Transforming China and India: Challenges and Opportunities

advertisement

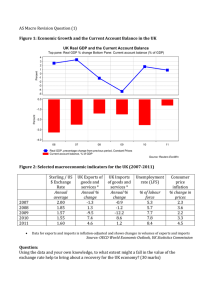

Transforming China and India: Challenges and Opportunities Chris Milner (GEP, School of Economics, University of Nottingham) Entry into the Global Economy • Before the 1990’s both China and India had highly protected and inward-looking economies – China’s (India’s) tariffs on imports averaged over 40% (90%) in 1992 and were complemented by an array of non-tariff barriers (licences, quotas & state trading restrictions) • Extent and speed of liberalisation and opening up of these two giants has been dramatic – in particular for China TARIFF RATES IN 2004 40.0% 36.9% Source: World Bank, World Development Indicators 35.0% 30.0% 28.1% 29.0% 28.0% 27.8% 25.3% 25.0% 20.0% 15.0% 10.0% 9.6% 9.6% 9.5% 6.2% 6.0% 5.8% 5.0% 0.0% Simple mean Weighted mean All Simple mean Weighted mean Primary China India Simple mean Weighted mean Manufactures China India 20 20 20 20 20 20 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 19 05 04 03 02 01 00 99 98 97 96 95 94 93 92 91 90 89 88 87 86 85 84 83 82 MERCHANDISE EXPORTS OVER GDP (per cent) 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% INDICES OF OPENNESS 2004 (per cent of GDP) South Korea Germany FDI inward stock China UK Total trade India Japan US 0 10 20 30 40 50 60 70 80 Comparative Growth Performance • Common features – control of population growth – role of trade liberalisation and export growth – growth clusters/uneven growth • Distinctive features – greater role of domestic savings and investment in China – greater role of FDI in technology-upgrading and export development in China – greater role of internal migration in China – greater role of manufacturing (services) sector in China (India) • China has substantially outperformed India GROWTH OF GDP IN INDIA AND CHINA (5-year moving averages per cent) Source: EIU 14.0 12.0 10.0 8.0 6.0 4.0 2.0 China India 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 0.0 STRUCTURE OF GDP, 2004 (per cent) 120% 100% 80% 41% 52% 60% 40% 46% 27% 20% 21% 13% 0% China India Agriculture Industry Services China and India in the Global Economy • Between 1990 and 2004 China and India’s exports grew considerably more rapidly than world exports – China is forecast to be world’s largest exporter by 2010 – of particular interest because much of the exporting is to the OECD countries – evidence of rapid technological upgrading in production and product terms • China and India already represent major markets, but have enormous further potential (given population size and scope for income growth) – the share of imports in GDP has grown rapidly – as yet, most of the imports are in raw materials, capital goods and intermediate goods ASIA'S SHARES IN WORLD EXPORTS OF MERCHANDISE (per cent) 30.0 25.0 20.0 15.0 2.5 10.0 6.0 6.7 7.5 6.4 6.4 5.9 2003 2004 2005 1.2 1.0 5.0 9.9 1.3 8.0 6.4 3.5 0.0 1948 1953 1963 1973 Japan China 1983 India 1993 Other Asia Challenges to the British Economy • Strong expectation that globalisation increases average incomes in long-run, but that there may be some groups that lose and shortterm adjustment costs – China, India and other emerging economies are increasing pace of adjustment required – particular concerns about employment and relative wage effects • Types of adjustment issues: – direct competition from imports to firms and workers, especially those involved in labour-intensive manufacturing and services – outsourcing of activities in import-competing and export-oriented activities in both manufacturing and services – direct export competition in these markets from upgrading domestic firms and in third markets from new exporters Opportunities for the British Economy • Direct exports of goods (associated with rise in production, incomes and technological-intensity) and services • Outward FDI opportunities in manufactures and services – platform for host markets and exporting – outsourcing to increase cost competitiveness • Inward FDI opportunities – outlet for trade surpluses? – platform for EU market? – ‘tariff-jumping’ motives? Comparative Data on China and India China India GNI per capita (current US $) 1740 720 Population 1304.5 1094.6 2.3 trillion 793 billion Sec. school enrolment(%) 72.5 53.5 Tertiary enrolment(%) 19.1 11.8 (millions) GNI (current US $) Note: 2005 data, except for education data which is for 2004 Challenges to Sustainability of Development in China and India • Common issues – inequality and social tensions – price distortions and infrastructure congestion (e.g. environmental) – structural issues (regional imbalances, state-owned enterprises) – low productivity in agriculture – degree of bureaucracy and regulation • Country-specific issues – fiscal deficit, low savings and absolute poverty in India – democratic challenge, weak banking sector and macro imbalances in China GNP per head Life Expectancy Male Adult literacy Female Adult literacy WELFARE Units 2004 $s PPP 2004 2002 2002 Under 5 mortality rate 2004, per 1,000 1995-2004 Under 5 malnutrition 2001 (China) Poverty Ratio (per 1999-2000 cent below $1 a day (India) at PPP) India China $5,890 $3,120 63 71 73% 95% 87% 48% 85 31 14.2% 44.9% 16.6% 34.7% Source: World Bank, World Development Indicators 2006 , UNDP, Human Development Report 2006, WTO, Recent Trade Developments 2006 Conclusions • China and India are increasing pace of globalisation • China in particular is rapidly catching-up technologically • Potential major adjustment challenges in OECD markets • Enormous potential for exporting, FDI and outsourcing • But some structural imbalances in China and India which may affect sustainability of current pace of development