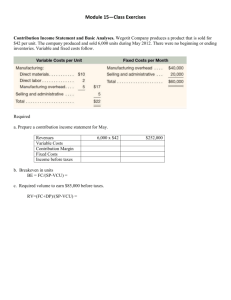

Ateneo de Zamboanga University School of Management and Accountancy Accountancy Department LEARNING PACKET COSMAN2 – Strategic Cost Management Session 1, First Semester, SY 2020-21 LEARNING PACKET NO. 3 TOPIC: Break-Even Point and Cost – Volume – Profit Analysis DATE: ____________________ Week No.: 3 Session: 1 INTENDED LEARNING OUTCOME: At the end of this learning units, the learners shall: 1.) Compute for Break-Even Point in a Single-Product and Multi-Product assumptions 2.) Compute for Target Profit Analysis using different assumptions (pre-tax, after-tax, percentage of sales ) 3.) Describe Margin of Safety and Degree of Operating Leverage I. CONCEPT NOTES 3.1.1 Nature of CVP Analysis Definition of CVP Analysis Cost-Volume-Profit (CVP) Analysis – a systematic examination of the relationships among costs, cost driver/activity level /volume, and profit. It is a powerful tool used by the management in order to help them understand the interrelationship among cost, volume and profit in an organization by focusing on interactions between five CVP elements. The Elements of CVP Analysis 1. 2. 3. 4. 5. Sales price of a product Volume or level of activity (within a relevant range) Variable cost per unit Total fixed cost Sales mix Application of CVP Analysis CVP Analysis may be applied to the planning and decision-making function of the management, which may involve choosing the 1. 2. 3. 4. type of product to produce and sell; pricing policy to follow; marketing strategy to use; and type of productive facilities to acquire. Simplifying Assumptions of CVP Analysis 1. All costs are classifiable as either variable or fixed (components of mixed costs are already segregated). 2. Cost and revenue relationships are predictable and linear over a relevant range of activity and a specified period of time. 3. Variable costs per unit and total fixed costs remain constant over the relevant range. 4. Unit sales price and market conditions remain unchanged. 5. Changes in costs and revenue are brought about by changes in volume alone. 6. There is no significant change in the level of inventory (Production = Sales). 7. Sales mix remains constant (for a company that sells multiple products). 8. Technology, as well as productive efficiency, is constant. 9. Time value of money concept is ignored. 3.1.2 Break-Even Analysis and Target Profit Analysis in a Single-Product Company Definition of Break-Even Point Break-Even Point – the sales volume (in pesos or in units) where total revenues equal total costs (TR = TC). Thus, at this point, the entity experiences neither profit nor loss (TR – TC = 0). Methods of Computing Break-Even Point Break-even sales can be computed using any of the following methods: 1. Graphic Approach 2. Equation Method or Algebraic Approach 3. Formula or Contribution Margin Approach Graphic Approach CVP Graph – also called break-even chart, it depicts the relationship of cost, volume, and profit in a graphical form. In this graph, the point where the total cost line intersects with the total revenue/sales line represents the break-even point. Steps in preparing the break-even chart: 1. Draw a line parallel to the volume axis to represent total fixed expense. 2. Choose some volume of unit sales and plot the point representing total expense (fixed and variable) at the sales volume you have selected. After the point has been plotted, draw a line through it back to the point where the fixed expense line intersects the pesos axis. 3. Again choose some sales volume and plot the point representing total sales in pesos at the activity level you have selected. Draw a line through this point back to the origin. Pesos Contribution Margin Method or Formula Approach This method uses directly the formula in finding Break-even point (in units or in pesos). Break-Even Point in Pesos (BEPP) BEPP = Total Fixed Cost (TFxC) Contribution Margin Ratio (CMR) When the BEP in units is already known, the BEPP can be computed as BEPP = Break Even Point in Units X Sales Price per Unit (SP/u) Break-Even Point in Units (BEPu) BEPu = Total Fixed Cost (TFxC) Contribution Margin per Unit (CM/u) Target Profit Analysis At certain instances, entities need to determine the volume of sales (in pesos or in units) that they need in order to achieve a specified amount of desired/targeted profit. In determining the targeted sales for a desired profit, the formula in finding for the BEP will still be used, substituting the zero-value for profit with the amount of the desired profit. Thus, TSP In Pesos TFxC + Desired Profit (DP) = CMR where: TS = Targeted sales DP = Desired profit before tax After-tax Desired Profit TSu In Units TFxC + Desired Profit (DP) = CM/u When the amount of the desired is expressed in an after-tax amount, said amount would have to be grossedup/converted into its before-tax equivalent before added to the amount of the total fixed cost. To compute for the before-tax profit, the formula is: DP = After-Tax Profit 1 - Tax Rate Desired Profit as a Percentage of Sales When the desired profit is expressed not as an amount, but as a percentage of sales, the formula to compute for the required sales can be derived based on the formula above Total Fixed Costs CM per unit - (Percentage x Selling price) 3.1.3 Break-Even Analysis and Target Profit Analysis in a Multiple Product Company Multi-Product BEP – the total volume of sales (in pesos or in units) that a company that produces and/or sells multiple products generates where the company experiences neither loss nor profit. Product BEP – the share of an individual product in the total BEP of a multiple product company based on the predetermined sales mix of the company’s products. Sales Mix – the relative proportion in which a company’s products are sold. Break-Even Analysis for a Multiple Product Company In a multiple product company, determining the break-even point may involve additional computations due to the following considerations: 1. Fixed costs incurred by a company cannot be usually identified with the specific products that the company produces and/or sell. 2. Each product may differ in terms of its contribution to the profit of the company due to the difference in selling price, variable costs, and sales volume of each product, thus differently contributes to the recovery of the total fixed costs incurred by the entity. In order to compute for the BEP for multiple product company, instead of using a single CMR or CM/u, it is required that the same shall be expressed in terms of their weighted average values (WaCMR and WaUCM) using the sales mix of each product as basis for weight assignment. BEPP = TFxC WaCMR BEPu = TFxC WaUCM Break Even point in Pesos = Total Fixed Costs Weighted Average Contribution Margin Ratio Break Even Point in Units = Total Fixed Costs Weighted Average Contribution Margin Per Unit The Weighted Average Contribution Margin ( WaCMR ) and Weighted Average Contribution Margin Per Unit (WAUCM) can be computed using the following formulae: WaCMR = Summation of ( Contribution Margin Ratio of a Product X Sales Mix Ratio in Pesos ) WAUCM = Summation of ( Contribution Margin / Unit of a Product X Sales Mix Ratio in Units) or WaCMR = Σ (CMRj X SMPj) or Total CM WaCMR = Total Sales WaUCM = Σ (CM/uj X SMuj) or Total CM WaUCM = Total Units Sales mix ratios (SM) in pesos and in units for each product may be computed as follows: Sales Mix Ratio in Pesos SMPj = Salesj Total Sales SMuj = Units Soldj Total Units Sold Sales Mix Ratio in Units SMuj = Units Soldj Total Units Sold The BEP shall then be distributed to the different products using the following formulae: Product Break Even Point in Pesos = Break Even Point in Pesos X Sales Mix Ratio in Pesos Product Break Even Point in Units = Break Even Point in Units X Sales Mix Ratio in Units Target Profit Analysis Target sales determination in a multiple product company is basically similar to that of a single product company. TSp ( Target sales in persos ) TSu ( Target sales in Units TSP = TFxC + DP WaCMR TSu = TFxC + DP WaUCM where: TS = Targeted sales DP = Desired profit before tax 3.1.4 Margin of Safety Margin of Safety – the excess of budgeted (or actual) sales over the creak-even volume. It is the amount or units of sales by which actual or budgeted sales