FIN 5210: Investments Problem Set 1: Security Valuation

advertisement

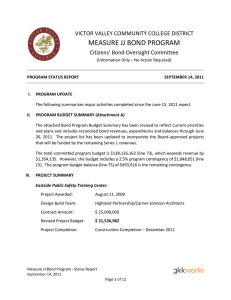

Practice Problems FIN 5210: Investments Fall 2014 Problem Set 1: Security Valuation 1. A bond is offered with face value of $1,000, a 10% coupon rate with semi-annual payments, and twenty years to maturity. If the market interest rate is 12%, what should be the price? 2. If the market interest rate rises to 15%, what will be the new price for the bond in question 1? 3. If the market interest rate drops to 9% instead, what will be the new price for the bond in question 1? 4. If the market interest rate changes to 8%, what will be the new price for the bond in question 1? 5. If the market interest rate rises to 10%, what will be the new price for the bond in question 1? Note that when the market rate equals the coupon rate, the price equals the face value. 6. If the market interest rate drops to 6% instead, what will be the new price for the bond in question 1? 7. If the market interest rate changes to 17%, what will be the new price for the bond in question 1? 8. If the market interest rate rises to 18%, what will be the new price for the bond in question 1? 9. If the market interest rate drops to 16% instead, what will be the new price for the bond in question 1? In the first three problems the market rate varied around 12%.1 In the next three problems it varied around 8% (changing by 2% both up and down). In the final three it varied around 17% (changing by 1% each way). Note that the capital gain from a decrease of x% in the market interest rate would be greater that the capital loss from an increase of x%. This relationship is known as convexity. 10. A bond is offered with face value of $1,000, a 10% coupon rate with semi-annual payments, and ten years to maturity. If the market interest rate is 12%, what should be the price? 11. If the market interest rate rises to 15%, what will be the new price for the bond in question 10? 1It changed by 3%, first going up from 12% to 15% and then going down from 12% to 9%. Page 1 of 6 Practice Problems FIN 5210: Investments Fall 2014 12. If the market interest rate drops to 9% instead, what will be the new price for the bond in question 10? 13. If the market interest rate changes to 8%, what will be the new price for the bond in question 10? 14. If the market interest rate rises to 10%, what will be the new price for the bond in question 10? 15. If the market interest rate drops to 6% instead, what will be the new price for the bond in question 10? 16. If the market interest rate changes to 17%, what will be the new price for the bond in question 10? 17. If the market interest rate rises to 18%, what will be the new price for the bond in question 10? 18. If the market interest rate drops to 16% instead, what will be the new price for the bond in question 10? Note that the capital gains or losses from changes in market interest rates are greater the longer the time to maturity. That is, bonds with longer maturities are riskier to hold. 19. A bond is offered with face value of $1,000, a 5% coupon rate with semi-annual payments, and twenty years to maturity. If the market interest rate is 12%, what should be the price? 20. If the market interest rate rises to 15%, what will be the new price for the bond in question 19? 21. If the market interest rate drops to 9% instead, what will be the new price for the bond in question 19? 22. If the market interest rate changes to 8%, what will be the new price for the bond in question 19? 23. If the market interest rate rises to 10%, what will be the new price for the bond in question 19? 24. If the market interest rate drops to 6% instead, what will be the new price for the bond in question 19? 25. If the market interest rate changes to 17%, what will be the new price for the bond in question 19? 26. If the market interest rate rises to 18%, what will be the new price for the bond in question 19? Page 2 of 6 Practice Problems FIN 5210: Investments Fall 2014 27. If the market interest rate drops to 16% instead, what will be the new price for the bond in question 19? 