December Market Commentary

advertisement

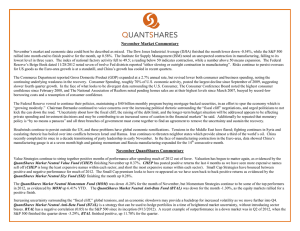

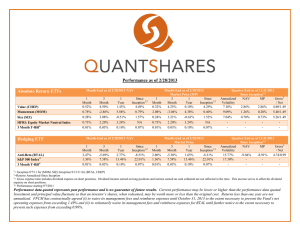

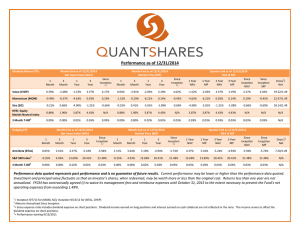

December Market Commentary December’s positive returns capped a strong year in the equity markets. The Dow Jones Industrial Average (DJIA) finished up 0.60%, and the S&P 500 returned 0.91% for December. Similar to November, December’s market and economic data could best be described as mixed. The Institute for Supply Management (ISM) PMI experienced a rebound in December after an unexpected contraction in manufacturing in November, which registered the lowest reading in three years. December showed a reading of 50.7, which indicated growth in the overall economy for the 43rd consecutive month; a reading above 50 indicates expansion, while a number below 50 means contraction. The markets continue to digest what looks to be divergent data surrounding the U.S. consumer. The U.S. employment picture continues its gradual improvement, but has not shown the signs necessary to significantly address the elevated unemployment issues facing the country as we slowly emerge from the Great Recession. New home sales data released in December showed the fastest pace in 2 ½ years, and home prices climbed more than forecast according to the S&P/Case-Schiller Index. A sustained pick-up in housing, buoyed by record-low borrowing costs, and increased consumer spending, is helping to sustain the economic recovery. The Conference Board’s Consumer Confidence Index however noted a drop in consumer confidence in December to 65.1 from a revised November number of 71.5, which was the highest consumer confidence since February 2008. The Federal Reserve policymakers in a surprising decision linked interest rates to unemployment and inflation. The Federal Open Market Committees statement noted “rates will remain low at least as long as unemployment remains above 6.5% and inflation is 2.5% or lower.” The Fed also vowed to continue their policies, maintaining a $40 billion monthly program buying mortgage-backed securities, and initiated an additional $45 billion of Treasury purchases, in an effort to spur the economy. The United States Congress was able to come to an agreement to avert the “fiscal cliff”, however long term budget problems still persist. The ability for the government to come to a sensible solution on both entitlement and tax reform remains to be seen, and these issues will continue to cast a shadow of uncertainty onto the market. December QuantShares Commentary Value strategies finished the year on a high note after struggling through the first half of 2012. Value delivered a strong second half, propelled higher most notably by performance in Q4 as markets bounced around on heightened volatility. As valuation started to matter again to the equity market, we have seen the QuantShares Market Neutral Value Fund (CHEP) record strong performance, finishing December up 1.65% and Q4 up 4.94%. CHEP has posted positive returns the last 5 months, as we have seen more expensive names sell off (CHEP is long the least expensive names, and short the most expensive names within each sector, respectively). Small Cap Strategies have bounced between positive and negative performance for much of 2012. The Small Cap premium looks to have re-appeared as we have seen a strong back half finish to 2012 for small cap names. This can be seen with the QuantShares Market Neutral Size Fund (SIZ) finishing December up 1.66% and Q4 up 2.16%. Momentum Strategies, although remaining positive performers for the calendar year 2012, gave back much of their first half outperformance, as these strategies faded into year end. This can be evidenced by the QuantShares Market Neutral Momentum Fund (MOM) which was down -2.40% for the month of December and -2.25% in Q4. The QuantShares Market Neutral Anti-Beta Fund (BTAL) was down for the month -5.03%, as the equity markets rallied for a positive finish. In early December we highlighted a Fund of Funds portfolio in our white paper “Momentum the Yin to Values Yang” where an equal weighting was applied to both MOM and CHEP to construct a low volatility, low correlation portfolio with similar characteristics to the un-investable HFRI Market Neutral Index. The first full calendar year of performance for a similarly constructed portfolio using the QuantShares ETFs returned 2.19% compared to 3.27% for the HFRI Market Neutral Index. Performance as of 12/31/2012 Absolute Return ETFs Month-End as of 12/31/2012 NAV Month-End as of 12/31/2012 Market Price (MP) 1 3 1 Since Month Month Year Inception* 1.69% 5.08% 0.07% 2.86% -3.36% -3.48% 2.22% 0.20% Quarter End as of 12/31/2012 Since Inception* Annualized NAV MP Gross** Volatility / Net 7.29% 2.86% 2.86% 4.80/1.49 9.45% 1.26% 0.20% 5.40/1.49 Value (CHEP) Momentum (MOM) 1 Month 1.65% -2.40% 3 Month 4.94% -2.25% 1 Year 0.11% 3.86% Since Inception* 2.86% 1.26% Size (SIZ) 1.66% 