• Research Support

advertisement

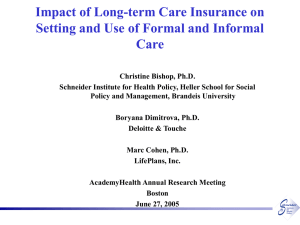

Impact of Long-term Care Insurance on Setting and Use of Formal and Informal Care Research Support • Health Care Financing and Organization, an Christine Bishop, Ph.D. Schneider Institute for Health Policy, Heller School for Social Policy and Management, Brandeis University initiative of Robert Wood Johnson Foundation • Data developed in previous projects supported Boryana Dimitrova, Ph.D. Deloitte & Touche by ♦ ASPE/ Office of the Assistant Secretary for Planning and Evaluation, Department of Health and Human Services ♦ Robert Wood Johnson Foundation/HCRI Marc Cohen, Ph.D. LifePlans, Inc. AcademyHealth Annual Research Meeting Boston June 27, 2005 2 The Fastest Growing Segment of the LTCI Market is Employer-Sponsored The LTCI Market Has Experienced Steady Growth Average Annual Growth Rates in the LTC Insurance Marketplace (1991-2001) 10000 9000 22% 7,529 6,831 7000 20 6,080 6000 18% 5,542 4,960 5000 4,351 3,837 4000 3,417 2,930 3000 2,430 2000 1000 25 8,261 8000 Percent Policies Sold (In Thousands) 9,000 1,550 815 12% 10 6% 1,930 1,130 5 0 1987 15 1992 1997 Source: LifePlans computations; Number of Long-Term Care Insurance Policies Sold, Cumulatively 1987-2002 estimates AAHP-HIAA LTC Market Survey 2003. Includes preliminary numbers for 2002. 0 2002 3 Total Individual Source: HIAA LTC Market Survey 2003: Lifeplans Computations Employer Life Riders 4 Estimated Market Penetration 2002 Long-Term Care Insurance 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% 9% 6% A “contingent claim” Provides holder with more resources when the insured “event” (disability) occurs 4% If the event occurs, resources have high value for consumption Age 45+ Ages 45 to 64 Age 65+ LifePlans Inc., 2003 5 6 Impact of insurance on choice of setting Research Questions • Does insurance affect choice of setting of care ♦ ♦ • Higher income is associated in cross-section with greater use of residential care given disability, perhaps because of living arrangement and caregiver patterns by socioeconomic status • “Extra” resources contingent on disability could support earlier entry into residential care OR Could support care at home, other things (marital status, age, disability, living arrangement, caregivers) constant. at home vs. residential setting • For community residents, does insurance affect ♦ ♦ Use of paid care Use of unpaid care (informal care) • 7 8 Choice of Setting by Income for Elders with Disabilities—NLTCS 1999 Modeling Selection Effect for Holding LTC Insurance Income <$20K >$20K All Care at Home 36.6% 17.2% 30.1% Residential Care 63.4% 82.8% 69.9% • LTC insurance market is new; age will differ • Income: Medicaid programs, premium costs Î higher income for purchasers • Education • Marital status at time of purchase: more likely to be married 100.0% 100.0% 100.0% 9 • Race: marketing to whites? 