28. A bond is offered with face value of $1,000, a 5% coupon rate with semi-annual payments, and ten years to maturity. If the market interest rate is 12%, what should be the price? 29. If the market interest rate rises to 15%, what will be the new price for the bond in question 28? 30. If the market interest rate drops to 9% instead, what will be the new price for the bond in question 28? 31. If the market interest rate changes to 8%, what will be the new price for the bond in question 28? 32. If the market interest rate rises to 10%, what will be the new price for the bond in question 28? 33. If the market interest rate drops to 6% instead, what will be the new price for the bond in question 28? 34. If the market interest rate changes to 17%, what will be the new price for the bond in question 28? 35. If the market interest rate rises to 18%, what will be the new price for the bond in question 28? 36. If the market interest rate drops to 16% instead, what will be the new price for the bond in question 28? There is something else you should notice from the data you have generated in the above problems. The relative price changes2 resulting from a change in the market interest rate are not the same for all bonds of the same maturity. Price volatility is higher when the coupon rate is lower. This is known as coupon bias. 37. Calculate the duration for each of the bonds in problems 1, 10, 19, and 28. The duration is the weighted-average maturity of the package of payments, where the weights are determined by each payment’s portion of total present value. Do not try to calculate duration with the calculator. You would need to use a spreadsheet to calculate the PV of each payment and then get the average maturity, so you may want to use the answers given in the answer sheet. See how the duration reveals the effects of convexity and coupon bias. The longer the duration, the more sensitive the bond price is to interest rate fluctuations. 2That is, (Pnew – Pold) / Pold. Page 3 of 6 Practice Problems FIN 5210: Investments Fall 2014 38. A bond is offered with face value of $1,000, a 10% coupon rate with semi-annual payments, and twenty years to maturity. If the market price is $818.18, what market interest rate is implied? That is, what is the yield to maturity? 39. What is the yield to maturity for the above bond if the market price is $950? 40. What is the yield to maturity for the above bond if the market price is $850? 41. What is the yield to maturity for the above bond if the market price is $1,050? 42. What is the yield to maturity for the above bond if the market price is $1,150? 43. What is the yield to maturity for the above bond if the market price is $1,100? 44. What is the yield to maturity for the above bond if the market price is $1,025? 45. A high tax bracket investor is comparing two bond issues for possible inclusion in her portfolio. She expects market interest rates to be declining slowly but steadily over the foreseeable future. Bond A is a 6% ten-year Aaa-rated bond selling at $750.76. Bond B is an 8% ten-year Aaa-rated bond selling at $875.38. What is the yield to maturity for each bond, assuming semi-annual payment of coupons? Which would you recommend, based on the investor's expectations about future interest rates? She is not interested in current income, but rather in capital appreciation. 46. If the market interest rate is 15%, what should be the price of a share of 8% preferred stock with par value of $100? 47. If the market interest rate is 10%, what should be the price of a share of 8% preferred stock with par value of $100? 48. If the market interest rate is 12%, what should be the price of a share of 8% preferred stock with par value of $100? 49. If the market interest rate is 8%, what should be the price of a share of 8% preferred stock with par value of $100? 