2.16% -0.52% 0.70% 1.91% 2.33% -0.04% 0.73% 7.27% 0.70% 0.73% 5.26/1.49 HFRI: Equity Market Neutral Index 3 Month T-Bill*** 0.50% 0.01% 1.18% 0.02% 3.26% 0.04% NA 0.04% 0.50% 0.01% 1.18% 0.02% 3.26% 0.04% NA 0.04% - - - - Hedging ETF Month-End as of 12/31/2012 NAV Anti-Beta (BTAL) S&P 500 Index*** 1 Month -5.03% 0.91% 3 Month -5.85% -0.36% 1 Year -7.93% 16.02% Since Inception* -9.04% 19.67% 3 Month T-Bill*** 0.01% 0.02% 0.04% 0.04% Month-End as of 12/31/2012 Market Price 1 3 1 Since Month Month Year Inception* -4.77% -5.56% -7.52% -8.91% 0.91% -0.36% 16.02% 19.67% 0.01% 0.02% 0.04% 0.04% Quarter End as of 12/31/2012 Since Inception* Annualized NAV MP Gross** Volatility / Net 16.38% -9.04% -8.91% 4.74/0.99 17.66% - - - - *= Inception 9/7/11 for (MOM, SIZ); Inception 9/13/11 for (BTAL, CHEP) **= Gross expense ratio includes dividend expense on short positions. Dividend income earned on long positions and interest earned on cash collateral are not reflected in the ratio. This income serves to offset the dividend expense on short positions. ***= Performance starting 9/7/2011 Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Returns less than one year are not annualized. FFCM has contractually agreed (i) to waive its management fees and reimburse expenses until October 31, 2013 to the extent necessary to prevent the Fund’s net operating expenses from exceeding 1.49% and (ii) to voluntarily waive its management fees and reimburse expenses for BTAL until further notice to the extent necessary to prevent such expenses from exceeding 0.99%. Company Overview: QuantShares designs and manages Market Neutral ETFs to provide exposure to well-known equity factors such as Momentum, Value, Beta and Size. QuantShares Market Neutral ETFs are the first ETFs that have the capability to short physical stocks (as opposed to derivatives) that passively track indexes. Our ETFs offer investors a diversifying asset that is both highly liquid and fully transparent. The ETFs are designed to generate spread returns, diversify risk and reduce volatility. Value, Size and Momentum tend to be more strategic in nature and provide strong risk-adjusted returns; Anti-Beta tends to be more tactical and allows investors to hedge or express short term investment convictions. QuantShares Market Neutral ETFs provide a liquid alternative to help dampen volatility and enhance the risk return profile of an investment portfolio. Disclosures: Before investing you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. This and other information is in the prospectus, a copy of which can be obtained by visiting the Fund’s website at www.quant-shares.com. Please read the prospectus carefully before you invest. Foreside Fund Service, LLC, Distributor. Shares are not individually redeemable and can be redeemed only in Creation Units. The market price of shares can be at, below or above the NAV. Market Price returns are based upon the midpoint of the bid/ask spread at 4:00PM Eastern time (when NAV is normally determined), and do not represent the returns you would receive if you traded shares at other times. Fund returns assume that dividends and capital gains distributions have been reinvested in the Fund at NAV. Some performance results reflect expense subsidies and waivers in effect during certain periods. Absent these waivers, results would have been less favorable. Risks: There is no guarantee that the funds will reach their objective. An investment in the Funds is subject to risk including the possible loss of principal amount invested. See prospectus for specific risks regarding each Fund. There is a risk that during a “bull” market, when most equity securities and long only ETFs are increasing in value, the Funds’ short positions will likely cause the Fund to underperform the overall U.S. equity market and such ETFs. The Funds may not be suitable for all investors. Short selling could cause unlimited losses, derivatives could result in losses beyond the amount invested, and the value of an investment in the Fund may fall sharply. Beta is a measure of an asset’s sensitivity to an underlying index. Long is purchasing a stock with the expectation that it is going to rise in value. Short is selling stock with the expectation of profiting by buying it back later at a lower price. Negative correlation is a relationship between two variables in which one variable increases as the other decreases. HFRI EH: Equity Market Neutral Index incorporates equity market neutral strategies including both Factor-based and Statistical Arbitrage/Trading Strategies. Equity Market Neutral Strategies typically maintain characteristic net equity market exposure no greater than 10% long or short. DJIA – Dow Jones Industrial Average is a price weighted average of 30 significant stocks traded on the NYSE and NASDAQ. S&P 500 is an index of 500 large cap common stocks actively traded on the NYSE and NASDAQ. One cannot invest directly in an index.