Boston College Financial Statements May 31, 2010 and 2009

Boston College

Financial Statements

May 31, 2010 and 2009

Boston College

Index

May 31, 2010 and 2009

Page(s)

Report of Independent Auditors ............................................................................................................... 1

Financial Statements

Statement of Financial Position.................................................................................................................... 2

Statement of Activities .................................................................................................................................. 3

Statement of Cash Flows ............................................................................................................................. 4

Notes to Financial Statements ............................................................................................................... 5–17

PricewaterhouseCoopers LLP

125 High Street

Boston, MA 02110-1707

Telephone (617) 530 5000

Facsimile (617) 530 5001 www.pwc.com

Report of Independent Auditors

To the Trustees of

Boston College

In our opinion, the accompanying statement of financial position and the related statements of activities and cash flows present fairly, in all material respects, the financial position of Boston College at May

31, 2010, and the changes in its net assets and its cash flows for the year then ended in conformity with accounting principles generally accepted in the United States of America. These financial statements are the responsibility of Boston College's management. Our responsibility is to express an opinion on these financial statements based on our audit. The prior year summarized comparative information has been derived from Boston College's 2009 financial statements, and in our report dated

September 14, 2009, we expressed an unqualified opinion on those financial statements. We conducted our audit of these statements in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

September 13, 2010

1

Boston College

Statement of Financial Position

As of May 31, 2010

(with summarized financial information as of May 31, 2009)

(in thousands of dollars)

Assets

Short-term investments

Accounts receivable, net (Note B)

Contributions receivable, net (Note C)

Notes and other receivables, net (Note B)

Investments (Note D)

Funds held by trustees (Note D)

Other assets

Property, plant and equipment, net (Note F)

Total assets

Liabilities

Accounts payable

Accrued liabilities

Deposits payable and deferred revenues

Bonds and mortgages payable (Note G)

U.S. Government loan advances

Total liabilities

Net Assets

Unrestricted (Note H)

Temporarily restricted (Note H)

Permanently restricted (Note H)

Total net assets

Total liabilities and net assets

2010 2009

$ 8,271

27,635

191,962

58,876

1,732,479

25,732

8,372

1,039,611

$ 3,092,938

$ 10,203

24,199

221,411

43,803

1,518,508

31,894

10,994

1,037,488

$ 2,898,500

$ 4,739

156,056

38,162

671,687

34,870

905,514

$ 5,390

126,780

42,202

679,436

34,461

888,269

1,165,688

336,926

684,810

2,187,424

$ 3,092,938

1,086,134

289,613

634,484

2,010,231

$ 2,898,500

The accompanying notes are an integral part of these financial statements.

2

Boston College

Statement of Activities

Year Ended May 31, 2010

(with summarized financial information for the year ended May 31, 2009)

(in thousands of dollars)

Unrestricted

Temporarily

Restricted

Permanently

Restricted

2010

Total

2009

Total

Operating

Revenues and other support

Tuition and fees before student aid

Auxiliary enterprises before student aid

Sponsored research and other programs

Government financial aid programs

Sales and services

Other revenues

Nonoperating assets utilized or released from

restrictions for operations

Total revenues and other support before student aid

Student aid applicable to tuition and fees

Student aid applicable to auxiliary enterprises

Net revenues

Expenses

Instruction

Academic support

Research

Student services

Public service

General administration

Auxiliary enterprises

Total expenses

Increase in net assets from operating activities

Nonoperating

Contributions

Realized and unrealized investment gains/(losses), net

Investment income, net

Other gains or (losses)

Debt extinguishment charges

Nonoperating assets utilized or released from restrictions

for operations

Net assets reclassified or released from restrictions

Increase/(decrease) in net assets from

nonoperating activities

Total increase/(decrease) in net assets

Net assets, beginning of year

Net assets, end of year

$ 474,257

136,806

55,549

5,269

4,465

9,998

68,266

754,610

(122,773)

