option, seven will take the monthly benefit, eight intend to... lump sum payment, and three have chosen to defer their...

advertisement

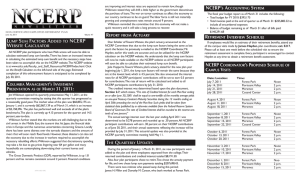

Quarterly Investments Increases Last Quarter of the Fiscal Year NON-CERTIFICATED EMPLOYEES RETIREMENT PLAN December 20, 2007 Volume 33 Clifton Gunderson’s Annual Auditor’s Report Brings Good News Mr. Mike Hillary of Clifton Gunderson had indicated the annual auditor’s report was conducted in accordance with auditing standards generally accepted in the United States of America. In his opinion, the financial statements were represented fairly, in all material respects, the financial status of the Non-Certificated Employees Retirement Plan of the Junior College District of St. Louis, St. Louis County, Missouri as of June 30, 2007. Also, the changes in the Plan’s financial status for the year ended in conformity with accounting principles generally accepted in the United States of America. A brief summary of the audits financial highlights are as follows; the net assets available for benefits at the beginning of year, July 1, 2006, equaled $56,542,321, compared to the net assets available as of June 30, 2007 totaled $63,339,186, which represents an increase of nearly $6.8 million from the previous year. Total investment income was $9,216,885, less the investment expenses of $134,647, resulting in the total net investment income totaling $9,082,238. Also, contributions made by the College and participants were $887,712 each, totaling $1,775,424. Total deductions including benefits paid to participants and administrative expenses add up to $4,060,797, and the net increase during the auditing period was $6,796,865. Plan enhancements that went into effect in July 2007 were also evaluated by Mr. Hillary, and his parting comments at the end of his presentation at the August 14, 2007 quarterly committee meeting, were that the Plan had a good year and is well funded. Mr. Wilkinson, Senior Portfolio Strategist, Columbia Management, began his quarterly report at the beginning of the November 14, 2007, NCERP quarterly committee meeting by stating the stock market, bond market, money markets and foreign markets have all been impacted by the sub-prime mortgage situation. The Federal Reserve has lowered rates twice and cut the discount rate by 50 percent. Due to current conditions of the stock market, special attention has been paid to value stocks in terms of performance in contrast with the performance of growth stocks. The conclusion is that growth stocks have outperformed value stocks by 4.5 percent. The NCERP Committee has determined that replacing value stocks with growth stocks would be an excellent opportunity to increase the Plans overall growth, with minor risks. The NCERP committee unanimously agreed to implement this change in the Plan’s portfolio. Beginning market value of the portfolio as of July 1, 2007, was $63,351,171. Net contributions and withdrawals were $222,522; income earned was $446,956; and the change in market value is $1,317,087, resulting in an ending market value as of September 30, 2007, of $64,892,693. Report of the Annual Actuarial Valuation as of June 30, 2007 Mr. Schisler began his report by summarizing the results of the 7/1/07 NCERP valuation. During the period July 1, 2006 – June 30, 2007, the Plan’s demographic experience was favorable. The valuation data showed actual salary/compensation increases lower than expected, with an average of 4.10% versus the assumed 4.75%. Also, the asset returned to the Plan was much better than anticipated with an actual 16.70% increase from investment gains versus the assumed 7.75%. This is the best rate of investment return on Plan assets since approximately 1999. Continued favorable experience keeps the Plan in a positive position for the future. The Plan remains in a surplus position in 2007, and there are no contribution shortfalls. Assets cover 92% of benefits, and the Plan is in a strongly funded position. Mr. Schisler suggests that this may be an opportunity to consider implementing small to moderate Plan enhancements, but that the committee first consider updating the mortality table used in the actual valuation. The Plan’s annual actuarial valuation was provided at the November 14, NCERP quarterly committee meeting. Latest News on the Voluntary Separation Program (VSP) Nineteen Plan participants are leaving the College under the provisions of the Voluntary Separation Program. Mr. Hayden has contacted each participant. One participant intends to take the 50/50 option, seven will take the monthly benefit, eight intend to take a lump sum payment, and three have chosen to defer their retirement benefit. Special Note: Those retirees who will be retiring January 1, 2008 under VSP will incur an unavoidable delay in benefit payment due largely to a minor delay in determining their salary for 2007. This important element is required in order to determine the amount of benefit payment and will not be determined until after January 18, 2008 according the College’s payroll department. As soon as this information is available, the Retirement Committee will ensure payouts; both lump sums, as well as annuity payments, will be processed as quickly thereafter as possible. No payments are expected to be delayed beyond January 31, 2008. Thanks to all those affected NCERP participants for their patience and please plan financial obligations accordingly. The Quarterly Updates Mr. Hayden reported that during the period of July 1, 2007 