50. If a share of 8% preferred stock with par value of $100 is selling for $75, what is the market interest rate? 51. If a share of 8% preferred stock with par value of $100 is selling for $85, what is the market interest rate? 52. If a share of 8% preferred stock with par value of $100 is selling for $65, what is the market interest rate? 53. If a share of 8% preferred stock with par value of $100 is selling for $80, what is the market interest rate? Page 4 of 6 Practice Problems FIN 5210: Investments Fall 2014 54. Suppose an established family business is for sale to the employees. The family has already removed all the assets that can possible be taken from the business without killing its viability, so the only thing left of value would be the cash flows from future operations. The amount that can be committed for debt service is $10 million per year. The employee stock ownership trust has negotiated a loan with 15% interest that would be repaid with equal annual installments over a period of eight years. Calculate the price the employee ownership trust can pay for the business. 55. Art Grunnion wants to start a company that would build open-ocean speedboats of the highest possible quality. He would put $1 million into the company on September 18, 2014. Even with all its earnings plowed back into the company, he expects that he will have to follow up his initial investment with additional $1 million investments on the company's anniversary date in each of the next four years (2015, 2016, 2017 and 2018). In 2019 (assume that it will be on the 18th of September), he expects to be able to sell the company for $10 million. Calculate the expected IRR for this bit of “venture capital financing.” Is it a good investment, if the opportunity cost of capital is 15%? 56. A venture capital partnership is considering whether to fund a new pharmaceuticals research company. The initial investment to be paid immediately would be $5 million. Then the expectations for future investment are $10 million a year from now, $20 million two years from now, $50 million three years from now, and $100 million four years from now. Five years from now the venture capitalists expect to sell the company for $1 billion. Is it a good investment, if the opportunity cost of capital is 15%? Calculate NPV and IRR. 57. Common stock for Red River Enterprises paid a dividend of $1 per share this year, and dividends are expected to grow at the rate of 8% per year for the foreseeable future. If an investor assumes that the risk level of Red River warrants a 12% rate of return, what would be the intrinsic value per share, using the normal growth model developed by Myron Gordon? 58. Recompute the value of Red River common stock assuming an expected growth rate of 10%. 59. Recompute the value of Red River common stock assuming an expected growth rate of 11%. 60. Recompute the value of Red River common stock assuming an expected growth rate of 11.5%. 61. Recompute the value of Red River common stock assuming an expected growth rate of 11.9%. Note that the Gordon Model has a tendency to “explode” when the growth rate is close to the required return. What else is wrong with it? Page 5 of 6 Practice Problems FIN 5210: Investments Fall 2014 62. Assume Rf = 10% and Rm = 15%. What is the required rate of return for an investment with b = 2? 63. Assume Rf = 10% and Rm = 15%. A stock with b = 2 has expected return of 17%. Is it overvalued, undervalued, or correctly valued? 64. Assume Rf = 10% and Rm = 15%. A stock with b = .5 has expected return of 14%. Is it overvalued, undervalued, or correctly valued? 65. Assume Rf = 10% and Rm = 15%. A stock with b = 1.6 has expected return of 18%. Is it overvalued, undervalued, or correctly valued? 66. An investment is twice as risky as average, in terms of relevant risk. What is its beta? 67. An investment is half as risky as average, in terms of relevant risk. What is its beta? Page 6 of 6 Practice Problems FIN 5210: Investments Solutions: Set 1 1. FV is 1000, PMT is 50, interest per year is 12, P/YR is 2, N is 40, mode is END, calculate PV. The answer is $849.54. (The negative sign in the display is due to the sign convention.) 2. The only thing that needs to be changed in the calculator entries would be the interest per year, which now is 15. (Here are the other entries: FV is 1000, PMT is 50, P/YR is 2, N is 40, mode is END). When you calculate PV, the answer is $685.14. (The negative sign in the display is due to the sign convention.) 3. Once again, the only thing that needs to be changed in the calculator entries would be the interest per year, which now is 9. The PV is $1,092.01. 