We will not beat around the bush: We are very proud of our flagship Ariel Fund’s performance record. Within its Morningstar1 MidBlend Category, the Fund ranks in the top decile over the trailing 1-, 3-, 5-, and 15-year periods as of March 31, 2015. True, no

fund has a spotless record: Ariel Fund ranks in the 70th percentile over the 10-year period. That decade-long period contains the

2006-2008 period when the Fund struggled. But just as there are periods where a fund is out of favor, there are periods where

everything clicks. In the six years between the March 9, 2009 bottom and March 9, 2015, Ariel Fund ranks number one in the 259

funds in this same category. Moreover, its performance over that stretch has been balanced. Among funds that existed in March

2009 as well as March 2015, Ariel Fund ranked number one among 259 category peers in the three years from March 9, 2009 to

March 9, 2012, and it ranked number four among 322 in its category in the three years from March 9, 2012 to March 9, 2015.

True to our fiercely competitive form, we are not resting on our laurels but are investigating the period in order to keep the streak

alive. We want to deeply examine our activities in the periods from 2009 to 2012, and 2012 to 2015 to determine what lessons we

could draw that we can apply going forward.

To be sure, we knew the big things had not changed: In large part our people, process and especially our philosophy have

remained quite stable over the last decade. We remain value investors who strive to purchase shares in growing companies that

trade at a large discount to their intrinsic values. We intend to hold them while the gap between price and value closes, which

typically takes several years. With all that in mind, we decided to examine Ariel Fund’s holdings in March 2009, March 2012 and

March 2015 to search for patterns that drove performance over back-to-back three-year periods.

The focus and concentration of Ariel Fund shifted meaningfully but gradually over the period. As of March 31, 2009, we held 31

equity positions in the Fund, which is toward the low end of our historical range. As the bear market ravaged stock prices and sent

valuations to once-in-a-lifetime lows in early 2009, we concentrated on our best opportunities and shed other holdings. We also

devoted a high percentage of our assets into the top ten holdings: 42.6%. Then, as stocks appreciated substantially over the next

three years, we gradually built our roster of holdings, reaching 37 by March 2012. We also made the portfolio slightly more even

by weight: In March 2012 the top 10 stocks held 36.9% of assets. This flattening continued the next three years, as the roster of

stocks shrank slightly to 35, but with only 33.3% of assets in the top 10. Note that the shift was neither massive nor sudden; it was

a tilt, rather than a sharp turn.

Past performance does not guarantee future results. Any past extraordinary performance for the short-term periods may not be

sustainable and is not representative of the performance over longer periods. Morningstar, Inc. is a nationally recognized

organization that reports performance and calculates rankings for mutual funds. Rankings are based on total returns. Morningstar

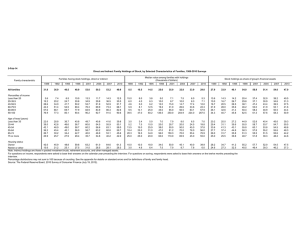

ranks each fund relative to all funds in the same category. For the period ended March 31, 2015, the rankings of Ariel Fund for the

1-, 3-, 5-, 10-, and 15-year periods were 4 out of 370 funds, 4 out of 319 funds, 25 out of 268 funds, 118 out of 168 funds, and 7

out of 96 funds, respectively, among Morningstar Mid-Cap Blend funds. For the period ended March 9, 2015, the rankings of Ariel

Fund for the 1-, 3-, 5- and 10-year periods were 8 out of 372 funds, 4 out of 322 funds, 30 out of 276 funds, and 118 out of 169

funds, respectively, among Morningstar Mid-Cap Blend funds. For the period ended March 9, 2012, the rankings of Ariel Fund for

the 1-, 3-, 5- and 10-year periods were 288 out of 288 funds, 1 out of 259 funds, 165 out of 208 funds, and 108 out of 130

funds, respectively, among Morningstar Mid-Cap Blend funds.

1

1

The roster of specific holdings in the Fund was neither wholly static nor largely erratic. Rather, a fluid shift occurred over the period.

Indeed, our overall portfolio turnover ratio was very similar to our long-term pattern: The annual median was 30% during the six

years, within our normal range. If you assume that, typically, about half of turnover is position adjustment and the other half is

swapping old holdings for fresh names, a 31-holding portfolio should retain roughly 13 of its original holdings at the end of six

years. Indeed, of the 31 holdings in Ariel Fund six years ago, 14 remain in the portfolio today. Also, the addition of new holdings

was balanced over the two three-year periods. Of the 21 new holdings today, 11 came between March 2009 and March 2012 and

10 more in the last three years. As you would expect, the holdings that departed did so for any number of reasons: Some were

acquired, some no longer fit our original thesis, some became expensive, and some eventually exceeded our market cap range.

Finally, the record shows a flexible handling of the stocks that remained in the fund for all six years. A few were top holdings in

2009, 2012, and 2015, suggesting their valuation was attractive and our confidence high throughout the period. For instance, real

estate firm JLL (JLL) ranked in the top 10 holdings in all three March portfolios, while competitor CBRE Group, Inc. (CBG) ranked in

the top 15 all three times. Other holdings, such as Meredith Corp. (MDP) and Sotheby’s (BID), were modestly sized positions as the

first quarters of 2009, 2012 and 2015 ended. There was not always continuity, however. Some of the stocks we thought were

screamingly cheap in 2009 remain in the portfolio and at considerably lower weights: Janus Capital Group Inc. (JNS) was a top five

holding in 2009 and 2012, but now ranks 25th in the portfolio. Royal Caribbean Cruises Ltd. (RCL) was originally a top five holding

as well but fell just outside the top 10 holdings in 2012 and 2015. On the flip side, some holdings from 2009 got cheaper in our

eyes, so we raised their weighting over the years: Brady Corp. (BRC) was in the middle of the portfolio in 2009 and 2012 but is

now a top 10 holding.

The record tells us we did not employ unusual tactics during the period of unusually good performance; rather, we simply executed

our strategy well. By focusing intently on intrinsic value, we were able to maintain nearly half the portfolio, gradually shed the other

half and replace stocks we sold with new positions. The rather mundane and yet encouraging lesson is that the sharp performance

edge over the last six years did not come from a change to the game plan, but rather to its precise execution during a time when

external changes were significant and frequent.

The opinions expressed are current as of the date of this commentary but are subject to change. The details offered in this

commentary do not provide information reasonably sufficient upon which to base an investment decision and should not be

considered a recommendation to purchase or sell any particular security.

Investing in equity stocks is risky and subject to the volatility of the markets. Investing in small-cap and mid-cap stocks is more risky

and more volatile than investing in large-cap stocks. The intrinsic value of the stocks in which the Fund invests may never be

recognized by the broader market. The Fund concentrates a significant portion of its assets in the financial services and consumer

discretionary sectors, and performance may suffer if these sectors underperform the overall stock market.

This commentary discusses stocks which may be, or may have been, held in certain portfolios Ariel manages. These stocks do not

represent all of the holdings in the Fund. Portfolio holdings are subject to change. The performance of any single portfolio holding is

no indication of the performance of other portfolio holdings of Ariel Fund. Click here for the current holdings for Ariel Fund.

Investors should consider carefully the investment objectives, risks, and charges and expenses before investing. For a current

prospectus or summary prospectus which contains this and other information about the funds offered by Ariel Investment Trust, call

us at 800-292-7435 or visit our website, arielinvestments.com. Please read the prospectus or summary prospectus carefully before

investing. Distributed by Ariel Distributors, LLC, a wholly-owned subsidiary of Ariel Investments, LLC.

2

0

0