Chapter 1 - Cost Volume Profit Analysis Reviewer

advertisement

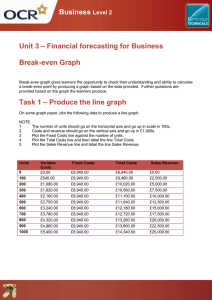

COST-VOLUME-PROFIT ANALYSIS Powerful tool for planning and decision making. Can be valuable tool in identifying the extent and magnitude of the economic trouble a company is facing and helping pinpoint the necessary solution. Allows manager to conduct sensitivity analysis by examining the impact of various price or cost levels on profit. THE BREAK-EVEN POINT AND TARGET PROFIT IN UNITS AND SALES REVENUE Approaches in finding break-even point: Operating Income Approach Contribution Margin Approach BASIC CONCEPTS FOR CVP ANALYSIS Operating Income It is income before income taxes. Only includes revenues and expenses. Net Income It is income minus income taxes. Contribution-margin-based income statement It is the useful tool for organizing firm’s costs into fixed and variable categories. 1. Formulas; a. Variable product cost per unit = Direct materials + Direct labor + Variable overhead b. Selling expense per unit = Price x percentage given c. Total Variable cost per unit = Direct materials + Direct labor + Variable overhead + Variable selling expense d. Contribution margin per unit = Price – Variable cost per unit e. Contribution margin ratio = (Price – Variable cost per unit)/ Price = (Sales – Total variable cost)/Sales f. Total fixed expense for the year Since variable product cost per unit consists of variable production or manufacturing costs, the plant manager would use this data. The plant manager is responsible for making a quality product as inexpensively and efficiently as possible. Knowing that variable product cost is $220 per unit provides a starting place for seeing what process improvements might do to the unit cost. The sales manager would be interested in the total variable cost per unit. Since this cost includes the sales commission, it reflects all of the variable costs. Sales managers can see the impact of the commissions (for which they are responsible) and can also see what impact a one-time discount might have on overall profitability. Top management would use the unit contribution margin for budgeting to see what impact an increase or a decrease in unit sales would have on operating income. Since fixed costs stay the same when units change, the contribution margin gives important information. 2. Company Name Contribution-Margin-Based Operating Income Statement Total Sales (Price x Units) Total variable expenses (VC per unit x units) Total contribution margin Total fixed expense Operating Income Per Unit THE EQUATION METHOD FOR BREAK-EVEN AND TARGET INCOME 1. Operating Income = Sales Revenue – Variable expenses – Fixed expenses Sales Revenue = (Price x Numbers of units) Variable Expenses = Variable cost per unit x Number of units 2. Units for a target profit = (Total fixed cost + Target income)/(Price – Variable cost per unit) Break-even units = Total fixed cost/ (Price – Variable cost per unit) At the break-even point, total revenue equals total cost. Once the break-even point is reached, all fixed costs are covered and additional units add only variable costs. Thus, contribution margin earned above break-even will go toward profit. The target operating income is treated as fixed cost for the purpose of figuring the number of units that must be produced and sold. Knowing the break-even units gives managers an easy way to tell just when during the year the firm moves out of the red and into the black. CONTRIBUTIN MARGIN APPROACH Refinement of the equation approach. It recognizes that at break-even, the total contribution margin equals the fixed expenses. Companies frequently prefer to express the break-even point in sales revenue. To do that, we recognize that total sales revenue must cover both total fixed costs and desired operating income. That is, the proportion of revenue left after variable costs are covered is what is left to cover fixed costs and income. BREAK-EVEN AND TARGET INCOME IN SALES REVENUE Variable costs Defined as a percentage of sales. Variable costs ratio Proportion of each sales that must be cover variable costs, can be computed using total data or unit data. Contribution margin ratio The percentage of sales revenue remaining after variable costs, is the proportion of sales to cover fixed costs and provide for profit. Sales Revenue Approach Operating Income = Sales – Variable costs – Total fixed costs Operating Income = Sales – (Variable costs x Sales) – Total fixed costs Operating Income = Sales (1 - Variable costs) – Total fixed costs Operating Income = (Sales x Contribution margin ratio) – Total fixed costs Sales = (Total fixed costs + Operating income)/Contribution margin ratio Break-even sales = Total fixed costs/Contribution margin ratio Break-even point in units = Total fixed costs/ (Price – Unit variable cost) Break-even units × Price = Price [Total fixed costs/ (Price - Unit variable cost)] Break-even sales = Total fixed costs × [Price/ (Price -Unit variable cost)] Break-even sales = Total fixed costs x [Price=Contribution margin Break-even sales = Total fixed costs/Contribution margin ratio TARGETED INCOME AS A PERCENT OF SALES REVENUE COMPARISON OF THE TWO APPROACHES Single-product setting Multiple-product setting AFTER-TAX PROFIT TARGETS Percentage of income Before-tax income = After-tax income/ (1 – Tax rate) Top management may be interested in target net income, since income taxes are a legitimate expense of the business and owners are interested in after-tax income. The accountant must first convert net income into operating income since the tax rate is a variable that is not taken into account in the break-even equation. Once the conversion is made, the break-even equation can be applied. MULTIPLE-PRODUCT ANALYSIS Direct fixed expenses Fixed costs that can be traced to each segment and would be avoided if the segment did not exist. Common fixed expenses Fixed costs that are not traceable to the segments and that would remain even if one of the segments was eliminated. BREAK-EVEN POINT IN UNITS FOR THE MULTIPLE-PRODUCT SETTING The break-even point in units gives managers a starting point for increasing profitability. If the company is making a loss, the breakeven point tells management just what needs to be done to stop losing money. Once the break-even point is passed, the company will earn a profit. By looking at break-even points for each product, managers can see whether one product is being “carried” by other products SALES MIX The relative combination of products being sold by a firm. Can be measured in units sold or in proportion of revenue. Is reduced to the smallest possible whole number. Represented by the percent of total revenue contributed by each product. Pricing decisions May involve new sales mix and must reflect this possibility. SALES MIX AND CVP ANALYSIS Defining a particular sales mix allows us to convert a multiple-product problem to single-product CVP format. Product Price Unit Unit Sales Unit Variable Contribut Mix Contributio Cost ion n Margin x Margin Sales Mix Product 1 Product 2 Package Contribution Margin GRAPHICAL REPRESENTATION OF CVP RELATIONSHIP It can help managers see the difference between variable cost and revenue and deepens their understanding of CVP relationships. Helps manager understand quickly what impact an increase or decrease in sales will have on the break-even point. Basic graphs: Profit-volume graph and Cost-volume-profit graph PROFIT-VOLUME GRAPH Portrays the relationship between profits and sales volume. Graph of operating income. Dependent variable It is operating income, along vertical axis. Independent variable It is number of units, along horizontal axis. COST-VOLUME-PROFIT GRAPH Depicts the relationships among cost, volume, and profits. Provides revenue and cost information. Graph two separate lines: the total revenue line and the total cost line: Revenue = Price × Units Total cost = (Unit variable cost × Units) + Fixed cost ASSUMPTIONS OF COST-VOLUME-PROFIT ANALYSIS The profit-volume and cost-volume-profit graphs just illustrated rely on some important assumptions. Some of these assumptions are as follows: 1. The analysis assumes a linear revenue function and a linear cost function. 2. The analysis assumes that price, total fixed costs, and unit variable costs can be accurately identified and remain constant over the relevant range. 3. The analysis assumes that what is produced is sold. 4. For multiple-product analysis, the sales mix is assumed to be known. 