4. Once again, the only thing that needs to be changed in the calculator entries would be the interest per year, which now is 8. The PV is $1,197.93. 5. Interest per year is 10 (other entries remain unchanged from the above problems). PV is $1,000. 6. Interest per year is 6 (other entries remain unchanged from the above problems). PV is $1,462.30 7. Interest per year is 17 (other entries remain unchanged from the above problems). PV is $603.99. 8. Interest per year is 18 (other entries remain unchanged from the above problems). PV is $569.71 9. Interest per year is 16 (other entries remain unchanged from the above problems). PV is $642.26 10. FV is 1000, PMT is 50, interest per year is 12, P/YR is 2, N is 20, mode is END, calculate PV. The answer is $885.30. (The negative sign in the display is due to the sign convention.) 11. The only thing that needs to be changed in the calculator entries would be the interest per year, which now is 15. (Here are the other entries: FV is 1000, PMT is 50, P/YR is 2, N is 20, mode is END). When you calculate PV, the answer is $745.14. (The negative sign in the display is due to the sign convention.) 12. Interest per year is 9 (other entries remain unchanged from the above problems). PV is $1,065.04 13. Interest per year is 8 (other entries remain unchanged from the above problems). PV is $1,135.90 14. Interest per year is 10 (other entries remain unchanged from the above problems). PV is $1,000.00 15. Interest per year is 6 (other entries remain unchanged from the above problems). PV is $1,297.55 16. Interest per year is 17 (other entries remain unchanged from the above problems). PV is $668.78 17. Interest per year is 18 (other entries remain unchanged from the above problems). PV is $634.86 Prof. Kensinger Fall 2014 page 1 Practice Problems FIN 5210: Investments Solutions: Set 1 18. Interest per year is 16 (other entries remain unchanged from the above problems). PV is $705.46 19. FV is 1000, PMT is 25, interest per year is 12, P/YR is 2, N is 40, mode is END, calculate PV. The answer is $473.38. (The negative sign in the display is due to the sign convention.) 20. The only thing that needs to be changed in the calculator entries would be the interest per year, which now is 15. (Here are the other entries: FV is 1000, PMT is 25, P/YR is 2, N is 40, mode is END). When you calculate PV, the answer is $370.28. (The negative sign in the display is due to the sign convention.) 21. Interest per year is 9 (other entries remain unchanged from the above problems). PV is $631.97 22. Interest per year is 8 (other entries remain unchanged from the above problems). PV is $703.11 23. Interest per year is 10 (other entries remain unchanged from the above problems). PV is $571.02 24. Interest per year is 6 (other entries remain unchanged from the above problems). PV is $884.43 25. Interest per year is 17 (other entries remain unchanged from the above problems). PV is $321.13 26. Interest per year is 18 (other entries remain unchanged from the above problems). PV is $300.77 27. Interest per year is 16 (other entries remain unchanged from the above problems). PV is $344.15 28. FV is 1000, PMT is 25, interest per year is 12, P/YR is 2, N is 20, mode is END, calculate PV. The answer is $598.55. (The negative sign in the display is due to the sign convention.) 29. The only thing that needs to be changed in the calculator entries would be the interest per year, which now is 15. (Here are the other entries: FV is 1000, PMT is 25, P/YR is 2, N is 20, mode is END). When you calculate PV, the answer is $490.28. (The negative sign in the display is due to the sign convention.) 30. Interest per year is 9 (other entries remain unchanged from the above problems). PV is $739.84 31. Interest per year is 8 (other entries remain unchanged from the above problems). PV is $796.15 32. Interest per year is 10 (other entries remain unchanged from the above problems). PV is $688.44 33. Interest per year is 6 (other entries remain unchanged from the above problems). PV is $925.61 34. Interest per year is 17 (other entries remain unchanged from the above problems). PV is $432.20 Prof. Kensinger Fall 2014 page 2 Practice Problems FIN 5210: Investments Solutions: Set 1 35. Interest per year is 18 (other entries remain unchanged from the above problems). PV is $406.64 36. Interest per year is 16 (other entries remain unchanged from the above problems). PV is $460.00 37. 