through September 30, 2007, 14 new participants were added to the Plan. During that same period, three Plan participants chose to retire effective August 1, 2007. One individual chose to receive monthly benefits whereas the other two selected the lump sum payment option. The payout for the individuals requesting a cash settlement is $166,601.17. No deaths were reported during the reporting period. Also during this period, 12 employees separated from the College. The contributions and credited interest of those individuals totaled $119,937.49 and has been successfully paid to each of the terminated employees. NCERP’S Accounting System Fiscal year budget report as of September 30, 2007, includes the following: • The total budget for 2006-2007 fiscal year: $371,531.00 • Total charges that have been paid: $65,895.15 • Encumbered charges: $17,598.550 • Balance as of September 30, 2007: $288,037.35 Administrative expenses for the retirement plan are currently budgeted at $371,531.00. Less than the industry standard of 1% of the total value of assets managed. Retirement Interview Schedule If employees would like an estimate of their retirement benefits, please attend any of the campus visits made by James Hayden, plan coordinator. Please call at least a week before the scheduled visit to ensure the retirement assessment is complete. Every participant is encouraged to contact the Plan Coordinator at any time to obtain a retirement benefit assessment. Date January 10, 2008 January 17, 2008 January 24, 2008 February 7, 2008 February 14, 2008 February 21, 2008 February 28, 2008 March 6, 2008 March 13, 2008 March 20, 2008 April 3, 2008 April 10, 2008 April 17, 2008 April 24, 208 May 1, 2008 May 8, 2008 May 15, 2008 June 5, 2008 June 12, 2008 June 19, 2008 June 26, 2008 Location Forest Park Florissant Meramec Forest Park Florissant Meramec Cosand Center Forest Park Florissant Valley Meramec Forest Park Florissant Valley Meramec Cosand Center Forest Park Florissant Valley Meramec Forest Park Florissant Valley Meramec Cosand Center NCERP Committee Meeting Schedule Time 12 Noon 2 p.m. 2 p.m. 12 Noon 2 p.m. 2 p.m. 2 p m. 12 Noon 2 p.m. 2 p.m. 12 Noon 2 p.m. 2 p.m. 2 p.m. 12 Noon 2 p.m. 2 p.m. 12 Noon 2 p.m. 2 p.m. 2 p.m. S M T W T F S Locations are: Meramec, BA-105; Florissant Valley, Training Center, TC-109; Forest Park, Executive Dean’s Conference Room; and Cosand Center, Room 208. Points of contact: The NCERP committee representatives are listed on the back panel of this brochure: Plan participants are encouraged to attend the committee’s quarterly meetings at the Forest Park campus, Room L-007. The tentative time and dates are listed below: February 13, 2008, Cosand Center 9:15 a.m. May 14, 2008, Forest Park 9:15 a.m. August 13, 2008, Florissant Valley 9:15 a.m. November 12, 2008, Meramec 9:15 a.m. Beneficiary Accuracy Please make sure beneficiary information on file for NCERP retirement contributions is accurate. Failure to do so could result in retirement contributions being paid to the employee’s estate versus having the contributions going to loved ones. If there are questions or concerns, contact James Hayden, plan coordinator at ext. 5217. Unofficial.… Which Money to Touch First in Retirement? Retirees typically have their money in various accounts including taxdeferred savings such as IRAs, 401(k) plans, or annuities and taxable investment accounts such as CDs bonds, or other securities. You’ve got social security earnings coming your way and if you’re lucky, perhaps a pension plan. To get the most from your savings, after taxes, you need to know which accounts to tap first and which to leave until last. “Individual situations, and tax consequences, can lead to different ‘best’ paths for different retirees,” says Peg Downey, a Maryland financial Planner, “but there are some standard guidelines to follow.” Taxable Accounts. Most people should draw on money from taxable assets before dipping into tax-protected accounts such as traditional IRAs, 401(k)s, and other qualified plans, says financial advisor and attorney Gary Schatsky, president of ObjectiveAdvice.com. “This way your money can continue to grow and compound tax-deferred until 70?, when you must take some of the money,” he says. Savvy investors in lower tax brackets, such as the 15% tax bracket, may elect to take distribution prior to 70?, which adds to their gross income for that year putting them at the top of the tax bracket. Thus, they pay tax now, but at what may be a lower rate than they would pay in the future. They also preserve some of their taxable portfolio. • Interest from bank CDs, bonds and money market funds is taxed at ordinary income rates. Long-term capital gains on profits from the sale of assets you’ve held from at least a year are taxed generally at 15% or 5% for those in the lowest two tax brackets. Most stock dividends also are taxed at 15%. Keep in mind that for any dividends, interest, or capital-gains payouts, taxes are due on the tax returns prepared for the year you receive them. • U. S. Government bonds are free from state taxes. Municipal bonds are free from federal tax and state taxes too, if you live in a state that issued them. • Pension and annuity payment from qualified retirements are fully taxable. Some states exempt certain types of pensions from state income taxes such as military or government pensions. Others allow a portion of any type of pension income to escape state income taxes. Check with your tax advisor. Tax deferred accounts. Ideally, you want to