Talking Point Schroders What do equity and credit markets say about

advertisement

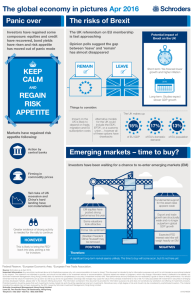

February 2016 Schroders Talking Point What do equity and credit markets say about global growth in 2016? Schroders Multi-Asset Investment Team The latest figures from our Economics team signal a slight easing in growth momentum with inflation unchanged. Likewise, our cyclical model continues to show a slowdown in the business cycle in the US and Japan. This is primarily because consumer-oriented indicators have slowed whilst macroeconomic and credit indicators have worsened. Overall, we have been in mild slowdown in the US for six months, Japan for 21 months but in expansion in Europe for the majority of 2015 where France, Italy and Spain have been compensating for weakness in Germany. Nevertheless, we have seen a modest improvement in global manufacturing PMI, consumer confidence, credit and inflation over the last three months, though this is concentrated in Europe. Generally speaking, the outlook remains uncertain. In particular, the trend in the credit markets is not supportive. A widening credit spread (the difference between the yield on a corporate bond and government bond of the same maturity) is not a healthy sign for the equity market or the economy as a whole. What is happening in credit markets? Since last year, spreads on US high yield bonds have widened on the back of energy related and idiosyncratic risks. These wider spreads imply a negative outlook; therefore investors expect to be compensated for taking on this extra risk. Over the last few months we have continued to see a divergence between equity and credit markets. Widening spreads are also a warning sign for equity investors though this has not been reflected in equity markets as they have not fallen to the same extent as high yield markets. What does this mean for growth? This divergence essentially shows that the two assets are pricing different economic outcomes. Credit markets are pricing in a recession while equities are reflecting a slow pace of growth. Historically, this divergence corrects either through robust earnings growth or a recession. We feel neither is likely in the near term. During the tech bubble of the late 1990s, credit spreads increased before equity prices reached their peak in 2000, and in 2007, credit spreads grew again, given their relation to the bubble in the US housing market. What does this mean for equities? Today, apart from a tightening in credit conditions, equity investors also need to contend with tighter monetary policy in the US. The Federal Reserve (Fed) raised interest rates in December, and the start of previous Fed SchrodersTalking Point Page 2 hiking cycles have often coincided with a contraction in multiples. The concern is that we have transitioned from a cyclical backdrop that used to provide a tailwind to equity markets to one that acts as a headwind. With markets at the top end of the cyclical range, we have to rely on earnings to do the heavy lifting. Therefore, a strong earnings cycle is critical for equity markets. Admittedly, our outlook for earnings is quite subdued. How should investors react? Under the surface, the tightening in credit conditions is influencing investor sentiment within equities. Leverage is being shunned as investors have started to avoid companies using debt to buy back equity. Indeed, balance sheet strength is back on the agenda, suggesting that the trend towards companies with strong balance sheets should persist. The mixed reading on economic and financial conditions means that equity investors need to prepare for higher volatility. Yet we believe that it is premature to get overly bearish. Our interpretation is that the current economic and market environment represents a late cycle expansion where cracks and market excesses emerge.To summarise, global activity is soft but the overall level is consistent with the global economy growing by a modest 2%. In this scenario we believe equities can deliver positive returns in such a benign environment. Important Information Any security(s) mentioned above is for illustrative purpose only, not a recommendation to invest or divest. This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The views and opinions contained herein are those of the author(s), and do not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The material is not intended to provide, and should not be relied on for investment advice or recommendation. Opinions stated are matters of judgment, which may change. Information herein is believed to be reliable, but Schroder Investment Management (Hong Kong) Limited does not warrant its completeness or accuracy. Investment involves risks. Past performance and any forecasts are not necessarily a guide to future or likely performance. You should remember that the value of investments can go down as well as up and is not guaranteed. Exchange rate changes may cause the value of the overseas investments to rise or fall. For risks associated with investment in securities in emerging and less developed markets, please refer to the relevant offering document. The information contained in this document is provided for information purpose only and does not constitute any solicitation and offering of investment products. Potential investors should be aware that such investments involve market risk and should be regarded as long-term investments. Derivatives carry a high degree of risk and should only be considered by sophisticated investors. This material, including the website, has not been reviewed by the SFC. Issued by Schroder Investment Management (Hong Kong) Limited. Schroder Investment Management (Hong Kong) Limited Level 33, Two Pacific Place, 88 Queensway, Hong Kong Telephone +852 2521 1633 Fax +852 2530 9095