MA WITH HETEROGENOUS INCOME

advertisement

DEWEY,

MIT LIBRARIES

3 9080 02874 5179

Massachusetts Institute of Technology

Department of Economics

Working Paper Series

CAPITOL INCOME TAXES WITH

HETEROGENOUS DISCOUNT RATES

Peter A.

Diamond

Johannes Spinnewijn

Working Paper 09-22

July 14,2009

RoomE52-251

50 Memorial Drive

Cambridge,

This

MA 02142

paper can be downloaded without charge from the

Paper Collection at

Social Science Research Network

http://ssm.com/abstract=1434182

Capital Income Taxes with Heterogeneous Discount Rates^

Peter Diamond*

Johannes Spinnewijn*

MIT

MIT

July 14, 2009

Abstract

With heterogeneity

in

Stiglitz result that savings

both

skills

and preferences

for the future,

the Atkinson-

should not be taxed with optimal taxation of earnings does

not hold. Empirical evidence shows that on average people with higher

higher rates.

skills

save at

Saez (2002) suggests that with such positive correlation taxing savings

can increase welfare. This paper analyzes this issue in a model with

correlation between ability

and preference

the same earnings

number

to the analysis

is

level,

the

that types

switch to a lower earning job.

who

for the future.

of types of jobs in the

less

than perfect

To have multiple types

economy

is

restricted.

at

Key

value future consumption less are more tempted to

We show that introducing both a small savings tax on

the

high earners and a small savings subsidy on the low earners increase welfare, regardless

of the correlation between ability

and preferences

However, a uniform

for the future.

savings tax, as in the Nordic dual income tax, increases welfare only

is

sufficiently high.

results

*We

There are also some

results

if

that correlation

on optimal taxes that

parallel the

on introducing small taxes.

Keywords: Optimal

Taxation, Capital Income, Discount Rates

JEL

Number: H21

Classification

Emmanuel

Werning and seminar parand the NBER for

valuable comments, and the National Science Foundation for financial support (Award 0648741). The research reported herein was supported by the Center for Retirement Research at Boston College pursuant to

are grateful to Jesse Edgerton, Louis Kaplow,

ticipants at

MIT,

Saez, Ivan

Berkeley, Stockholm University, the Stockholm School of Economics

a grant from the U.S. Social Security Administration funded as part of the Retirement Research Consortium.

The findings and conclusions are solely those of the authors and should not be construed as representing the

opinions or policy of the Social Security Administration or any agency of the Federal Government; or the

Center

for

Retirement Research at Boston College.

of Economics, E52-344, 50 Memorial Drive, Cambridge,

department

'Department

of

Economics, E51-090, 50 Memorial Drive, Cambridge,

MA

MA

02142, pdiamond@mit.edu.

02142, jspinnew@mit.edu.

Digitized by the Internet Archive

in

2011 with funding from

Boston Library Consortium

Member

Libraries

http://www.archive.org/details/capitalincometaxOOdiam

Introduction

1

The

Atkinson-Stiglitz (1976) theorem shows that

linear earnings taxes, optimal taxation

assumptions are

tween consumption and labor and

the available tax tools include non-

inconsistent with taxing savings

when two key

consumers have preferences that are separable be-

(1) that all

satisfied:

is

when

(2) that all

consumers have the same sub-utility function

of consumption. Empirical evidence suggests that on average those with higher

(Dynan, Skinner and Zeldes, 2004, Banks and Diamond, 2008).

at higher rates

relax the second condition

skill

skills

We

therefore

and analyze the taxation of savings with heterogeneity

We

and savings propensity.

save

both

in

consider both uniform and earnings-varying taxation of

savings.

This paper uses a simple model

restricted.

This sheds

light

on the

role of the positive correlation

argument

we

skill

and the

is

be taxed, whereas the savings of the low

independent of the correlation between ability

optimum has

factors, provided that the

A

is

of savings progressive in earnings. In a two-skills model,

earners should be subsidized. This result

productive job.

economy

and savings propensity. The paper provides an

find that the savings of the high earners should

and discount

in the

desirability of earnings-dependent savings taxes

between

making the taxation

for

which the number of types of jobs

in

the high skilled workers on the more

uniform savings tax, however, only increases welfare

if

that correlation

is

sufficiently high.

Our paper

builds

on the analysis

Saez (2002). He derives conditions on endogenous

in

variables to sign the effect on social welfare of introducing a uniform

subsidy,

when consumers have heterogeneous

an optimal non-linear earnings

net marginal social value

is

restricted to the

same

on savings increases welfare

if

or a

With

sub-utility functions of consumption.

tax, a small tax

either the

negatively correlated with savings, conditional on earnings, or

on average those who choose to earn

if

commodity tax

earnings.

less

By

save less than those

restricting the

the importance of the (exogenous) correlation between

number

skills

who choose

to earn more,

of types of jobs,

we analyze

and savings preferences

for the

taxation of savings.

Primary attention

and two

skill levels.

screening problem.

is

focused on a model with four worker types

Thus we

The model assumes

model where each worker can

setting

are examining a particular

with two discount factors

example of a multidimensional

the existence of two jobs, rather than the standard

select the

where workers with the same

-

skill

number

of hours to be worked.

1

This results in a

but different discount factors choose the same job

and so have the same earnings. With the introduction of earnings-related savings tax

:

A

limited

number

of jobs

was assumed

in

Diamond

(2006).

rates,

We

they are subject to the same tax rates.

assume that

optimum both

at the

high-skill

types work at the high-skill job and that redistribution from high earners to low earners

is

Given these assumptions

the important redistribution.

social welfare increases

with the

introduction of a tax on the savings of high earners and with the introduction of a subsidy

on the savings of low earners. The

relative frequencies of the four types in the population

plays no role in the derivation of this result, conditional on the assumed structure of the

optimum.