8.20 years, 6.31 years, 9.42 years, 7.27 years 38. P/YR is 2, mode is END, FV is 1000, PMT is 50, N is 40, PV is –818.18, calculate the interest per year. (The negative sign for PV is due to the sign convention.) Answer is 12.49% 39. PV is –950 (other entries remain unchanged from problem 38). Interest per year is 10.61% 40. PV is –850 (other entries remain unchanged from problem 38). Interest per year 11.99% 41. PV is –1050 (other entries remain unchanged from problem 38). Interest per year 9.44% 42. PV is –1150 (other entries remain unchanged from problem 38). Interest per year 8.43% 43. PV is –1100 (other entries remain unchanged from problem 38). Interest per year 8.92% 44. PV is –1025 (other entries remain unchanged from problem 38). Interest per year 9.71% 45. Both bonds yield 10%; but she would pick Bond A because it gives lower reinvestment risk and a smaller income tax burden, with the same yield. Given her expectations for declining interest rates, bond A would also offer a higher expected capital gain. 46. P0 = $8 / 0.15 = $53.33 47. P0 = $8 / 0.10 = $80.00 48. P0 = $8 / 0.12 = $66.67 49. P0 = $8 / 0.08 = $100.00 50. R = 8 / 75 = 10.67% 51. R = 8 / 85 = 9.41% 52. R = 8 / 65 = 12.31% 53. R = 8 / 80 = 10.00% 54. See Example 7, Topic 3, slide 58. Value is $44.9 million 55. See Example 8, Topic 3, slide 59. IRR is 24.07% 56. See Example 9, Topic 3, slide 60. IRR is 108.99% 57. P0 = (1 x 1.08) / (0.12 – 0.08) = $27.00 58. P0 = (1 x 1.10) / (0.12 – 0.10) = $55.00 59. P0 = (1 x 1.11) / (0.12 – 0.11) = $111.00 60. P0 = (1 x 1.115) / (0.12 – 0.115) = $223.00 61. P0 = (1 x 1.119) / (0.12 – 0.119) = $1,119.00 62. Rrequired = 10% + 2(15% – 10%) = 20% 63. Since the required return is 20%, the expected return at the current price is too low. The price will have to come down. The stock is currently overvalued. Prof. Kensinger Fall 2014 page 3 Practice Problems FIN 5210: Investments Solutions: Set 1 64. Rrequired = 10% + 0.5(15% – 10%) = 12.5%. Since the required return is 12.5%, the expected return at the current price is too high. The price will have to rise. The stock is currently undervalued. 65. . Rrequired = 10% + 1.6(15% – 10%) = 18% Since the required return is 18%, the expected return at the current price is just right. The stock is priced at equilibrium. 66. β=2 67. β = 0.5 Prof. Kensinger Fall 2014 page 4 FIN 5210: Investments Practice Problems Solutions: Set 1 Table Illustrating Coupon Bias and Convexity old rate new rate old price 20-year, 10% bonds 12% 12% 8% 8% 17% 17% 15% 9% 10% 6% 18% 16% 10-year, 10% bonds 12% 12% 8% 8% 17% 17% 20-year, 5% bonds 10-year, 5% bonds Prof. Kensinger new price capital gain (loss) relative change $849.54 $849.54 $1,197.93 $1,197.93 $603.99 $603.99 $685.14 $1,092.01 $1,000.00 $1,462.30 $569.71 $642.26 ($164.40) $242.47 ($197.93) $264.37 ($34.28) $38.27 -19.35% +28.54% -16.52% +22.07% -5.68% +6.34% 15% 9% 10% 6% 18% 16% $885.30 $885.30 $1,135.90 $1,135.90 $668.78 $668.78 $745.14 $1,065.04 $1,000.00 $1,297.55 $634.86 $705.46 ($140.16) $179.74 ($135.90) $161.65 ($33.92) $36.68 -15.83% +20.30% -11.96% +14.23% -5.07% +5.48% 12% 12% 8% 8% 17% 17% 15% 9% 10% 6% 18% 16% $473.38 $473.38 $703.11 $703.11 $321.13 $321.13 $370.28 $631.97 $571.02 $884.43 $300.77 $344.15 ($103.10) $158.59 ($132.09) $181.32 ($20.36) $23.02 -21.78% +33.50% -18.79% +25.79% -6.34% +7.17% 12% 12% 8% 8% 17% 17% 15% 9% 10% 6% 18% 16% $598.55 $598.55 $796.15 $796.15 $432.20 $432.20 $490.28 $739.84 $688.44 $925.61 $406.64 $460.00 ($108.27) $141.29 ($107.71) $129.46 ($25.56) $27.80 -18.09% +23.61% -13.53% +16.26% -5.91% +6.43% Fall 2014 page 5 FIN 5210: Investments Practice Problems Solutions: Set 1 Illustration of Convexity $1,200.00 $1,000.00 Price $800.00 $600.00 $400.00 20-year $200.00 10-year 5-year 1-year $0.00 1 3 5 7 9 11 13 15 Rate Prof. Kensinger Fall 2014 17 19 21 23 25 27 29 (%) page 6