benefit from tax deferral for as long as possible. Once you reach age 70 ?, however, there is a minimum withdrawal schedule, based on your life expectancy, from traditional IRAs and 401(k) or 403(b) plans. This schedule is designed to ensure that you make a concerted effort to drain the account so the government can collect taxes on the money before you die. To figure how much you need to take out, check the tables on the IRS Web site www.irs.gov/pub/irs-pdf/p590.pdf or consult a tax advisor. You’re taxed at ordinary income tax rates on the amount you withdraw. If you don’t withdraw the required amount each year, the IRS will assess you with a 50% penalty of the minimum withdrawal due. Missing required minimum distribution is perhaps the single biggest mistake for IRA owners. Once you determine your required minimum distribution, you can take the money from any traditional IRA accounts you own. You can take the full required amount from one IRA to satisfy the calculated requirement for each of your IRAs. But you still have to take additional required minimum distributions from qualified plans such as a 401(k). In other works, an IRA distribution can’t be increased to satisfy the required distribution of a 401(k) or other tax-deferred plan. If you roll your existing 401(k) into an IRA, however, you can avoid taking two distributions; taking one from the IRA will suffice. Bottom line: The rollover helps you keep more of your money. When you request your required minimum distribution, you might want to consider having it automatically invested in shares of stock or mutual funds, instead of cash. Although you will still pay taxes, you can keep it invested and, hopefully, it will appreciate over time, explains financial planner Mary Malgoire. Annuities. If you have an annuity and want to draw on it to cover living expenses, plan to take to payout as a continual stream of regular payments throughout retirement. Though you’ll be offered the options of withdrawing the payout in lump sum or in a series of unscheduled withdrawals, you’d have to pay ordinary income tax immediately on all of the earnings. Receiving a lump sum could result in a large tax bill, so consider it carefully. In many situations, it’s better to pay taxes in stages, leaving the rest of your money in your account to potentially grow tax-deferred. Roth IRAs and Roth IRA 401(k) plans. The IRS already taxed the contributions you made to these accounts. So once you retire and decide to withdraw these funds, you won’t owe taxes on the earnings – provided you’re at least 59 ? years and have held the account for at least five years. You don’t have to take any minimum distributions from these, even after age 70 ?. “Let ‘em ride,” Mr. Schatsky counsels. “This should be the last account you tap. You want to keep that tax-free growth working.” Points of Contact: Board of Trustees Appointment CALLA WHITE 6688 Chesapeake Drive Apartment C Florissant, Missouri 63033 Phone: (314) 355-9112 Term expires: BOT’s pleasure Board of Trustees Appointment RUTH LEWIS 10455 Litzsinger Road St. Louis, MO 63131 Telephone: (314) 567-7098 Term Expires: BOT’s pleasure Non-Unit Representative TIM O’NEILL, vice chairman MC - Printing Telephone: (314) 984-7709 e-mail: toneill@stlcc.edu Term expires: June 30, 2008 Unit Representative KEVIN WHITE CC – TESS Systems Operations Office Phone: (314) 539-5058 E-mail: kwhite@stlcc.edu Term expires: June 30, 2010 Physical Plant Mike Wibbenmeyer MC – Utilities/HVAC Phone: (314) 984-7749 E-mail: mwibbenmeyer@stlcc.edu Term expires: June 30, 2009 Any suggestions for improvements, questions, comments or other concerns about the retirement plan may be directed to any of the NCERP committee representatives. Any proposed agenda items may be sent to James Hayden or the employee representative 10 days prior to the meeting date. Individuals with speech or hearing impairments may call via Relay Missouri by dialing 711. St. Louis Community College FLORISSANT VALLEY FOREST PARK MERAMEC WILDWOOD ACCOMMODATIONS STATEMENT St. Louis Community College makes every reasonable effort to accommodate individuals with disabilities. If you have accommodation needs, please contact the Access office at the campus where you are registering at least six weeks before the beginning of the class. Event or other public service accommodation requests should be made with the event coordinator or applicable location non-discrimination officer at least two working days prior to the event or public service. NON-DISCRIMINATION STATEMENT St. Louis Community College is committed to non-discrimination and equal opportunities in its admissions, educational programs, activities and employment regardless of race, color, creed, religion, sex, sexual orientation, national origin, ancestry, age, disability or status as a disabled or Vietnam-era veteran and shall take action necessary to ensure non-discrimination. This newsletter is designed to summarize and explain basic changes in the Non-Certificated Employees Retirement Plan and provides updates on other related matters. Since it is only a summary, this newsletter does not cover the Plan's provisions in detail. Therefore, if there is any conflict between this newsletter and the Plan document itself, the Plan document will always govern. An official copy of the Plan is available for inspection in the Human Resources Department at the Joseph P. Cosand Community College Center, 300 South Broadway, St. Louis, MO and in each campus’ library during regular business hours. 100386 12/07