Chapter 10 notes

advertisement

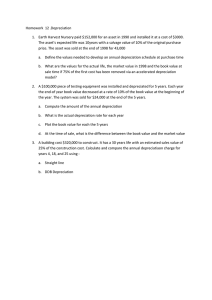

Chapter 10 notes The category Property, Plant, and Equipment (fixed assets) include all the assets that are depreciable plus land. Based of the Cost principle, we assign the acquisition costs to all these assets. Acquisition costs include any cost incurred in order to get the asset to be ready for its intended use. These costs include price paid, sales tax, license fee, professional costs, modifying costs, commission, delivery costs, installation, set up costs, and testing costs. Depreciation Depreciation can be explained in two ways: 1. Due to normal wear and tear (therefore reducing its book value) of the asset from daily use 2. It is a gradual way to recover initial investment There are three ways of depreciation introduced (page 432): 1. Straight line 2. Unit of activity 3. Declining balance There are three terms which are very important in depreciation: a. Acquisition costs b. Useful life ----- This is a very subject number. This is a period of time that you think you can use this asset in your business to generate revenue c. Salvage value ----- This is the estimated fair market value of the asset at the end of the useful life Under Straight line method, we use the following formula to calculate annual depreciation: Annual depreciation = (cost – salvage value ) / useful life (in years) Monthly depreciation will be ----- annual depreciation / 12 Under unit of activity method, we need to estimate the total units a machine can produce throughout its useful life or total number of miles a truck can run throughout its useful life. Then we get the cost per unit = (total cost – salvage) / total units Every subsequent period, the depreciation amount will be: Units produced in that period * cost per unit Under declining balance method (page 435), for annual depreciation, we use twice the straight line rate. e.g. If an asset has a life of 5 years, the straight-line rate will be 20% per year. Under the declining balance method, the rate will be 40%. Let say the cost is 10,000. First year depreciation will be 10,000 * 40% = 4000. Second year will be (10,000 – 4000) * 40% = 2400. In the third year, the depreciation will be (10,000 – 4000 – 2400) * 40%. Notice the salvage is never used yet. The final book value of the asset can never get below the salvage value (refer to P435). When we dispose of assets either during its life or at the end of its life, we will need to zero out its cost account, accumulated depreciation account (for that asset only), and recognize gain/loss from the transaction. Natural Resources Instead of calling it depreciation expense, we call this depletion expense. The procedure is very similar to units of activity method (refer to P442). Be aware of one thing, at the end of the year, we figure how many pounds of minerals have been extracted, we multiply the depletion cost per pounds with this total extracted poundage. The product will be debited to inventory. When the minerals are sold then we pass the inventory cost to depletion expense. Intangible Assets Intangible assets include patents, copyrights, trademarks and trade names, franchises and licenses, goodwill. We only amortize those with definite useful lives. Therefore, we do not amortize trademarks/names and goodwill. Patents ------- Accumulate costs primarily from buying a patent (new inventions) right from someone else Copyright -------- Accumulate costs primarily from buying a copyright (a book or a movie) from someone else Trademarks/names --------- Accumulate costs primarily from acquiring the trade mark or name from someone else Franchise --------- When you want to run a McDonald, you need to pay a large lump sum of money to McDonald corporation in order to sign a lease (let say 10 years) to operate a McDonald fast food. That money will be capitalized and amortized through the term of the lease. Licenses ---------- Every cell phone company has to lease certain signal frequency range from the government in order to provide cell phone services to customers. They need to pay an initial large lump sum payment to the government or to another cell phone company. That money will be capitalized and amortized through the lease term. Good will ------- This is created only when a company acquires another company and the price paid exceeds the net worth of the company being bought. Reasons for overpayment include exceptional management team, company reputation, good relation with labor union.