may be dropped/decreased without resulting into a loss. Margin of Safety in Pesos = Sales in Pesos – Break Even Point in Pesos Margin of Safety in Units = Sales in Units – Break Even Point in Units Margin of Safety Ratio = Margin of Safety in Pesos / Sales in Pesos or Margin of Safety in Units / Sales in Units 3.1.5 Operating Leverage Operating Leverage – a measure of how sensitive net operating income is to a given percentage change in sales. It is also considered as the extent to which a company uses fixed costs in its cost structure. Degree of Operating Leverage (DOL) – also called as Operating Leverage Factor (OLF), this serves as multiplier in measuring the extent of the change in profit before tax resulting from the change in sales. CM PBT Where: PBT = Profit before tax DOL = CM = Contribution Margin To compute for the percentage change in profit: Percentage Change in Profit = Percentage Change in Sales X Degree of Operating Leverage Sample Problem : 1. Brihon Corporation produces and sells a single product. Data concerning that product appear below: Selling price per unit ....................... Variable expense per unit ............. Fixed expense per month .............. P230.00 P103.50 P518,650 Required: a. Assume the company's monthly target profit is P 12,650. Determine the unit sales to attain that target profit. b. Assume the company's monthly target profit is P 63,250. Determine the dollar sales to attain that target profit. Ans: Selling price per unit ................................................ Variable expense per unit ...................................... Contribution margin per unit and CM ratio .... Per Unit Percent of Sales P230.00 100% 103.50 45% P126.50 55% a. Unit sales to attain target profit = (Fixed expenses + Target profit)/Unit contribution margin = (P518,650 + P12,650)/P126.50 = 4,200 b. Total sales dollars to attain target profit = (Fixed expenses + Target profit)/CM ratio = (P518,650 + P63,250)/0.55 = P1,058,000 2. Ms. Ganda sells two beauty products for hopeless individuals, Sandpaper and Eraser. Historically, the firm has sold, on the average, 400 units of Sandpaper and 1,200 units of Eraser. It incurs fixed costs of P14,400 per period. Pertinent data about the two products are as follows: Sandpaper Eraser Selling price P20 P10 Contribution margin per unit 6 4 REQUIRED: 1. How much revenue is needed to break-even? How many units of Sandpaper and Eraser does it represent? Step 1 : Determine sales mix in pesos Sales Mix Ratio in Pesos Salesj SMPj = Total Sales Units Soldj SMuj = Total Units Sold P Sales Mix Ratio in Pesos for Sandpaper = P20 X 400 / ( P20 X400 + P10 X 1,200 ) = P 8,000 / P20,000 = 40% Sales Mix Ratio in Pesos for Eraser = P20 X 400 / ( P20 X400 + P10 X 1,200 ) = P 12,000 / P20,000 = 60% Step 2 : Determine Contribution Margin Percentage Contribution Margin Percentage = Contribution Margin / Selling Price For Sandpaper = P6 / P 20 = 30% For Eraser =P4 / P10 = 40% Step 3 : Determine Weighted Average Contribution Margin Ratio = Summation of ( Sales Mix Ratio X Contribution Margin Ratio ) = ( 0.4 X 0.3 ) + (0.6 X 0.4 ) = 0.12 + 0.24 = 0.36 Step 4: Determine Break Even Point in Pesos Break Even Point in Pesos = Fixed Costs / Weighted Average Contribution Margin Ratio = P 14,400 / 0.36 = P 40,000 Step 5: Determine the Number of Units for Each Product Break Even Point Revenue * Sales Mix Ratio in Pesos Selling Price per Unit Number of Units – Sandpaper P40,000 * 40% (Percentage of Sales ) = 800 units P20 ( Selling Price per Unit ) Number of Units –Eraser P40,000 * 60% (Percentage of Sales ) = 2,400 units P10 ( Selling Price per Unit ) 2. How much, revenue is needed to earn pre-tax profit of P10,800? Targeted Sales = Fixed Costs + Desired Profit / Weighted Average Contribution Margin Ratio = (P 14,400 + 10,800 ) / 0.36 = P 70,000 3. How much revenue is needed to earn an after-tax profit of P15,680? (Ms.Ganda pays corporate income taxes) Since the word is “ corporate income taxes” , we assume it to be 30% Step 1 : Find Profit Before Tax Profit Before Tax = After-Tax Profit / 1 – Tax Rate = 15,680 / ( 1-0.3 ) = 22,400 Targeted Sales = Fixed Costs + Desired Profit / Weighted Average Contribution Margin Ratio = (P 14,400 + 22,400 ) / 0.36 = P 102,222 (estimate ) 4. If the company earns the revenue determined in (2), but in doing so, sells 2 units of Sandpaper for each Eraser, what would the pre-tax profit or loss be? Step 1: Find Sales Mix Ratio in Pesos Let us assume 2 Units of Sandpaper X P 20 each = P40 1 Unit of Eraser X P 10 Each = 10 Total = 50 Sales Mix Ratio ( In Pesos ) Sales Mix Ratio in Pesos for Sandpaper = P40 / P50 = 80 % Sales Mix Ratio in Pesos for Eraser = P10/P50 = 20% Step 2 : Determine the total contribution margin per product Total Contribution Margin Per Product = Total Revenue X Sales Mix Ratio X Contribution Margin Ratio Sandpaper P 70,000 X 0.8 X 0.3 = P16,800 Eraser P 70,000 X 0.2 X 0.4 =P 5,600 Step 3: Deduct Fixed Costs to find the Pre-Tax Profit / Loss Total Contribution Margin = 22,400 Less: Fixed Cost 14,400 Pre-Tax Profit / Loss = 10,000 II. CHECKING FOR UNDERSTANDING ( Problems with solutions ) PROBLEM 1 Diamond Jim’s makes and sells class rings for local schools. Operating information is as follows: Selling price per ring Variable cost per ring Rings and stones Sales commissions Overhead Annual fixed cost Selling expenses Administrative expenses Manufacturing $600 $220 48 32 $180,000 105,000 60,000 a. What is Diamond Jim’s break-even point in rings? b. What is Diamond Jim’s break-even point in sales dollars? c. What would Diamond Jim’s break-even point be if sales commissions increased to $54? d. What would Diamond Jim’s break-even point be if selling expenses decreased by $6,000? PROBLEM 2 Mel’s Male Accessories sells wallets and money clips. Historically, the firm’s sales have averaged three wallets for every money clip. Each wallet has an $8 contribution margin, and each money clip has a $6 contribution margin. Mel’s incurs fixed cost in the amount of $180,000. The selling prices of wallets and money clips, respectively, are $30 and $15. The corporate-wide tax rate is 40 percent. a. How much revenue is needed to break even? How many wallets and money clips does this represent? b. How much revenue is needed to earn a pre-tax profit of $150,000? c. How much revenue is needed to earn an after-tax profit of $150,000? d. If Mel’s earns the revenue determined in (b) but does so by selling five wallets for every two money clips, what would be the pre-tax profit (or loss)? Why is this amount not $150,000? PROBLEM 3 Beantown Baseball Company makes baseballs that sell for $13.00 per two-pack. Current annual production and sales are 960,000 baseballs. Costs for each baseball are as follows: Direct material $2.00 Direct labor 1.25 Variable overhead 0.50 Variable selling expenses 0.25 Total variable cost $4.00 Total fixed overhead $1,250,000 a. Calculate the unit contribution margin in dollars and the contribution margin ratio for the company. b. Determine the break-even point in number of baseballs. c. Calculate the dollar break-even point using the contribution margin ratio. d. Determine the company’s margin of safety in number of baseballs, in sales dollars, and as a percentage. e. Compute the company’s degree of operating leverage. If sales increase by 30 percent, by what percentage would pre-tax income increase? f. How many baseballs must the company sell if it desires to earn $1,096,000 in pretax profit? g. If the company wants to earn $750,000 after tax and is subject to a 40 percent tax rate, how many baseballs must be sold? h. How many baseballs would the company need to sell to break even if its fixed cost increased by $50,000? (Use original data.) i. Beantown Baseball Company has received an offer to provide a one-time sale of 20,000 baseballs at $8.80 per two-pack to the Lowell Spinners. This sale would not affect other sales, nor would the cost of those sales change. However, the variable cost of the additional units would increase by $0.20 for shipping, and fixed cost would increase by $6,000. Based solely on financial information, should the company accept this offer? Show your calculations. PROBLEM 4 Dim Witt is the county commissioner of Clueless County. He decided to institute tolls for local ferry