5. The selling prices and costs are assumed to be known with certainty. RELEVANT RANGE Operating range, second assumption. Once a relevant range has been identified, then the cost and price relationships are assumed to be known and constant. PRODUCTION EQUAL TO SALES The third assumption is that what is produced is sold. There is no change in inventory over the period. The fact that inventory has no impact on break-even analysis makes sense. Break-even analysis is a short-run decision-making technique, so we are looking to cover all costs of a particular period of time. Inventory embodies costs of a previous period and is not considered. CONSTANT SALES MIX Fourth assumption. Using spreadsheet analysis, the sensitivity of variables to a variety of sales mixes can be readily assessed. PRICES AND COST KNOWN WITH CERTAINTY Fifth assumption. Prices and costs are known. CHANGES IN THE CVP VARIABLES Alternative 1: If advertising expenditures increase, sales will increase from units to units. Alternative 2: A price decrease would increase sales. Alternative 3: Decreasing prices and increasing advertising expenditures will increase sales. INTRODUCING RISK AND UNCERTAINTY An important assumption of CVP analysis is that prices and costs are known with certainty. Risk and uncertainty Part of business decision making and must be considered. Risk differs from uncertainty in that with risk, the probability distributions of the variables are known. With uncertainty, the probability distributions are not known. Managers Deal with risk and uncertainty in a variety of ways. First, of course, management must realize the uncertain nature of future prices, costs, and quantity managers move from consideration of a break-even point to what might be called a break-even band. Two concepts useful to management (measures of risk) are margin of safety and operating leverage Margin of Safety The margin of safety is the units sold. Expected to be sold. The revenue earned. Expected to be earned above the break-even volume. It is a crude measure of risk. The further above the break-even point, the larger the margin of safety and the further the company is away from break-even and a loss. Margin of safety is a crude measure of risk. The further above the break-even point, the larger the margin of safety and the further the company is away from break-even and a loss. OPERATING LEVERAGE It is concerned with the relative mixed of fix costs and variable costs in an organization. As variable costs decrease, the unit contribution margin increases, making the contribution of each unit sold that much greater. Fixed costs are being used as leverage to increase profits. Uses of fixed costs to extract higher percentage changes in profits as sales activity changes. Degree of operating leverage Can be measured for a given level of sales by taking the ratio of total contribution margin to profit. Degree of operating leverage = Total contribution margin/Profit The automated system has higher fixed costs, lower variable costs, and a higher contribution margin per unit. The higher fixed costs are used to extract more contribution margin from each unit sold, and this system will pay off nicely—if unit sales are high enough. The manual system will be less risky if unit sales are lower. The degree of operating leverage can help a firm determine how much riskier the automated system is. SENSITIVITY ANALYSIS AND CVP A what-if technique that examines the impact of changes in underlying assumptions on an answer. CVP ANALYSIS AND NON-UNIT COST DRIVERS Conventional CVP analysis assumes that all costs of the firm can be divided into two categories: those that vary with sales volume (variable costs) and those that do not (fixed costs). Activity-based costing (ABC) system, in which costs are divided into unit- and non-unit-based categories. In conventional CVP, those non-unit variable costs are assumed to be fixed. CVP can be modified to take account of this richer set of variable costs. This type of modification can make CVP even more useful, since it provides more accurate insights concerning cost behaviour. Company’s costs can be explained by three variables: a unit-level cost driver, units sold; a batch-level cost driver, number of setups; and a product level cost driver, engineering hours. The cost equation can then be expressed as follows: Total cost = Fixed costs + (Unit variable cost × Number of units) + (Setup cost × Number of setups) + (Engineering cost × Number of engineering hours) Operating income, as before, is total revenue minus total cost. This is expressed as follows: Operating income = Total revenue - [Fixed costs + (Unit variable cost × Number of units) + (Setup cost × Number of setups) + (Engineering cost × Number of engineering hours)] A comparison of the ABC break-even point with the conventional break-even point reveals two significant differences. 1. The fixed costs differ. Some costs previously identified as being fixed may actually vary with non-unit cost drivers, in this case setups and engineering hours. 