The underlying assumption

is

that those valuing the future

work than those valuing the future

less,

more are more

conditional on the disutility of work. This

that an incentive compatibility (IC) constraint just binding on a high

value for the future

not binding on a high

is

willing to

skill

worker with low

skill

worker with high value

Earnings-dependent taxes and subsidies on savings allow an increase

for the future.

tempted to switch

jobs.

all

are

high earners) eases the binding IC constraint

transfers resources from the high saver to the low saver for

it

who

In particular, introducing taxation of savings of high earners

(and transferring the revenue back equally to

since

by

in redistribution

targeting types in a given job with saving preferences different than those of types

just

means

whom

the IC constraint

binding. Introducing a subsidy on savings for low earners (financed by equal taxation on

low earners) also eases the binding IC constraint by making switching to the lower job

is

all

less

attractive to the high earner with low savings. In extensions, the case for taxing the savings

of high earners appears to be

earners.

more robust than the case

While the focus of the paper

is

for subsidizing the savings of

the introduction of small taxes,

we

low

also consider

optimal taxes under stronger assumptions. 2

The assumption

is

in line

that those with less discounting of the future are

with standard modeling, representing preferences by u (x)

alternative specification j-u (x)

types with higher 5

+

u

(c)

—

v (~/n

;

)

prefer to save more, but to

l

+

more

S,u (c)

willing to

—

v

work

would imply the exact opposite. That

work

less.

We

on education and

is,

examine some empirical

support for our assumption, using data from the Survey of Consumer Finances (SCF).

find that conditional

An

(z/rii).

We

age, people with higher discount factors tend to earn

more. To proxy for the discount factor, we use reported savings and the time horizon people

report having in

mind when making spending and savings

to revisit the positive correlation

between

skills

decision.

We also use these proxies

and savings propensities.

This paper contributes to the literature on the optimal choice of the tax base and the

joint taxation of labor

and capital incomes

in particular.

Banks and Diamond (2008) review

the literature on the inclusion of capital income in the tax base.

The

analysis assumes rational savings by

relevant for retirement savings policies.

all

Gordon (2004) and Gordon

workers. Concern about too

little

individual savings

is

also

and Kopczuk (2008) argue that capital income reveals information about earnings

thus should be included in the tax base.

people with different

an income

tax,

skills

may be

and

ability

and

Blomquist and Christiansen (2008) analyze how

different preferences for leisure

separated with a commodity tax.

who cannot be

The

separated with

four-types model with hours

chosen by workers has been studied by Tenhunen and Tuomala (2008), which calculates a set

of examples, but explores the analytics only in two- and three-type models.

We

both welfarist and paternalist objective functions.

We

examples to some of our results below.

in a two-types

They

consider

relate the results in their calculated

focus on the four-types model since the result

model, while striking, does not seem relevant for policy inferences. 3 While

the focus of this paper

is

on capital taxation, the intuition generalizes to the taxation of

other commodities for which the preferences are heterogeneous, since this heterogeneity

may

impact the labor choice as well (Kaplow, 2008a).

The paper

two

jobs.

is

Section 2 sets up the model with four types and

organized as follows.

Section 3 characterizes respectively the

referring to

best and the restricted

first

no taxation of savings and an 'equal job, equal pay'

restriction.

first

best,

Section 4

introduces incentive compatibility constraints and characterizes the second best including

Optimal savings tax rates are

the introduction of earnings-varying savings tax rates.

considered.

also

Section 5 considers a uniform savings tax, rather than one varying with the

level of earnings.

For comparison, Section 6 reviews a two-types model. Section 7 discusses

empirical support for the assumptions and Section 8 has concluding remarks.

Model

2

We

consider a model with two periods. Agents consume in both periods, but work only in

the

first

period. Preferences are

and work. Denoting

earnings by

z,

first

assumed to be separable over time and between consumption

period consumption by x, second period consumption by

> 0,u" <

u'

producing output

factor

We

and

preferences satisfy

U(x,

with

c,

and

z.

An

v'

>

c,

z)

0,v"

=

>

u (x)

0.

+

An

5u

(c)

—

v (z/n)

agent's ability

,

n determines the

disutility of

agent's preference for future consumption depends on the discount

5.

consider heterogeneity in both ability n and preference for future consumption

5.

''Kocherlakota (2005) provides an argument for regressive earnings-varying wealth taxation. He analyzes

skills, which is not present in this model.

a model with asymmetric information about stochastically evolving

Although robust insights

for

optimal taxation have been derived in models with two types,

considering heterogeneity in two parameters in a model with two types implies perfect cor-

between the two parameters. The inference based on a simple two-types economy,

relation

although simple,

we consider a

fij

may

therefore be misleading.

and welfare- weights

factors 6

and

1

We

four-types model.

and

with Sh

Sh,

The

rj^.

>

Si.

In order to allow for imperfect correlation,

denote the four types by ll,lh,hl,hh with frequencies

first

two types have low

ability ni, but differ in discount

The second two types have high

also differ in discount factors

Si

and

rih

factor

hh

hi

lh

11

low ability ni

in

the economy, h and

The

/.

The output from a job

high-ability types can hold either job.

redistribution to the low-skilled types

balanced that

all

is

>

n-i,

Si

of the worker's type, while the disutility of holding a job varies with ability.

types can only hold the low job.

n/,

low discount

factor Sh

There are only two jobs

,

Sh.

high discount

high ability

n h with

ability

sufficiently

is

independent

The

We

low-ability

assume that

important and the type mix sufficiently

high-skilled workers hold high-skilled jobs at the various

optima analyzed.

This requires a restriction on the weights in the social welfare functions and the population

distribution,

We

which we do not explore.

begin with the

produced on a job

The

first

is

first best,

the

same

which

for

differs

everyone holding the job.

best has the property that there

consider a restricted first best (the term

constraints, the

term

'restricted'

from the usual treatment

'first

is

We

in that the

assume a

output

linear technology.

no marginal taxation of savings.

Then we

best' refers to a lack of incentive compatibility

means limited tax

tools,

but not limited by IC constraints)

with zero taxation of savings and the requirement that everyone holding a job receives the

same pay (no taxes based on

social welfare

We

identity, only

on potential earnings).

We

calculate whether

can be improved by taxing or subsidizing savings.

then turn to the second best, with taxes based on earnings, not potential earnings,

so that there

is

an incentive compatibility constraint.

restriction, thus preserving the condition of equal

potential gains from taxing or subsidizing savings.

pay

We

assume a zero taxation of savings

for equal

work. Again

we ask about

—

First Best

3

In the

is

first

worker

best, each

is

assigned to the matching job and the social welfare function

maximized with respect to the

consumption

type-specific

With the

periods and the job-specific output levels, subject to a resource constraint.

weight of type

of

ij

i]

,

t

the

first

and second

levels in the first

welfare

best solves:

£ /y^j (u

Maximize I|C ,,

+

[xtj]

6jU

-

[cy]

v

{z l /n,})

(1)

subject

E+

to:

^2

fij

i

x ij

+#

Forming a Lagrangian with A the Lagrange multiplier

£ = Yl

f*rt*i

u

(

^+

~

Si u fad

v

\

Zl l

_1

type

ij

~~

<

z%)

the resource constraint,

for

n^ ~ A

5Z fa

(

Xii

+R

' lc

H ~

we have

z i)

i,j

hi

We

cy

define the net marginal social value of

first

period consumption for an individual of

[xij]

-

as

9ij

Along the relevant portion of the

gij

=

+

VtjU

A.

social welfare optima,

and u

v'

ifulu

=

[zi/nA

L

fihVih)

[x^]

=

=

(/«

5jRu'

+

fih)

[cy]

A

=

we have the

for all i,j,

fuVuu'

and

+

[xu]

following properties:

fihVih.u' [x ih ]

,

rii

for

both the high-skilled and the low-skilled jobs. The net marginal social value of first period

consumption

for

each type equals

the required output for a given job

and the saving of each type

is

is

undistorted. Given that

independent of an individual's type, the earnings are

marginally distorted upward for one discount- factor type and downward for the other type,

since v! [xu]

^

u' [x^], unless

the welfare weights satisfy

T]

d

=

>] lh

.

The output

is

undistorted

'on average' though.

3.1

Equal Pay

Restricted First Best:

for

Equal Work and

No

Taxation of Savings

If

the (after-tax) earnings on a job, y

; ,

is

restricted to be type- independent

and savings can

not be taxed, there are further constraints, which we approach using the indirect

utility-of-

consumption function,

This function

R\.

iuj [y,

u>j

[j/j

=

R]

subject

satisfies

max u

x

to:

[x]

+ R~

1

c

+

5jU

—

y.

[c]

For later use, we note that

dwj

u

\x]

dy

j£

where

Sj [y,

We

all

R]

is

= R- 2 cu'[x} = R- (y-x)u'[x} = R-h J

1

iy,R}u'[x}

the savings function of someone with discount factor

5j.

continue to assume that the welfare weights and population fractions are such that

high skilled are on the more productive job at the optimum.

The

restricted first best

solves the following problem,

Maximize^

]T fljrjij ( Wj

R]

[y n

-

v [zjn,])

(2)

subject

E+

to:

J2

fij (Vi

~

zi)

<

Forming a Lagrangian, we have

hi

hi

The

first

order conditions

(FOC)

are

5Z fctfijU' [Xij] =

A^/y

3

Yl fitful

3

\

zil ni\ l n

i

=

A

3

for

i

—

h,

I.

5Z^'

3

Recalling the definition of the net marginal social

utility,

g tJ

=

rj^u' [xij]

—

A,

the population-weighted values add to zero at each job,

}] fij9ij =

for

i

=

h,l.

3

Thus, the welfare weights determine the direction of desired redistribution (given the equal

pay condition) between workers on each job. Also,

vl [xij]

The

FOC

for

job outputs,

z,,

are the

=

5jRu'

same

absence of savings taxation,

in the

for all i,j.

[cij]

as given above.

Restricted First Best with Small Earnings-Dependent Savings

3.2

Taxes

Given the observability of earnings, small

linear taxes

on savings (collected

in the first period)

could be set differently for high and low earners. This can for instance be implemented by

IRA and

the rules on retirement savings accounts, like the

desire to redistribute can be

met by a small

401 (k) in the US.

them by

(local)

on savings by workers on

linear tax or subsidy

a given job with the revenues returned equally to

The

raising net-of-tax earnings

on the

job.

Differentiating the Lagrangian with respect to a savings tax rate r,

level

i/i,

evaluated at a zero tax

=

A

(

d7~

The impact

H

of a savings tax

level:

fa

(tt

?/i,

the derivative can be written

=

-fr

~ xv)

H fvW'

)

on the Lagrangian

revenue constraint and the impact on

by

on those with earnings

11 fa

utilities.

is

made up

Using the

\

x ij\

of

FOC

(Vi

two

~ x u)

•

pieces: the

with respect to

impact on the

j/j,

multiplied

as:

(%'"'

(^

~

A ) X 'J

=

11 fa9U x H-

3

3

Recall that

Hfij9ij

=

for

i

=

h J-

3

This implies that a tax on the savings by the two types on a given job increases welfare

the savings of the one type towards which redistribution

compared

The

is

desirable saves sufficiently

if

little

to the other type.

welfare weights imply the desired direction of redistribution within productivity

types and so the signs of g }J

With equal incomes and

.

>

Cih

Thus,

if first

period

utilities get

Cu

the same weights for both types, n il

implying a desire to redistribute to the high saver. In contrast,

the

same weights

for

both types,

redistribute to the low saver.

we have

rj

hh u' [xhh]

= Vm u

given discount factors,

i]

'

ht

\

If

x m}

=

r)

we have

different discount factors,

if

=

r)

lh

,

<

gu

second period

<

g,h,

utilities get

u Si

=

n lh 5h, the signs are reversed, implying a desire to

there

is

no desire to redistribute

for high (low) skill types

m general,

with uniform weights for

i]

{Vih u

'

l

—

x ih}

Va u> x u})\

u we do not satisfy both conditions.

,

Second Best

4

We

draw a distinction between

restricted first-best analyses

and second-best ones based on

the absence or presence of IC constraints involving taking a job with lower productivity

(the reverse having been ruled out by assumption).

observability of productivity.

IC constraints are binding.

The prime

We

is,

the distinction depends on the

issue in second-best analyses

is

determining which

start with the further restriction, as above, that savings not

be taxed. With no taxation of savings and equal pay

imitating the other discount rate type

if

That

who

is

for

equal work, the IC constraint of not

holding the same job does not bind. Similarly,

a high productivity worker were to take the low productivity job, the person imitated

would be the one with the same discount

need not be such a worker

for

a high

skill

factor.

Imitation

is

a misnomer here since there

worker to optimize savings while taking a low

skill

job given the assumed policy tools and information.

We add the critical

assumption that earnings distribution issues are

that at the second-best

period consumption g tJ

optimum

=

sufficiently

important

(with IC constraints) the net marginal social value of

r/^u' [x l j]

— A

is

first

negative for both of the worker types holding

the high-skill job and positive for both of the types holding the low-skilled job. Without a

binding IC constraint, this condition could not hold at the optimum as noted above.

