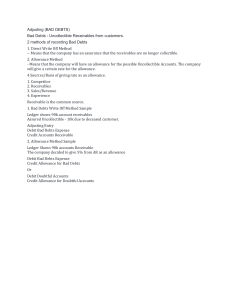

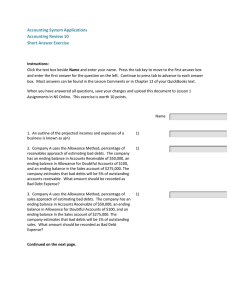

📒 Aging of Receivables Dates @February 23, 2021 Done Notes Topic Type 📒 Lesson Transactions that affect Allowance for Bad Debts Allowance for Bad Debts Contra-Asset account (i.e. deducted from Accounts Receivable) ⇑ = CREDIT (normal balance) if ever there will be a transaction that will increase allowance for bad debts, in preparing the journal entry, we have to credit allowance for bad debts because that is its normal balance ⇓ = DEBIT If there is a transaction that will decrease allowance for bad debts, opposite ng normal balance Transactions that Decrease Allowance for Bad Debts Accounts Written Off Kung may accounts na kailangan i-write-off, the journal entry using allowance method is: Since nag-debit ng allowance for bad debts, ibig sabihin babawasan siya Transactions that Increase Allowance for Bad Debts Recovery of Accounts Previously Written Off Recovery is equivalent to reversal of acconts written off, kaya ang entry ay: Aging of Receivables 1 In short, binaliktad lang yung entry na ginawa natin previously nung nag-write-off tayo ng accounts Another concept of recovery is it is equivalent to collection from customer. Second entry ay: Pero ang focus natin ay yung journal entry one, dahil dun may credit ng allowance for bad debts, na nakakapag-increase ng allowance for bad debts. Year-End Adjustment Methods of Recording Bad Debts Direct Write-Off Method Since direct, diretso / direct na dapat i-credit yung accounts receivable Ito ay may entry lamang under direct write-off method kapag worthless yung account. Kapag doubtful ang collections, walang entry, ang kadalasang ginagamit ay yung allowance method. Aging of Receivables 2 Allowance Method Allowance method - automatic na gagamit ka ng allowance account Ang pinagkaiba ng direct write-off mthod at allowance method is yung account na crinedit; sa direct write-off, credit accounts receivable, sa allowance method, credit allowance for bad debts Kahit magkaiba yung crinedit, dapat maisip natin na pareho lang effect niyan sa current assets (mababawasan yung current assets) Summarize yung transactions that could affect allowance for bad debts Beginning balance - credit kasi yun yung normal balance ng allowance for bad debts Recovery of accounts previously written off - can increase; Accounts written off - can decrease Aging of Receivables 3 After ma-effect yung Write-off and Recovery, ang macocompute ay tatawagin na balance before adjustment kasi at year-end, gagawa tayo ng adjusting entry to record Bad Debts and finally macocompute na yung Allowane for Bad Debts at the end of the period. There are problems wherein given na yung information to compute the ending balance of Allowance for Bad Debts without using the T-Account, ito yung tinatawag na Aging of Receivables, kung saan yung percentage of uncollectibility ay minumultiply sa Receivables. Ending Balance → % x Receivables / Aging of Receivables Meron ding problem kung saan pwede mo na macompute yung Bad Debts Expense, this time yung percentage of uncollectibility ay binabase sa Sales. Bad Debts Expense → % x Sales Methods of Estimating Bad Debts Naka-red yung "estimating" kasi yung kanina is "Methods of Recording" 1. Income Statement Approach % of uncollectibility x Sales = Bad Debts Expense 2. Balance Sheet Approach % of uncollectibility x Receviables = Allowance for Bad Debts Kapag ang percentage ay binase sa sales, which is an income statement element, dapat ang magiging product niyan ay income state element din in the form of an expense. Kapag ang percentage of uncollectibility ay binase sa receivables, which is a balance sheet item, dapat ang product niyan ay balance sheet item in the form of an allowance. Aging of Receivables When you prepare Aging of Receivables, you need to determine the Accounts Receivable at the end of the period. The amount of Accounts Receivable at the end of the period kailangan maclassify into "not yet due" or "Current Account" and "Past Due account". Table for Aging of Receivables Once na-multiply yung amount of receivables sa percentage na estimated to be uncollectible, ang lalabas ay yung allowance or provision. Amount x Estimated % Uncollectible = Allowance / Provision Aging of Receivables 4 Past due - depende sa entity kung ano ang number of days na pwede niya i-classify yung past due Instead na "Over 90 days", pwede ding 91-120 days tapos "Over 120 days", pero sa example natapos na siya sa "Over 90 days" Yung total sa "Amount" na column ay Accounts Receivable, End, at yung total sa "Allowance / Provision" na column ay Allowance for Bad Debts, End Note sa pag-compute ng Amortized Cost of Accounts Receivable Yung Amortized Cost na 'yan ang madalas na makikita sa problem, pero pwede rin ang maging equivalent niyan ay Carrying Value or Accounts Receivable to be Presented in the Statement of Financial Position Yung Allowane for Bad Debts, Allowance for Sales Returns, Allowance for Sales Discounts ay pwede ring tawaging Provision for Bad Debts, Provision for Sales Returns and Provision for Sales Discounts. 10:15 Aging of Receivables 5