10 Data Sources Unmeasured Effects • All insured persons claiming benefits from 8 private LTC insurance companies in 1999 ♦ Disabilities in 2+ ADLs • Purchasers have a higher self-assessed OR probability of needing LTC in next five years • Purchasers are more risk averse than ♦ Cognitive impairments • 1999 National Long-term Care Survey nonpurchasers comparison group – same functional level ♦ Disabilities in 2+ ADLs ♦ See Finkelstein and McGarry (2004) OR ♦ Cognitive impairments 11 12 Comparing the two groups Elders with disabilities: Insured elders differ from general population • Insured group with physical disability is ♦ Younger ♦ More likely to be married ♦ Higher education ♦ Higher income ♦ More likely to be white Age Married Male Education HS, Not College College Graduate Income $20K+ Proportion White 13 Proportion in nursing home 90% 65.2% *** *** *** *** Sample: restrict to nonpoor (couples or singles) Insured status ♦ Insurance as the endogenous variable of interest 60% ♦ Education and never married as instruments: affect insured 50% state • 40% Setting of care ♦ Insurance 62.0% 30% ♦ Level of disability 34.8% ♦ Income 10% Nursing Home Receiving Care at Home 0% Not Insured with Disability Insured with Disability 15 16 Bivariate Probit Results (2) Bivariate Probit Results Estimates for Setting of Care: Community = 1 Variable Coefficient se t Pr > |t| Intercept 3.023 0.621 4.87 <.0001 Insured 1.427 0.220 6.49 <.0001 Married 0.212 0.129 1.64 0.1008 Never married -0.394 0.270 -1.46 0.1443 Male -0.205 0.116 -1.77 0.0761 Log of Income (000) -0.113 0.074 -1.53 0.1249 White -1.819 0.190 -9.56 <.0001 Age:Years 65-59 0.115 0.114 1.01 0.3112 Age: Years 70-79 -0.036 0.022 -1.65 0.0996 Age: Years 80+ -0.032 0.013 -2.42 0.0156 Disabled in 1 ADL -1.331 0.344 -3.87 0.0001 - 2 ADLs -1.203 0.313 -3.84 0.0001 - 3 ADLs -1.426 0.308 -4.64 <.0001 - 4 ADLs -1.685 0.304 -5.54 <.0001 - 5 ADLs -1.793 0.295 -6.07 <.0001 - 6 ADLs -2.187 0.302 -7.24 <.0001 Cognitive impairment -0.647 0.118 -5.49 <.0001 Estimates for Insured Status Insured = 1 Variable Coefficient se t Pr > |t| Intercept -2.287 0.542 -4.22 <.0001 Never married -0.659 0.253 -2.60 0.0092 HS graduate 0.558 0.132 4.23 <.0001 Technical school 1.682 0.235 7.17 <.0001 Some college 1.213 0.158 7.68 <.0001 College graduate 1.470 0.168 8.77 <.0001 Graduate school 2.167 0.261 8.30 <.0001 White 1.443 0.215 6.70 <.0001 Age:Years 65-59 0.227 0.116 1.96 0.0497 Age: Years 70-79 -0.052 0.022 -2.35 0.0185 Age: Years 80+ -0.096 0.012 -8.14 <.0001 17 0.531 0.349 0.715 0.974 Bivariate Probit for Insured State and Setting of Care • • 38.0% 80% 20% 0.350 0.074 0.327 0.898 14 100% 70% Not Insured w Insured 85.723 79.843 *** 0.142 0.487 *** 0.216 0.346 *** 18 Marginal Effects on Probability of Community Residence Variable Insured Married Never married Male Log of Income (000) White Age:Years 65-59 Age: Years 70-79 Age: Years 80+ Disabled in 1 ADL - 2 ADLs - 3 ADLs - 4 ADLs - 5 ADLs - 6 ADLs Cognitive impairment Mean Marginal Effect for Sample 0.390 0.058 -0.108 -0.056 -0.031 -0.497 0.032 -0.010 -0.009 -0.364 -0.329 -0.390 -0.460 -0.490 -0.598 -0.177 19 Insurance is Associated with Higher Probability of Care at Home • Care at home is not associated with higher • • 20 For Community Residents: Effect of Insurance on Paid Care and/or Unpaid Care? • Conditional on community residence: selection effect ♦ Because insurance affects who remains at home, we are observing a different group than would occur otherwise • Should be modeled as simultaneous with choice of setting (choose based on care available) • Paid and unpaid care: substitutes or complements? • Zeros 21 Bivariate Probit for Joint Distribution of ANY Paid and ANY Unpaid Help Any Paid Care = 1 Any Unpaid Care = 1 Variable Coefficient Sig t Coefficient Sig t Intercept -1.398 0.298 -0.748 ns