Assumption

1

The net marginal

9hj

social values of first period

<

®,9ij

>

0,

for j -h,l.

consumption

satisfy

We

No

Second best with

4.1

Taxation of Savings

assume that the Pareto-weights and population fractions are such that

workers work at the high-skilled job and the desired

is

sufficient that at least

one IC constraint

Maximize,,,,

subject

J2 f^q^

E+

to:

Wh

wi

Forming a Lagrangian with

and assuming that

C =

Y fan

(

WJ

at the

t

y"

-

v

R]

~

v

[yh,

-v

R]

~ ~0 <

fij {Vi

[yh,R]

°

]

(

wh

/n h > W[

[z h

\

[yh

R]

R]

[yu

-v

-

3)

[zi/n h ]

v [zi/n h

]

.

the Lagrange multiplier for the corresponding IC constraint,

fj,j

v

l

]

[zjn,])

/n h >

[z h

optimum each worker

R ~

level of redistribution to lower earners

binding.

is

(vjj [yi}

J2

high-skilled

all

Zi /

n^ - A

Y

i,j

assigned to the matching job,

is

fa ( y

>

we have

~ *)

hi

+ 22 ^j wj

(

[

y/"

R ~

_ w

i

v z >J n h\

]

[

\y<->

R +

]

v z i/ n h])

[

3

Since the first-period consumption of type hj

period consumption of type

the

Ij,

Y fWhj u

Y

'

[

FOC

switching to the low job equals the

if

with respect to earnings are

YW

-Y

x hj] +

[xhj]

~

X

j

;

hsiij 11 '

[

x ij]

Y Ai

=

°'

=

°-

j

vj u> x u\

[

- x Yf<j

3

Given the definition of the net

Y^

Y

i)

y ii'

—

[x,j]

Y^ ^ <

Y M>

= -

9ho

u>

A, this implies

°>

3

3

=

fato

3

The population-weighted

=

social utility g,j

^'"'

°-

3

values add to a positive expression

Y

i,j

f'J 9 'J

=

Y

Pi ("' Xl i\

l

3

LO

&

~ u Xh

'

\-

>

°'

first-

That

is,

transfers which

would be worth doing without an IC constraint are

restricted, raising

the social marginal utilities of consumption, on average, above the value of resources in the

hands of the government. Since the IC constraints are on the high

more

redistribution from the high earners to the low earners

IC constraints

straints

is

Given the equal pay constraint,

binding, and

it is

it

is

skilled types,

on average

desirable.

follows that only one of the

the one on the low discount factor type.

To

IC con-

see this consider

the difference in consumption utility from different incomes,

A [yh,Vu £j. R] = w

This difference in consumption

utility is increasing in

dA[yh ,yi,Sj,R]

u

35

The

difference in labor disutility does not

constraint

is

[c kj ]

-

The low discount

more tempted

[yi,

R]

the discount factor,

u

[cij]

>

0.

depend on the discount

binding on the low discount factor type,

factor type.

therefore

- w3

R]

[Vh,

j

it is

factor.

Thus

if

the IC

not binding on the high discount

factor type values earnings in the first period less

and

is

to switch to the less productive job.

Second Best with Small Earnings-Dependent Taxes on Savings

4.2

As above, the

sign of the welfare impact of introducing a small linear savings tax or subsidy

depends on the welfare weights.

Given observability of earnings, the small linear tax on

savings could be different for high and low earners.

tax on savings (collected in the

first

=

is,

f

]P fhj

(y h

- x hj

-

)

J

^7 =

That

A

A

(

5Z

/« ( y

'

" x «)

)

n

on

utilities,

Y^ fhjVhj u>

" Yl fljlll J u

the impact on the Lagrangian

constraint, the impact

welfare impacts of introducing a

period) are obtained by differentiating the Lagrangian

(with savings taxation included and the tax rates

O^r

The

is

'

i

x hj]

M

made up

set at zero):

(Vh

- x hj) -

fa ~ x 'j)

+

W

Vi u '

1

r "l

[-

[x h i] (y h

(w

-

-

r »)

,

•

of three pieces: the impact on the revenue

and the impact on the binding IC constraint.

11

- xu )

The

FOC

for earnings are

53 fhJ9hj + V-iu'

=

[xhi\

0,

3

j

Multiplying these by the earnings level at the job,

dC

and substituting, we have

j/*,

= 53 fhjQhjXhj +

u x hl] x hl,

'

l-h

[

J

= 53 fa9U x U ~

E<9r

;

Substituting for n

t

u' [xu]

FOC

from the

^

we

for earnings,

— = fhh9hh (xhh -

t^

x "] x "'

t

find

>

Xhi)

and

=

KOTi

The

JihQih [xih

)

0.

signs follow from the assumption on the net social marginal utilities

in savings

behavior by types ih and

il

for

i

plays no role in signing these expressions.

Proposition

skill

- xu <

1

jobs and g^j

that falls

At the second

<

0,gij

on high earners

>

is

0,

best

for j

h,

is

I.

The

optimum, assuming that

=

differences

correlation between skill and discount

The Proposition immediately

all

h,l, then introduction of a

welfare improving;

savings that falls on low earners

One can

—

and the

high

follows.

skill

workers hold high

small linear tax on savings

and introduction of a small

linear subsidy

on

welfare improving.

increase the redistribution from high earners/high savers by taxing savings, but

increasing net-of-tax earnings just enough that the high earners/low savers remain indifferent

to job

change and thus the binding IC constraint

is

unchanged.

One can

also increase

the redistribution towards the low earners/high savers by subsidizing their savings, but

decreasing net-of-tax earnings such that the low earners/low savers remain indifferent so

that

it

does not become more attractive for the high earners/low savers to take the low job.

12

Second Best with Optimal Linear Earnings-Dependent Taxes

4.3

on Savings

We

have considered the introduction of small savings taxes on high and low earners. Part of

the interest in this analysis comes from the possible link to the signs of the optimal taxes.

FOC

Derivation of the

it

for the

optimal linear savings taxes

straightforward;

is

we show

that

matches the signs of the small improvements given the additional condition that workers

save more

One

first

if

4

the after-tax return to savings are higher.

difference in analysis

that changes in both the earnings and savings taxes have a

is

order effect on tax revenues through the behavioral change in savings. In

n

revenue from a linear savings tax

units, the tax

discount factor

5j

and earnings y equals T

l

denote optimal savings

dependence on the

Sj [y,,

R(l —

A

second difference

sv u

depends on the

level of the savings tax.

l^\° K

M F«J

i_ Ti

{

Forming a Lagrangian, and assuming that

at the

is

no

that the relative

is

marginal increase in the savings tax compared to the

of a marginal increase in earnings

dr

For notational convenience,

r,)].

by s^. (Given preference separability, there

r,)]

effort to achieve gross earnings.)

size of the utility loss of a

—

period

on the savings of workers with

levied

[yi,R(l

sd

x

first

That

utility gain

is,

i-ndVi'

optimum each worker

is

assigned to the

matching job, we now have

C =

Y

The

htfij

FOC

H

for

[W. (!

