Document 14988143

advertisement

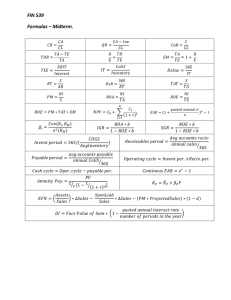

Matakuliah : F0282 - Analisis Laporan Keuangan Perusahaan Tahun : 2009 ASPEK LIKUIDITAS DAN ASPEK SOVABILITAS PERUSAHAAN Pertemuan 5 Murniadi Purboatmodjo ASPEK LIKUIDITAS A. Likuiditas: adalah kemampuan perusahaan untuk memenuhi kewajiban keuangannya sesegera mungkin/ pada saat ditagih. Keadaan ini adalah bila aktiva lancar lebih besar dari pada hutang lancar. Disebut :”likuid/likid”. Apabila tidak dapat dipenuhi : “illkuid” Rasio likuditas terdiri dari : 1. Current Ratio 3 A. 1. Current Ratio: Current Assets Current Liabilities o o o o Determines short-term debt-paying ability Focus is on the relationship between current assets and current liabilities - Inter-firm comparison is possible and meaningful Traditional benchmark: 2.00 - Decreased current ratio indicates lower liquidity - Industry averages provide contextual benchmark Considerations - Quality of inventory and receivables - Inventory cost flow assumptions 4 A. 2. Acid Test (Quick) Ratio o Measures the immediate liquidity of the firm o Relates the most liquid assets to current liabilities Exclude inventory More conservative variation: Also exclude other current assets that do not represent current cash flow o Traditional benchmark: 1.00 Industry averages provide contextual benchmark o Consideration Quality of receivables 5 Acid test (Quick) Ratio (Cont’d) First Method Current Assets - Inventory Current Liabilities Inventory should be removed from CA possible misleading in liquidity indication, because : (1) inventory may be slow moving, (2) possibly obsolete, (3) parts of the inventory may have been pledged to specific creditors, or (4) a valuation problem with the inventory (cost Vs a fair current valuation) 6 Acid test (Quick) Ratio (Cont’d) Second method Cash Equivalents + Marketable Securities + Net Receivables Current Liabilities It may also be desirable to achieve a view of liquidity that excludes some other CA that may not represent relatively current cash flow, such as prepaid or miscellaneous items Usually there is a very immaterial difference between the acid test computed under the first method and the second method, because the only difference in the computation is the inclusion of prepaids. But sometimes, there is a very material difference. 7 A. 3. Days’ Sales in Receivables Gross Receivables Net Sales 365 o o o Should mirror the company’s credit terms Gives an indication of the length of time that the receivables have been outstanding at the end of the year - Use of the natural business year (lower sales at year-end) can understate result Compare - Firm data for several years - Other industry firms and industry averages 8 A. 4. Accounts Receivable Turnover in times Net Sales Average Gross Receivables Indicates the liquidity of receivables o Determining average gross receivables o - End of year and beginning of year base points for average mask seasonal fluctuations - Internal analysis: use monthly or weekly amounts - External analysis: use quarterly data 9 A. 5. Accounts Receivable Turnover in Days Average Gross Receivables Net Sales 365 o o Similar to Number of Days’ Sales in Receivables except average receivables are used Should reflect firm’s credit and collection policies 10 A. 6. Days’ Sales in Inventory Ending Inventory Cost of Goods Sold 365 Indicates the length of time needed to sell all inventory on hand o Use of a natural business year - Understates number of day’s sale in inventory o - Overstates liquidity of inventory o Implications of extremes - High: excessive inventory for sales activity - Low: inventory shortage and lost sales 11 A. 7. Inventory Turnover Cost of Goods Sold Average Inventory o o Indicates the liquidity of inventory Determining average inventory - End of year and beginning of year base points for average mask seasonal fluctuations - Internal analysis: use monthly or weekly amounts - External analysis: use quarterly data 12 Aspek Solvabilitas B. Solvabilitas kemampuan perusahaan memenuhi kewajibannya apabila perusahaan tersebut dilikuidasi, baik kewajiban jangka pendek maupun jangka panjang. Keadaan ini bila perusahaan mempunyai aktiva atau kekayaan yang cukup untuk membayar semua hutangnya disebut“solvabel”. Kalau jumlah aktiva lebih kecil dari pada hutangnya disebut “Insolvabel” 13 B. 1. Debt Ratio Total Liabilities Total Assets Indicates the percentage of assets financed by creditors o Determine the firm’s ability to carry debt by comparing a company’s total liabilities with its total assets o Total Liabilities includes : ST liabilities, reserves, deferred tax liabilities, minority shareholders’ interest and redeemable preferred stock and any other non-current liability. It does not include : shareholders’ equity (convertible PS, PS, CS, capital in excess of stated value, foreign currency equity accounts, LT investment equity accounts, RE or TS) 14 B. 2. Debt/Equity Ratio Total Liabilities Shareholders' Equity Helps determine how well creditors are protected in case of insolvency o The lower the better the company position (from Lt debt-paying ability perspective) o Comparisons - Industry competitors and averages o 15 B. 3. Debt to Tangible Net Worth Ratio Total Liabilities Shareholders' Equity - Intangible Assets Determines the entity’s long-term debt payment ability o Indicates how well creditors are protected in case of the firm’s insolvency o More conservative than debt ratio or debt/equity ratio due to exclusion of intangibles o 16 B. 4. Times Interest Earned Recurring Earnings, Excluding Interest Expense, Tax Expense, Equity Earnings, and Minority Earnings Interest Expense, Including Capitalized Interest Indicates long-term debt-paying ability o Consider only recurring income - Exclude discontinued operations - Exclude extraordinary items o Exclude (add back) to income - Interest expense - Income tax expense - Equity losses (earnings) of nonconsolidated subsidiaries - Minority loss (income) o Include interest capitalized o 17 Times Interest Earned (cont’d) o o o Comparisons 3 to 5 years of historical data • Lowest value is the primary indicator of interest coverage Industry competitors and averages Secondary analysis Interest coverage on long-term debt Use only interest on long-term debt • Not practical for external analysis Short-run coverage Add back noncash expenses to recurring income Less conservative 18 C. Likuiditas dan solvabilitas: Dimungkinkan keadaan perusahaan : • Likuid dan solvabel • Likuid tetapi insolvabel • Illikuid tetapi solvabel • Illikuid dan insolvabel Perusahaan insolvabel dan illikuid kondisi keuangannya kurang baik, karena suatu waktu akan menghadapi kesulitan keuangan. Perusahaan illikuid akan segera kesulitan keuangan meskipun solvabel. Perusahaan insolvabel tapi likuid tidak segera mengalami kesulitan keuangan baru timbul kalau perusahaan dilikuidir 19 LATIHAN SOAL: FINANCIAL REPORTING AND ANALYSIS-GIBSON P6-16 dan /P7-9 20