Insurance 2.659 <.0001 0.090 ns Log of income (000) 0.166 ns -0.092 ns Male 0.284 0.260 0.168 ns Years 65 to 69 0.079 ns 0.087 ns Years 70 to 79 -0.066 0.131 -0.004 ns Years Over 80 0.010 ns 0.055 0.019 3 ADLs 0.415 0.202 0.508 0.035 4 ADLs 0.159 ns 0.726 0.002 5 ADLs 0.917 0.002 0.595 0.004 6 ADLs 1.098 0.001 0.430 0.107 Cognitive Impairment -0.425 0.059 0.547 0.002 Child within 25 miles 0.088 ns 0.497 0.001 Married -0.554 0.044 0.893 <.0001 Rho 0.108 ns 22 If assume unpaid hours given -Variable Intercept Insured Log of Income (000) Male Age:Years 65-59 Age: Years 70-79 Age: Years 80+ - 3 ADLs - 4 ADLs - 5 ADLs - 6 ADLs Cognitive impairment Child within 25 mi Married Informal Care Hours 23 income -- does not appear to be a “superior good” But perhaps additional resources contingent on disability are used differently from ordinary income? Or people preferring care at home are more likely to purchase insurance? Hours of Paid Care Coefficient Sig t -37.087 0.0328 56.282 <.0001 3.405 0.1739 2.115 ns 2.355 ns -0.946 0.1129 -0.300 ns 12.113 0.0191 19.405 <.0001 25.537 <.0001 46.469 <.0001 -3.863 0.2509 -5.146 0.1052 -18.489 <.0001 -0.211 <.0001 Tobit Analysis Paid and Informal Hours Variable Intercept Insured Log of Income (000) Male Age:Years 65-59 Age: Years 70-79 Age: Years 80+ - 3 ADLs - 4 ADLs - 5 ADLs - 6 ADLs Cognitive impairment Child within 25 mi Married 24 Hours of Paid Care Hours of Informal Care Coefficient Sig t Coefficient Sig t -40.750 0.025 -27.074 0.185 59.843 <.0001 -11.338 0.022 3.982 0.124 -3.248 0.296 1.096 ns 5.980 0.162 2.045 ns 4.737 0.241 -0.856 0.166 -0.090 ns -0.492 ns 0.999 0.071 10.046 0.059 21.834 0.000 15.996 0.001 27.174 <.0001 21.361 <.0001 29.646 <.0001 41.828 <.0001 32.861 <.0001 -5.375 0.121 12.469 0.002 -6.485 0.047 10.448 0.006 -23.536 <.0001 30.554 <.0001 Insurance has a strong effect on paid care for community-resident elders • Bivariate probit shows large significant effect • on any paid (of course) Estimate given paid hours are nonzero implies 56 hours a week more for insured; paid hours are reduced by about 12 minutes for every hour of informal care Insurance affects informal care through effect on amount of paid care • • • No significant effect on the probability of any informal care Tobit shows reduction of about 11 hours for insured (Of course) insured must be buying more care for themselves than they would with an equal income increase – (about an hour a week for a $10000 income increase) • Tobit shows large effect – 60 hours 25 26 Compute Inverse Mills Analog Based on Bivariate Probit Results λcommres ⎡ ⎤ Yγ − ρXβ ⎥ ⎢ φ ( Xβ ) Φ 1 ⎢ ⎥ 2 2 ⎢ (1 − ρ ) ⎦⎥ ⎣ = F ( Xβ , Yγ , ρ ) Paid Hours (2SLS) Variable Intercept Insurance Hours of Unpaid Help ln Income (est) Number ADL Disabilities Cognitive Impairment R-squared =.2439 N=414 27 28 Unpaid Hours (2SLS) Variable Intercept Hours of Paid Help Child within 25 miles Married Number ADL Disabilities Cognitive Impairment R-squared =.25684 N=414 29 Parameter Standard Estimate Error 1.326 -0.451 3.089 15.510 8.285 7.627 4.272 0.114 2.926 3.171 1.027 3.156 t Value Pr > |t| 0.31 0.7564 -3.96 <.0001 1.06 0.2917 4.89 <.0001 8.07 <.0001 2.42 0.0161 Parameter Standard Estimate Error -5.263 20.717 -0.702 1.401 8.779 4.695 7.465 3.866 0.138 2.279 1.312 3.227 t Value Pr > |t| -0.71 0.4812 5.36 <.0001 -5.09 <.0001 0.61 0.539 6.69 <.0001 1.45 0.1465