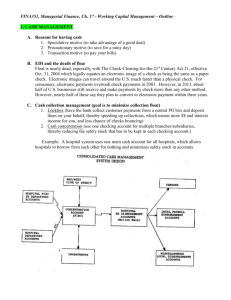

SMART MONEY CREDIT THE TRUE STORY 1

SMART MONEY

CREDIT

THE TRUE STORY

1

What is Credit?

• An arrangement to receive cash, goods, or services now, and pay for them in the future.

• A claim against Future

Income.

• A reduction in Disposable

Income during the time period the Credit is repaid.

2

Why do you need Credit?

• It enables people to enjoy goods and services now, and pay for them in the future.

• You may not have enough cash to pay for the good or service, and it may take a very long time to save the necessary funds.

• The proper use of Credit Cards allows consumers to postpone payment of goods, earning interest on the funds that would have been paid in cash.

3

Where do you obtain Credit?

• Commercial Banks

• Consumer Finance

Companies

• Credit Unions

• Life Insurance

Companies

• Federal Savings Banks

• Credit Card Companies

4

What determines if you will get the Credit desired?

1. CHARACTER – Will you repay the loan?

2. CAPACITY – Can you repay the loan?

3. CAPITAL – What are your

Assets and Net Worth?

4. COLLATERAL – What if you don’t repay the loan?

5. CONDITIONS – What if your job is insecure?

5

Other Creditworthiness

Factors

• AGE (ECOA)

• PUBLIC ASSISTANCE

• HOUSING LOANS

Care must be taken not to violate the conditions of the Equal

Credit Opportunity Act, or protected classes under the

Civil Rights Act of 1964, and its extensions.

6

Credit Reports

• Nowadays, due to the glut of consumers and the need to save time, grantors of credit have come to rely on Credit Reports.

• There are three (3) major Credit Reporting

Bureaus , and each publishes its own form of a

FICO Score.

• FICO is the acronym for Fair Isaac

Corporation, the developer of the algorithm and program used to calculate a FICO Score

(1956).

7

What’s in your Credit

Report?

• Personal Information

• Accounts

• Inquiries

• Negative Items

According to independent research

Credit Scoring is not unfair to minorities or those with little

Credit History.

8

FICO Scores

• It’s intention is to measure your Credit Risk, based on your current FICO Score.

• The Scores range between 300 and 850.

• FICO Scores are based on:

1. Payment History (35%)

2. Amounts Owed (30%)

3. Length of Credit History (15%)

4. New Credit (10%)

5. Type of Credit Used (10%)

9

FICO Scores

continued

• The Median FICO Score is 723.

• Higher Scores mean Lower Interest Rates.

• Most Lenders based Approval on FICO

Scores.

• Many Lenders use the FICO Score in conjunction with their own Application.

• Scores will vary between different Credit

Bureaus.

10

FICO Scores

continued

1. Equifax produces a BEACON Report.

2. Experian produces an Experian/Fair

Isaac Risk Model.

3. TransUnion produces a FICO Risk

Score, Classic.

Any and all Bureaus may be contacted by your

Lender.

11

Why is my FICO Score ‘X’?

• Depends on your Credit track record reflected in the FICO Score.

• Items will remain on your Credit

Report for between 7 and 10 years ; it’s up to you to check your

Report for Accuracy.

• Do not allow debts to be placed with

Collection Agencies.

• Do not permit balances on your

Credit Cards, pay them monthly.

12

FICO Payment History (35%)

• Almost 65% of all Credit

Reports show no late payments.

• This is the largest portion of your FICO Score.

• Take care of past debts and ensure they are corrected on your Credit Report.

13

FICO Amounts Owed (30%)

• What is the total amount owed?

• How many accounts have balances outstanding?

• How close to ‘limits’ are the revolving accounts?

• What is remaining on any installment loans?

• Is your debt over suggested ratios?

14

FICO Length of Credit

History (15%)

• How long have you been using

Credit?

• How long have specific accounts been established?

• How long has it been since you’ve used specific accounts?

• Do not open and close accounts too quickly.

Let them ‘season’ for a couple of years.

15

FICO New Credit (10%)

• Are you taking on too much debt

(ratios)?

• How many ‘new’ accounts do you have?

• How long has it been since you’ve opened a new account?

• What has been the length of time between and number of Credit

Inquiries?

• What is your most recent Credit

History?

16

FICO Types of Credit in Use

(10%)

• How well are you managing your current Credit?

• What kinds of Credit

Accounts do you have?

• Closed Accounts stay on your record, so don’t try to

‘escape’ an existing debt.

17

Facts

• A ‘good’ FICO Score is determined by the Lender.

Statistics are published by Fair

Isaac Corporation.

• If you’re turned down for Credit, you should receive a written statement stating the reason for rejection of your application.

• Manage your Credit so you pay the best available interest rates, terms, etc. when you need

Credit.

18

Now you know …

CREDIT

THE TRUE STORY

19