2. The numerator of the ABC break-even equation has two non-unitvariable cost terms: one for batch-related activities and one for product-sustaining activities. STRATEGIC IMPLICATIONS: CONVENTIONAL CVP ANALYSIS VERSUS ABC ANALYSIS CVP ANALYSIS AND JIT If a firm has adopted JIT, the variable cost per unit sold is reduced, and fixed costs are increased. The emphasis on total quality and long-term purchasing makes the assumption even truer that direct materials cost is strictly proportional to units produced. CVP ANALYSIS, ENTITIES MULTIPLE DRIVER, AND NONPROFIT SUMMARY OF LEARNING OBJECTIVES 1. Determine the number of units and amount of sales revenue needed to break even and to earn a target profit. i. At break-even, total costs (variable and fixed) equal total sales revenue. ii. Break-even units equal total fixed costs divided by the contribution margin (price minus variable cost per unit). iii. Break-even revenue equals total fixed costs divided by the contribution margin ratio. iv. To earn a target (desired) profit, total costs (variable and fixed) plus the amount of target profit must equal total sales revenue. v. Units to earn target profit equal total fixed costs plus target profit divided by the contribution margin. vi. Sales revenue to earn target profit equals total fixed costs plus target profit divided by the contribution margin ratio. 2. Determine the number of units and sales revenue needed to earn an after-tax target profit. i. Desired after-tax profit must be converted into before-tax profit to calculate units or revenue needed. ii. To find the operating income implied by a certain after-tax profit, divide the after-tax profit by 1 minus the tax rate. iii. Apply the break-even equations as before to the newly calculated before-tax profit target. 3. Apply cost-volume-profit analysis in a multiple-product setting. i. Multiple-product analysis requires the expected sales mix. ii. Break-even units for each product will change as the sales mix changes. iii. Increased sales of high contribution margin products decrease the break-even point. iv. Increased sales of low contribution margin products increase the break-even point. 4. Prepare a profit-volume graph and a cost-volume-profit graph, and explain the meaning of each. i. CVP assumes linear revenue and cost functions, no finished goods ending inventories, constant sales mix, and that selling prices and fixed and variable costs are known with certainty. ii. Profit-volume graphs plot the relationship between profit (operating income) and units sold. Break-even units are shown where the profit line crosses the horizontal axis. iii. CVP graphs plot a line for total costs and a line for total sales revenue. The intersection of these two lines is the break-even point in units. 5. Explain the impact of risk, uncertainty, and changing variables on cost-volume-profit analysis. i. Uncertainty regarding costs, prices, and sales mix affect the breakeven point. ii. Sensitivity analysis allows managers to vary costs, prices, and sales mix to show various possible break-even points. iii. Margin of safety shows how far the company’s actual sales and/or units are above or below the break-even point. iv. Operating leverage is the use of fixed costs to increase the percentage changes in profits as sales activity changes. 6. Discuss the impact of non-unit cost drivers on cost-volume-profit analysis. i. Under ABC, cost drivers are separated into unit-based and non-unitbased drivers. ii. Variable rates for the non-unit-based drivers are multiplied by the estimated level of the drivers and added to total fixed costs. iii. The standard CVP models still hold under ABC. SUMMARY OF IMPORTANT EQUATIONS The subject of cost-volume-profit analysis naturally lends itself to the use of numerous equations. 1. Sales revenue = Price × Units sold 2. Operating income = (Price × Units) - (Unit variable cost × Units) Fixed cost 3. Break-even point in units = Fixed cost/(Price - Unit variable cost) 4. Contribution margin ratio = Contribution margin/Sales = (Price - Unit variable cost)/Price 5. Variable cost ratio = Total variable cost/Sales = Unit variable cost/Price 6. Break-even point in sales revenue = Fixed cost/Contribution margin ratio = Fixed cost/ (1 - Variable cost ratio) 7. Margin of safety = Sales - Break-even sales = Units sold - Break-even units 8. Degree of operating leverage = Total contribution margin/Operating income 9. Percentage change in operating income = Degree of operating leverage × Percent change in sales