~

+

fi t

T i)

R \

v zil n i])

\

(wi [y h (1

-

,

rh )

-

x

Y

Ai

tt yi

~ z^ ~

R]-v [z h /n h - w

]

t

[y u (1

TiS v [W>

-

r

(

)

R)

i

l

-

T i)

R }}

+ v [zi/n h

])

.

earnings are

Y

Y

fhjVhj u ' x hj]

\

+

htfljU*' [Xij]

fru'

-

[xhi]

fliU

-

[Xu]

Y ^

X

-

Yl Mlj

"

2

(

(

1

Th

l

~FT

dy

=

)

°'

- Ti-

dy

'Consideration of earnings-dependent nonlinear savings taxation would raise the issue of the degree of

complexity that

is

interesting for policy purposes.

L3

FOC

The

Y

for savings

tax rates are

ftJ

IhjVhjU

+

[Xhj]

L

i

ftu' [xta]

Y

-r^

h

'h

•!•

J

X fhJ

s

{

^+

^

1

Th

=

o,

OTh

I

3

SU

Denote by

=

/?/,

respectively the high

= R(l — n)

R(l - r^) and Ri

and low

skill

find that the optimal linear savings tax

fhhQhh {Xhh

~ xm) =

rh

is

r^}

0.

the after-tax returns to savings for

Combining the

types.

+

first

order conditions as before,

we

such that

Y

X fhj

s hj

\

- -Q^Shi + ^y!r Rh

(

\

4)

and

fihQlh (xih

The

~

Xll)

=

T

iY X

f'J

Sl J

I

~

~d^

S"

+

TR

Rl

^

'

|

left-hand sides in equations (4) and (5) correspond to the welfare changes of introducing

earnings-dependent taxes on the high earners and low earners respectively. Thus,

of the terms in brackets

if

on the right-hand

the introduction of a small tax

additive, -^-

<

1,

and so

—

s tj

is

>

—

dRi

n

u

is

-p^-Su

>

is

for

i

=

and vice

h,l.

versa. Since preferences are

Hence, a sufficient condition

for

that savings are increasing in the after-tax return,

the second best

optimum, assuming that savings are increasing in the

after-tax returns, all high skill workers hold high skill jobs,

and g hj <

the optimal linear savings tax

and negative for

is

positive for the high earners

0,gij

>

for j

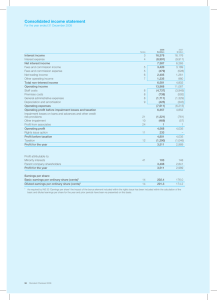

with hours chosen by workers.

CES

They

in their

Figure

derive the

1.

h,l,

(2008)

(2008) consider two-, three- and four-types models

mechanism design optimal

preferences with varying correlations between discount and

marginal taxes shown

—

the low earners.

Mechanism Design Optimum in Tenhunen and Tuomala

As noted above, Tenhunen and Tuomala

suming

sum

-

Proposition 2 At

4.4

the

positive, the optimal linear tax is positive

welfare- improving

the right-hand side term to be positive

^ii

side

if

For

allocations as-

skill,

with implicit

but very high correlation, they find that sav-

all

ings are implicitly marginally taxed for the high skill worker with low discount factor (type

3),

savings are implicitly subsidized for the low

2),

and there are no other marginal savings

skill

worker with high discount factor (type

distortions.

1

I

With very high

correlation, the low

05

——

i

t*

1

type

1

1

1

....... type 2

1

1

1

1

t

/

/

025

/

/

Wffffnm>tllM»t«»tltl»l«»tlHllllltM»JH»»l

1

i

/

•025

0

0:

5

correlation

FIGURE

1

Marginal tnx on savings

worker with low discount factor (type

skill

m

the welfarisf cnse

1) is implicitly

taxed, which also happens in the

two type model, which has perfect correlation. The potential relevance of the pattern we find

is

enhanced by

their findings.

mechanism design optimal

In contrast with our model, the

allocation allows distortion of the savings of each type separately.

is

not too high, on average the savings tax

low

skill

positive for the high skill

we

levels in

main

allow different ability levels for the two high earner types. Second,

all

four types.

Third,

High Earners

assume that the two types with high

high

skill

is

skill

allow different

the analysis extends to three

sufficiently

more

1

continues to hold.

skilled,

skill

if

skill

which IC constraint

is

\r>

As long

skill

as the

type with low

may be more tempted

required. For given skill of type hh,

binding holds

higher than h M (> n hh ), where the cut-off level n M

model above, we

the type with low discount

the type with high discount factor

is

skill.

than the high

However,

to switch to the low earner job for which less output

this reversal of

In the four-types

have exactly the same

type with high discount factor has higher

discount factor, Proposition

factor

we show how

we

propositions.

workers and jobs, preserving the various assumptions.

Different Ability Levels of the

,

for the

types.

discount factors for

is

and negative

consider three extensions to highlight the extent of robustness of the

First,

n hh

as the correlation

Robustness

4.5

We

is

As long

is

when

the ability level n M of type hi

such that the IC constraint

is

just

binding on both types,

{wi

[y h

,

R]

-

v {zh /h M )}

~

W'i

[Vi,

R]-v {zi/hhi)} =

{wh

With

is

[yh,

R]-v (zh /nhh )} - {w h

[y t

,

R]-v (zi/nhh )}

v [z/n] convex, the difference in labor disutilities between jobs, {v (zi/n)

n^

decreasing in n. Hence, for values of

for the

n«

higher than

the IC constraint

is

—

.

v (zh/n)},

more

stringent

high discount saver. In this case, a savings subsidy on the high earners and a savings

tax on the low earners are welfare improving. This

among

Different Discount Factors

the opposite of Proposition

is

the High and

earnings and no taxation of savings, a high

Low

With

Savers

1.

job-specific

worker considering switching to the low job

skill

chooses optimal savings without needing to match any particular worker holding the low

job. Thus, with the

is

same

skill

always higher for the high

the discount rates

among

among

skill

worker

the low

introducing taxation of savings

high earners, the gain from switching to the low job

skill

among

who

has lower preference for savings, regardless of

We

workers.

continue to have a welfare gain from

high earners as in Proposition

1.

