11 Depreciation, Impairments, and Depletion DEPRECIATION

advertisement

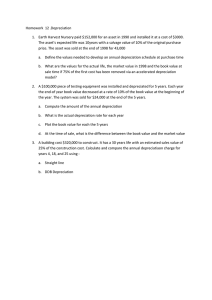

CHAPTER 11 Depreciation, Impairments, and Depletion ……..…………………………………………………………... DEPRECIATION “allocating the cost of tangible assets to those periods expected to benefit” Depreciable base = Original cost - Salvage value Estimated service life physical factors economic factors Methods of Depreciation Units of production Straight-line Sum-of-the-years’ digits Declining-balance method salvage value in not deducted in determining the depreciable base Group and composite methods composite depreciation rate no gain or loss on disposition Exercise 11-1 Cost Life (in years) Salvage value (a) Straight-line (b) Sum-of-the-years’ digits $518,000 12 $50,000 Exercise 11-1 (continued) (c) Double-declining balance Book value Rate Deprec Exp. Brief Exercise 11-6 Composite Depreciation Group Cost A $70,000 B 50,000 C 82,000 Salvage $7,000 5,000 4,000 Life 10 years 5 years 12 years Composite rate = Discarded an asset in Group A, $4,000 cost, 7 years old: Depreciation for Partial Years Determine depreciation for a full year Prorate between years Exercise 11-4d: Sum-of-the-years’ digits Total 2010 2011 2012 Depreciation Rate Revisions No correction of prior years No adjustments to “catch up” Brief Exercise 11-7 Original estimate: ($8,000 - $1,000)/5 = $1,400 Book value at time of revision: $8,000 - (2 x $1,400) = $5,200 New estimate: ($5,200 - $500)/2 = $2,350 IMPAIRMENTS 1. Recoverability test for impairment future net cash flows (undiscounted) < carrying value 2. If impaired, calculate the amount of the loss carrying value - fair value of the asset market value or PV of future net cash flows 3. Entry: Loss on Impairment 2,700 Accumulated Depreciation 2,700 Impairment Example Equipment: Taffy maker Original cost Accum depreciation Estimated life Annual rev: taffy production Annual cost: taffy production Fair value of taffy maker Cost of disposal $1,000,000 600,000 4 years $240,000 130,000 380,000 10,000 Impairment Example Equipment: Taffy maker Original cost Accum depreciation Estimated life Annual rev: taffy production Annual cost: taffy production Fair value of taffy maker Cost of disposal $1,000,000 550,000 4 years $240,000 130,000 380,000 10,000 DEPLETION Depletion Base Base Other Asset Exp. Acquisition costs Exploration costs Development costs tangible equipment intangible costs Restoration costs Recording Depletion Inventory Accumulated Depletion 250,000 250,000 Oil & Gas Full cost method all exploration costs are capitalized costs of unsuccessful exploration added to the cost of successful wells cannot capitalize more than the present value of the reserves Successful efforts method only costs of successful efforts are capitalized Special Depletion Issues Change in estimate of reserves accounting is the same as change in estimate of asset life Current value of reserves not recorded (recognized) must be disclosed by oil & gas companies increase in value of timber is not recorded Liquidating dividends dividends in excess of retained earnings credit the excess to Paid-in Capital Exercises 11-16 & 11-17 Carrying amount ($9M - $1M) Fair value Net realizable value 11-16 Asset still used (a) (a) $8,000,000 4,400,000 4,380,000 11-17 Asset not used 11-16 Asset still used 11-17 Asset not used (b) (b) (c) (c)