boat passengers. After the tolls had been in effect for four months, Astra Astute, county accountant, noticed that collecting $1,450 in tolls incurred a daily cost of $2,000. The toll is $0.50 per passenger. a. How many people are using the ferry boats each day? b. If the $2,000 cost is entirely fixed, how much must each passenger be charged for the toll process to break even? How much must each passenger be charged for the toll process to make a profit of $250 per day? c. Assume that only 80 percent of the $2,000 is fixed and the remainder varies by passenger. If the toll is raised to $0.60 per person, passenger volume is expected to fall by 10 percent. If the toll is raised and volume falls, will the county be better or worse off than it is currently and by what amount? d. Assume that only 80 percent of the $2,000 is fixed and the remainder varies by passenger. If passenger volume will decline by 5 percent for every $0.20 increase from the current $0.50 rate, at what level of use and toll amount would the county first make a profit? e. Discuss the saying “We may be showing a loss, but we can make it up in volume.” PROBLEM 5 Tennessee Tonic makes a high-energy protein drink. The selling price per gallon is $7.20, and variable cost of production is $4.32. Total fixed cost per year is $316,600. The company is currently selling 125,000 gallons per year. a. What is the margin of safety in gallons? b. What is the degree of operating leverage? c. If the company can increase sales in gallons by 30 percent, what percentage increase will it experience in income? Prove your answer using the income statement approach. d. If the company increases advertising by $41,200, sales in gallons will increase by 15 percent. What will be the new break-even point? The new degree of operating leverage? III. ANALYSIS 1.) Which is more strategic for a company, a higher or lower break-even point? 2.) Assuming that we have 2 products, Product A with a contribution margin ratio of 0.7 and Product B with a contribution margin ratio of 0.4. We can expect a lower break—even point if Product ____ has more sales in comparison to Product ______. 3.) How is fixed costs related to degree of operating leverage? V. INDEPENDENT LEARNING 1.) Aqua Gear, in business since 2008, makes swimwear for professional athletes. Analysis of the firm’s financial records for the current year reveals the following: Average swimsuit selling price Variable swimsuit expenses Direct material Direct labor Variable overhead Annual fixed cost Selling Administrative P70 28 12 8 P 10,000 24,000 The company’s tax rate is 40 percent. Mr. Dewgong , company president, has asked you to help his answer the following questions. a. What is the break-even point in number of swimsuits and in pesos ? b. How much revenue must be generated to produce P40,000 of pre-tax earnings? How many swimsuits would this level of revenue represent? c. How much revenue must be generated to produce P40,000 of after-tax earnings? How many swimsuits would this represent? d. What amount of revenue would be necessary to yield an after-tax profit equal to 20 percent of revenue? e. Aqua Gear is considering purchasing a faster sewing machine that will save P6 per swimsuit in cost but will raise annual fixed cost by P40,000. If the equipment is purchased, the company expects to make and sell an additional 5,000 swimsuits. Should the company make this investment? f. A marketing consultant told Aqua Gear managers that they could increase the number of swimsuits sold by 30 percent if the selling price was reduced by 10 percent and the company spent P10,000 on advertising. The company has been selling 3,000 swimsuits. Should the company make the changes advised by the consultant? 2.) Yard Bird manufactures commercial and residential riding lawnmowers. The company sells one commercial mower per three residential mowers sold. Selling prices for the commercial and residential mowers are, respectively, P5,600 and P1,800, and variable selling and production cost are, respectively, P3,800 and P1,000. The company’s annual fixed cost is P8,400,000. Compute the sales volume of each mower type needed to