Subsidization of savings of low earners will continue to generate a welfare gain as long

as the discount factor of the high-skill low-saver

of discount factors

among

holders of the low

consumption of the high-skilled low saver

on that job

if

small enough relative to the distribution

is

skill job.

Denoting by

taking the low

skill job,

x^i the first-period

the

FOC

for earnings

is:

3

The impact

of a savings tax on low earners

7^7

= Yl

is

f'j9ijXij

~

hu

'

[x'hi]

xM

.

3

Comparing the consumption

among low

in the

earners, this derivative

IC constraint with a weighted average of consumptions

is

savings of low earners in Proposition

negative (and the gain from the subsidization of the

1

_

continues to hold)

__

and only

if

xM >

xi,

where

Ej fij9ijXij

Yl j

With the

if

fijSij

net marginal social values assumption, gy

16

>

0, for j

—

h,

/, x~i is

a proper weighted

—

—

average of the Xy. Since the discount rates for the marginal high

high to meet this condition,

we

type

skill

may

well be too

consider the tax of the savings of higher earners to be a more

robust policy conclusion than the subsidization of the savings of low earners.

We

are exploring two extensions to the basic model, one with an education choice

and

one with a continuum of worker types. In both cases, preliminary work suggests the same

pattern of greater robustness of the taxation of higher earners than of the subsidization of

lower earners. 5

Three Ability Levels, Three Jobs

We extend

optimum

skilled

We introduce an intermediate skill level in the model.

the assumption that welfare weights and population fractions are such that at the

the high skilled are on the most productive job to also have

all

on the intermediate job.

We

all

the intermediate

again consider the case in which agents

may be tempted

Only two downward constraints are relevant

to switch to jobs designed for less skilled people.

though.

First, as above, for

constraint

two agents with the same

but different discount factors, the IC

skill,

slack for the type with the higher discount factor

is

with the lower discount factor. The reason

A

both

[2/1,2/2, 5j,

— —

dA[ym ,yi,6j,R]

— -

>

-

=

R]

- w3

Wj [yi,R]

and

binding for the type

that, with

is

=

if it is

—

[y 2

—

R]

,

d^{yh ,y

— ,8J- ,R]

do

l

,

.

>

-

for

i

—

m,

I.

ad

Second, with v [z/n] convex, we have a similar condition for the difference in the' disutility

of labor between jobs.

That

is,

A'

with

[z h

dA'[z h ,zi,n]

Thus,

for

,

zi,n]

= {-v

,

=

v

[z h

[z h /n\

two agents with the same discount

low-skilled job

is

/n]

zh

+

-

v [z,/n\

,

,

v [z[/n\ z

factor, the

L

)

2

jn <

0.

IC constraint of switching to the

slack for the type with the highest ability

if it is

satisfied for the

type with

the intermediate ability switching to the low-skilled job and for the type with highest ability

switching to the intermediate job.

That

is,

the local IC constraints imply the global IC

constraint.

In a similar

way

'With heterogeneity

in education.

If

as for the four-types model,

in

discount factors, people

we can

who discount the

only education determines a worker's

factors than low-skilled workers.

17

skill level,

set

up the Lagrangian

future less

may

for the

choose to invest more

high-skilled workers have higher discount

,

.

The two

constrained maximization problem.

Wi

wi

The impact

[y

R]-v [z h /n h

[y h

,

m

R]

,

-

v

[z

m /n m

relevant

]

> w

t

[y

}

> w

t

[y h

IC constraints are

m

,

-

R]

R]

-

m /nh

v

[z

v [zi/n m

]

]

of the introduction of earnings-dependent savings taxes on the Lagrangian equals

respectively

—

=

a

OT

h

fhh9hh {xhh

- xM >

)

0,

DC

JmhQmh \%mh

~7\

DC

=

77-

or

This implies that Proposition

The

-

xu )

<

<

^i

0.

1

continues to hold for the high earners and the low earners.

1

following Proposition applies for the intermediate earners.

Proposition 3 In a model with

redistribution

three ability levels

on savings that

linear tax (subsidy)

if

fihQih (xih

%ml)

from

(to) the

falls

and

three jobs, the introduction of a small

on the intermediate earners

is

welfare improving

intermediate earners to (from) general revenues

is

welfare

improving.

Proposition 3 implies that there

is

a single sign change

in the response of welfare to taxing

savings as a function of earnings. This result generalizes for more than three jobs as well,

the welfare weights are non-increasing in

The

skill.

if

savings of workers with earnings below

a given level are subsidized, the savings of workers with earning above that level are taxed.

The

result

depends on the assumption that types with the same

skill

are at the

same

job,

which becomes increasingly strained with many jobs.

The

single sign

change of the welfare impact of introducing a savings tax as a function of

earnings also holds for the optimal linear earnings-dependent savings taxes

[x]

=

optimal savings tax rate

is

CRRA preferences,

u

distributed across jobs, f }]

-t^-

=

0,

jz~i an d 7

fij

1-

With logarithmic

—

f3

for Vz, j.

fj

for \/i,j

and

~

xu)

first-period

workers

if

u

=

T,

i

=

log

[x],

the

s,j

=

-j^yi

and

satisfies

^ \fij-~Xu.

consumption x io

18

[x]

they are uniformly

Since for logarithmic preferences

the optimal tax on the savings of earners at job

—

preferences,

strictly increasing in the earnings of

fih9ih (Xih

With

<

when workers have

—

j^-yi,

we

find the following

,

,

expression for the optimal savings tax,

-

{Si

fh

A

S h ) (r\ ih

7"i

EiVi&;\»

Since

<$/,

>

5i,

with the welfare weights non-increasing

linear savings tax

is

+

l

5

in skill, this implies that the

optimal

increasing in earnings,

dTi

>0

7T

oyi

-

Second Best with Uniform Taxes on Savings

5

Proposition

1

what

leaves the natural question of

the tax rate on savings

oc

- = dc

a

Ot

dr h

oc

,

^r- =

for

both earnings

levels.

~

JhhQhh {Xhh

.

.

Xhl)

+

.

~

Jlh9lh {%ih

Xii)

Oti

In contrast with the earnings-varying tax

on savings, the correlation between

count factor plays a role here.

