but will pay very late so it costs more to collect Cancelation policy Large firms have economies of scale Small firms may farm this debt collection job out to a factor – known as factoring o This costs the seller a fee. The factor collects the debt and assumes risk of default customers. Factor has better knowledge and experience with setting credit limits. Common in Europe, not common in America Can obtain credit insurance in case of defaults Cash The marginal value of liquidity declines as you hold increasing amounts of cash Trade off: cost of keeping cash in inventory (the lost interest) against benefits (saving on transaction costs) Sweep programs: bank automatically “sweeps” surplus funds into an interest-bearing investment 3 main ways firms send and receive money electronically: direct payments, direct deposits, and wire transfers. Travels through the Automated clearing house (ACH) To speed up the deposit of cheques, some firms have a concentration account. Held at one of the companies local banks. This reduces transfer times as it is local and time taken to clear cheque is reduced since customers check is likely to be drawn at the local bank o Local lock box system for customer to drop off cheques is also used Much of the work of cash management is done by banks which costs the firm a fee Marketable securities Made in the money market. Large corps will manage their own but smaller corps will hire a professional investment management firm to do put their cash into this fund – mutual fund in low-risk, short term securities Money market investments don’t pay interest, only the difference at maturity. Interest rates are quoted on discount basis. Example discount 98.75 means for every $98.75 invested you receive $100 at maturity. A 5% discount is NOT a 5% return. Corporate bonds and government bonds => long-term debt securities Eurodollar = money deposited at a bank in Europe Domestic and foreign money markets LIBOR = London interbank offered rate IBF = international banking facilities Principle money market instruments: o U.S treasury bills Sales are by uniform price auction – all same price. Primary and secondary markets. o Federal agency securities Slightly higher return than treasury bills. Issues by government agencies as GSE’s o Short-term tax-exempts Interest is not subject to federal tax. Issued by states, municipalities, universities, agencies. Low risk and backed by insurance policy. o Variable-rate demand notes Long term securities (bonds) and sell early. Interest payments are linked to the level of short-term interest rates. When interest rates are reset the investor has the option to sell, so worth can’t be less than face value o Bank time deposits and certificates of deposit (CD’s) o o o o Make deposit at a bank for fixed period for small return. Can sell CD before maturity, but to cancel early costs a fee. (Like GIC) Commercial paper and medium term notes Unsecured, short and medium term debt issued by company’s on a fairly regular basis Bankers acceptances (BA’s) A written demand for bank to pay a given sum in the future. Once the bank accepts it, it can be traded. Repurchase agreements “repos” Secured loans that are typically made to a government security dealer. The investor buys part of the dealers holding of treasury security and simultaneously arranges to sell them back again at a later date at a specified higher price. Commonly overnight agreements. Floating-rate preferred stock Investing cash in another corps preferred stock. Can change with interest rates so can invest in preferred stock that is linked to the general level of interest rate Sources of short-term borrowing Bank loans Commitment o Company establishes a line of credit LOC that allows them to borrow up to an established limit from the bank o Evergreen credit = no maturity o Revolving credit = fixed maturity o Expensive - have to pay interest on borrowings and commitment fee (around 0.25%) Maturity o Short term loans Self-liquidating means the sale of goods provides the cash to repay the loan Bridge loan: interim financing until the purchase is completed and long term financing is arranged o Long term loans Typically 4-5 years Usually paid in level amounts over the maturity Rate of interest o Short term loans are fixed and quoted at discount o Longer-term loans interest is usually linked to the general level of interest rates. Example: LIBOR, federal funds rate or banks’ prime rate Syndicated loans o For large loans and credit lines o Borrower may pay an arrangement fee to one or more lead banks, which then parcels out the loan or credit line among a syndicate of banks Loan sales and collateralized debt obligations o Banks can sell a portion of their existing loans to other banks if they have excess demand Security o If bank is concerned about a firms credit risk, it will ask the firm to