If

there

is

no desire to redistribute within a job,

r

hh9hh

r

Jih9ih

Jhh

=

y^

=

^

ST~^ r

y

,

Thj9hj

,

Y~^

>

Jlh

,

c

=

gu, for

— - vJhh

=

Jij9ij

##,

,

f' h

^

I

l-H

r

h,l,

r

then

-i

[x

fJ-iU

I

,

=

i

M

\

1

u F«J

•

Thus, the welfare impact of a change in the uniform tax on savings equals

It is

Adding the

we have

responses to the two separate tax changes,

"H

do with a Nordic dual income tax where

same

required to be the

is

to

9£

(

»T

\L,-/m

fhh

,

r

n

/

flh

N

A

n]/

Lj/y

/

convenient to write this as

9£

_

. „__„ w

flh

,

r

„

!

,

{x „

_

^J^^n

'

fhhTLjfh]

with

_

u'\x hl (x hl

]

U' [x a ] {Xu

19

- x hh

- Xih)

)

-

\

i

j

skill

and

dis-

Since Xu

>

xih,

S ,g n

_

(_j

{-jj^jrO ~

S , 9n

1

j

The

sign of this expression depends on the distribution of types and the ratio of the weights,

Q.

That

1h

>

12 j fhj

Q >

is,

y/"

Hj

,

1

is

a sufficient condition for a positive correlation between aspects,

to imply that introducing a savings tax increases social welfare.

1

,

flj

Assuming homothetic

u

Chl

\f

This expression

.

{

preferences, so that

y—

=

we

[x]

Thus,

the relative risk aversion 7

if

between

is

larger than

is

factor

smaller than

(i.e.

y/

hf

t

1,

>

if

7

is

Proposition 4

with

CRRA

greater than

is

no desire

// there is

-preferences,

A uniform

1

then

y/" ,

0,

>

1

and a

positive correlation

implies that |^

1

)

when

the correlation

to redistribute within a job,

positive.

is

one and the correlation between

ability

small subsidy on savings increases welfare

If there is

—

g,f,

gu, for

no desire

if the

if

and discount factor

the correlation between ability

As with the

some

tax returns to savings and by

the savings of type

and the after-tax

we

Sij

interest rate.

interesting cases.

CAR A

When

h,l,

relative

is

the relative risk aversion

g^ —

negative.

is

gu, for

1

=

h,l, with

if

and

positive (negative).

ij

Denote by

R T = R(l—r)

the after-

as a function of after-tax earnings

Setting the derivative of the Lagrangian with respect to r

- xM ) +

fihQih {xih

~

xu)

=

\J d

t }

U

''For

is

find the following condition for the optimal linear tax,

fhh9hh (xhh

negative.

7

earnings- varying taxes, the sign result for introducing a uniform tax matches

that for optimal linear taxation in

equal to zero,

is

—

and discount factor

and discount factor

within a job,

to redistribute

if

i

logarithmic preferences, a uniform small tax (subsidy) on savings increases welfare

only

If

negative, |^

is

a uniform small tax on savings increases welfare

greater than one and the correlation between ability

Corollary

prefer-

This implies the following proposition.

1.

risk aversion is smaller than

positive.

CRRA

For

the sign of |^ depends on the size of the correlation and the magnitude

1,

of the earnings difference between jobs. Conversely,

negative

becomes

f2

find

and discount

ability

the expression for

-,

equal to one for the log utility function.

is

ences, u

,

= £M

^M

preferences,

§y

the correlation

is

is

Xf

i:j

\

s^

(-/

O

ij

- ~-Su

+ w^-Rt

dyi

1

-i

dRT

negative when the correlation between ability and discount factor

dc

is positive if the absolute risk aversion is sufficiently sma

dr

positive,

^

20

is

If

sum

the

positive

of the terms in brackets

Proposition 5

If there is

logarithmic preferences or

is

we have

the introduction of a small uniform tax

if

logarithmic preferences and

savings

positive,

is

CRRA

welfare improving. This

within a job, g,h

to redistribute

preferences with 7

positive if the correlation between ability

<

1,

=

g,i,

for

the optimal linear

and discount factor

is

is

7 <

preferences with relative risk aversion

no desire

CRRA

is

that the optimal uniform tax

is

the case for

1.

i

=

h,l, with

uniform tax on

positive.

Two Types

6

Using a model with two types of workers, a high-skilled worker with high discount factor and

a low-skilled worker with low discount factor, the empirical finding of a positive correlation

between

skill

and savings rates

is

treated as a perfect correlation. In this model,

positive (negative) marginal earnings taxation then there

(negative) marginal savings taxation.

The

corollary

is

if

design

optimum has the same

property.

to realistic diversity in the economy.

The source

that introducing savings taxation

is

If

The

full

is

is

mechanism

seem robust

of this inference does not

With two-dimensional

earners with both high and low savings rates.

there

a gain from introducing positive

redistribution goes from the high earner to the low earner.

a gain

if

heterogeneity, there are low

a high earner can imitate the savings of a

low earner with the same savings propensities, a savings tax on the low earner does not work

to discourage the high earner from imitating.

Thus

to

model less-than-perfect

correlation,

we use the

four-types model with high and low earners with both high and low concern for

the future.

We

The proof parallels

model.

is

in

to as

Diamond

1

report the results for two types here to

and

(2003).

same

result for the

contrast with the four types

mechanism design optimum, which

consider the second-best Pareto frontier with the types referred

2.

Proposition 6 In

sign (nj

We

that of the

mark the

— n 2 ),

level is welfare

a two-types model without taxes on savings

the introduction of a small linear tax (subsidy)

improving

if

and only

if

and with sign{5\ —

on savings

=

at a given earnings

earnings at that level are marginally taxed (subsidized).

Corollary 2 In a two-types model without taxes on savings and with sign

the introduction of a savings tax

62)

on the lower earner

is

(5i

—

62)

=

sign (nj

welfare improving if redistribution

goes from the higher earner to the lower earner.

The

proposition combines the properties of the mechanism design optima in the two

separate two-types models with heterogeneity in one dimension.

21

When

both types have the

— n 2 ),

same discount

but different

factor,

are marginally taxed or subsidized

(Mirrlees, 1971).

the earnings of the potentially imitated type

abilities,

the ability of that type

if

when both types have the same

Similarly,

same discount

Stiglitz, 1976).

lower or higher respectively.

is

factor, distorting savings does not help separate the

Similarly,

both types have the same

if

marginal taxation.' However, when the two types

both the marginal taxation

subsidization) of savings

is

but different discount

ability,

type are marginally taxed or subsidized

factors, the savings of the potentially imitated

the discount factor for that type

lower or higher respectively

is

both

(or subsidization) of earnings

both types have the

If

two types (Atkinson and

earnings are not subject to

ability,

differ in

and discount

ability

factor,

and the marginal taxation

(or

used to separate types.

Preferences and IC Constraints

7

Above we used the

utility functions

u

[x]

+

8jU

[c]

—

v

[z/rij].

This family of

has the property that those with higher savings rates (larger values of

work

to increase

for

a given amount of additional pay.

But that

utility functions {u [x]

reversed

pay.

If

-

+

5jU

[c])

—

/5j

v

=

[z/rij]

u

[x]

/8j

+

u

—

[c]

utility functions

5j) are

more

not the only

is

which the savings and labor supply decisions can be connected.

is

if

willing

way

in

For example, with the

v

[z/rij],

the relationship

those with higher savings rates are less willing to increase work for additional

we had assumed

this class of functions, then

of desirable savings taxes in Proposition

saver would imply that

it

is

1

we would have reversed the pattern

having the IC constraint bind for the high

-

not binding for the low saver, implying, in turn, that there

should be a subsidy of savings for high earners and a tax on savings for low earners. More

generally, a one-dimensional family of separable utility functions,

any pattern between the variation

in the interaction

in the subutility function of

between consumption and labor. This

empirical basis for distinguishing which case

is

more

to write utility in the form employed does not, by

U

[x, c, j]

[<p

is

different. Generally,

(but not borrowing against

role for discounting

it).

So modeling

on both aspects

-

in

can have

consumption and the variation

raises the question of identifying

relevant.

itself,

That

it

shed light on

work precedes

pay,

is

its

While the formal model has consumption and work simultaneous

experience in real time

,z,j],

an

standard practice

empirical reality.

in the first period,

which precedes spending

it

continuous time would naturally have a similar

saving and willingness to work. But that does not rule

out the possibility that the preferences of high and low savers differ in other ways than just

'This can be considered an implication of the Atkinson-Stiglitz theorem, since there

everyone has the same subutility function over

tax

is

first

not allowed, the two types can be usefully separated by an earnings tax.

earnings of the potentially imitated type

is

is

separability

period earnings and consumption. Notice that

positive

if

and only

22

if

if

The marginal tax on

that type saves less for the

same

and

a savings

the

earnings.

a discount rate on otherwise identical

and

utility

There are reasons based on casual empiricism

for

disutility functions

(assuming additivity).

supporting the appropriateness of using the

Modeling savings with rationality and discounting combines

formulation employed above.

underlying preferences and issues of self-control. As discussed in Banks and

Diamond

(2008),

psychological analyses suggest these are mixed together.

We

does not apply to working as well as to consuming

whether that

is

working

for later

consumption or working to influence future work opportunities. That

is,

working

(at

with disutility) involves self-control

which would be captured

human

may

in the

a future payoff.

for

those with less difficulty in self-control

-

may show

standard

see

And

no reason to think that

this

a job

saving involves self-control. So

greater willingness to both work and save,

utility function expression.

capital investment involves discounting in a similar

way

In a richer model,

to savings decisions

and so

generate the pattern in the standard model structure, although formal modeling would

distinguish between

It

financial capital accumulations.

not easy to find data applying directly to this issue.

is

answer

human and

is

whether, for a given level of

A

greater labor supply functions.

in circumstances

The

we want

question

to

those with higher savings rates tend to have

skill,

complication in looking at data comes from the differences

with age, which we address by considering separate age

We

cells.

report a

few correlations supportive of a positive correlation among savings propensities, discounting

and earnings

abilities

using the Survey of

on time horizon and savings

Before turning to the data,

we have been

levels.

Education choices

rates,

which matter

for

both

them.

education

skill

A

and discount

model

also report

is

skill

some

is

correlations with

of the complications in interpreting the

also a complication in interpreting the

both ex ante

"skill"

Presumably, the

and discount

factor,

level of

and can not be used

affect

wage

completed education

is

on average. In addition to affecting ex

affect one's discount rate thereafter.

rate

data across education

and discount rate and then

in

Thus education

is

a proxy

a simple way to distinguish between

further difficulty in interpreting the correlations

variable while skill

is

that education

is

a discrete

continuous and varying within education classes.

Three-period Model

7.1

We

briefly consider a three-period version of the two-period

for later taxation.

may

some

effort.

reflect

increasing in both ex ante

skill,

We

considering. This will bring out

data at different ages. There

post

Consumer Finances, which includes some questions

work

practice.

we

8

set

up a three-period model with the same preference structure as the two-period model

analyzed, assuming the

same discounting

for the utility of

consumption and the

disutility of

For discussion of correlations with experimentally measured discount rates, see Chabris et

23

al,

2008.

,

work and allowing

for different skills in the

u

+

[xi]

8u

\x 2

]

+

5

2

u

two working periods.

[c]

-

-

v [zi/m]

5v

[z 2 /?i 2

]

Considering the special case with

u

we have the time

[x]

=

series of

log

and v

[x]

=

[z/n]

k (z/nf

+1

/

{(3

+

1)

consumption and earnings behavior, assuming that hours are

a control variable and the marginal tax rate

is

constant over time (with derivation in the

Appendix):

X2

=

—

= 5R

%2

--

(5R)-

~2

z 2 /n 2

--

1/0 (

1+1//3

n2

\

(5Ry 1/0

1/73

( n2

\

zi/n-i

Thus, those with higher discount factors have more rapidly growing consumption but

rapidly growing earnings (for given

earnings and work effort

The

may

skills).

This suggests that the cross section pattern of

be different at different ages.

cross-section pattern of time series behavior

may be more

illuminating than that of

single-period behavior since the single-period cross section patterns are dependent on the

pattern over time in

skills.

be concerned about income

If

we added uncertain

effects in

rates of return to the model,

we would

also

skills.

But

these issues, just reporting simple correlations.

Data Analysis

7.2

We

full

both consumption and earnings choices. Consideration

of wealth or wealth/earnings ratios are also affected by the time series pattern of

we do not explore

less

first

SCF

consider the relations

among

discounting, saving, education and age.

We

use the

panels in 1998, 2001 and 2004, containing information on 13,266 households in total.

For savings rates we consider two proxies.

worth to earnings

regularly or not.

9

for households.

The sample

is

The

first

proxy

The second proxy

is

is

the logarithm of the ratio of net

whether people report that they save

divided into age-education cells (5-year age groupings from

among different statements. We use for this second proxy whether subjects confirm

"Save regularly by putting money aside each month." The results are similar (with sign

''Subjects can choose

the statement:

reversal) with the statement "Don't save

-

usually spend about as

24

much

as income."