provide some security. This is collateral and consists of liquid assets. Bank may take a floating charge which gives a general claim if the firm defaults. Commercial paper o Short-term unsecured notes. Sold directly to investors from firms – no intermediary. Not under-written. o Asset backed commercial paper: company sells its assets to a special-purpose vehicle that then issues the paper Medium-term notes o Hybrid between corporate bonds and commercial paper o Maturity is never less than 270 days o Not underwritten but are sold on a regular basis Week 4 Lecture Notes: Time Value of Money Most important term and concepts: Opportunity costs of capital Theoretical fundamentals of time preferences of an individual investor: o Marginal rate of time preference o Marginal return of private investments Time value of money Transferring future values to present and present values to future PV of an individual future flow PV of a stream of future flows Under constant or fluctuating opportunity costs of capital over period And vice versa FV of flow or stream of future flows PV: the minimum amount of money I will rationally sell my assets ? *definition is very important. Look it up more! Shortcuts under specific conditions PV of perpetuity PV of annuity PV of growing annuity PV of growing perpetuity And vice versa for FV Specifics: Comparisons of differently submitted rates – so called efficient annual interest rate Continuous compounding Week 5: Textbook Notes Chapter 2: How to Calculate Present Values Perpetuity: Investment that delivers steady stream of cash flow forever Annuity: Investment that delivers steady stream of cash flow for a limited period “a dollar today is worth more than a dollar tomorrow” – time value of money “a safe dollar is worth more than a risky dollar” Future Value of N = N * (1 + r)^t Where r = annual interest rate t= years Present value: OR: DFt * Ct Where: C = cash flow you will receive at t If you multiply C by 1 / (1+r)^t instead of dividing, it is called the discount factor Discount factor = present value of one dollar received in year t PV of an investment opportunity r = discount rate/opportunity cost of capital in the PV formula cost of capital = the return forgone by not investing in the alternative (financial markets) PV is also the market price as it satisfies both buyer and seller NPV (net present value) = PV – required investment Co = cash flow today, usually a negative number because it is a cash outflow Return = profit (revenue – cost) / investment NPV rule: Accept investments that have positive NPV’s Rate of return rule: Accept investments that offer rates of return in excess of their opportunity costs of capital PV’s when there are multiple cash flows ROR on perpetuity => r = C/PV Can switch around => PV = C/r Where C is cash payment and r is discount rate This PV formula of perpetuity tells us the value of a regular stream of payments starting one period from now Discount factor = 1/r o Compared to PV discount factor of 1/(1+r) To find todays PV of a delayed perpetuity, you take the regular perpetuity payment and multiply it by the discount factor with t = when the delayed perpetuity starts because that is how many years we need to go back to find todays value Where PV = C * 1/r * 1/(1+r)^t How to value annuities Annuity: an asset that pays a fixed sum each year for a specified number of years Ex: equal-payment house mortgage or instalment credit agreement An annuity is equivalent to the difference between an immediate and a delayed perpetuity Annuity due: a level streamPV( of payments starting immediately (instead of in one year). It is worth (1+r) times the value of the ordinary annuity EX: 156M ordinary annuity * (1+r) = annuity due Amortizing loan: part of the regular payment is used to pay interest on the loan and part is used to reduce the amount of the loan Ex: Mortgage payments – where you pay principle and interest FV of an annuity Growing perpetuities If we assume r is greater than g then: PV of growing perpetuity = C / (r-g) PV of Growing annuities How interest is paid and quoted: The effective annual interest rate is the compounded rate Ex: 10% compounded semi-annually: the effective rate is 10.25% => 1/(1+0.05)^2 o Need to divide interest by 2 for semi-annual and multiply t by 2 since there are now 2 compounding periods Quoted annual rate (APR) vs. effective annual rate o Ex: monthly o APR = 12%/12 months = 1% a month so should be 12% a year Total payment divided by the number of payments o EAR = ((1+0.01)^12) -1 = 12.68% per year o When interest is paid once a year, APR and EAR are the same o When interest is paid more than once a year, EAR is greater than APR Value of investment = [1 + (r/m)]^m EAR =( [1 + (r/m)]^m ) -1 Where m is the compounding frequency EXCEL SPREADSHEET FUNCTIONS In FV formula, PV should always be negative