(3,483)

628,354

233,914

54,523

36,162

44,728

2,433

112,549

143,938

628,247

107

5,903

86,484

4,650

(9,857)

(19,543)

11,810

79,447

79,554

1,086,134

$ 1,165,688

-

-

-

-

3,414

-

50,326

50,326

634,484

$ 684,810

-

-

-

-

$ 26,683

86,045

(192)

(1,276)

$ 44,281

4,912

54

(2,335)

(48,723)

(15,224)

47,313

47,313

289,613

$ 336,926

$ 474,257

136,806

55,549

5,269

4,465

9,998

68,266

754,610

(122,773)

(3,483)

628,354

233,914

54,523

36,162

44,728

2,433

112,549

143,938

628,247

107

76,867

177,441

4,512

(13,468)

-

(68,266)

-

177,086

177,193

2,010,231

$ 2,187,424

$ 455,096

145,232

50,297

5,046

4,835

9,669

67,331

737,506

(112,615)

(3,873)

621,018

226,601

54,294

33,986

43,745

2,241

111,657

148,392

620,916

102

150,817

(408,366)

4,871

1,593

(104)

(67,331)

-

(318,520)

(318,418)

2,328,649

$ 2,010,231

The accompanying notes are an integral part of these financial statements.

3

Boston College

Statement of Cash Flows

Year Ended May 31, 2010

(with summarized financial information for the year ended May 31, 2009)

(in thousands of dollars)

2010 2009

Cash flows from operating activities

Total increase/(decrease) in net assets

Adjustments to reconcile change in net assets to short-term

investments (used in) provided by operating activities

Depreciation, amortization and accretion

Net (gain) on retirement or disposal of fixed assets

Contributions of property and equipment

Loan cancellations

Contributed securities

Realized and unrealized investment (gains)/losses, net

Debt extinguishment charges

Change in assets and liabilities

Accounts receivable, net

Notes and other receivables

Contributions receivable, net

Accounts payable and accrued liabilities

Deposits payable and deferred revenue

Other assets

Contributions to be used for long-term investment

Net short-term investments (used in) provided by operating activities

Cash flows from investing activities

Proceeds from sales of investments

Purchases of investments

Student loans granted

Student loans collected

Purchases of property, plant and equipment

Change in funds held by trustees

Net short-term investments (used in) investing activities

Cash flows from financing activities

Net proceeds from issuance of debt and line of credit

Repayment of debt and line of credit

Payment of bonds and mortgages payable

Prepayment of debt

Change in U.S. Government loan advances

Contributions to be used for long-term investment

Net short-term investments provided by financing activities

Net change in short-term investments

Short-term investments, beginning of year

Short-term investments, end of year

Supplemental data

Interest paid

Asset retirement obligations recognized

Net fixed asset recognized related to asset retirement obligation

Contributed securities

$ 177,193 $ (318,418)

47,557

(3,703)

(1,093)

1,174

(7,849)

(177,441)

-

(3,436)

(14,479)

29,449

26,164

(4,040)

2,622

(77,272)

(5,154)

496,010

(524,691)

(4,005)

4,914

(45,871)

6,162

(67,481)

-

-

(6,978)

409

-

77,272

70,703

(1,932)

10,203

$ 8,271

132,053

(54,470)

(8,179)

(3,949)

245

42,030

107,730

1,164

9,039

$ 10,203

$ 31,209

184

381

7,849

46,413

(13,045)

(1,014)

1,057

(5,102)

408,366

104

1,809

-

(71,150)

4,081

(4,603)

72

(42,030)

6,540

623,839

(628,673)

(5,299)

4,341

(119,822)

12,508

(113,106)

$ 27,967

409

155

5,102

The accompanying notes are an integral part of these financial statements.

4

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

A. Accounting Policies

The significant accounting policies followed by Boston College (the "University") are set forth below and in other sections of these notes.

Basis of Presentation

The accompanying financial statements have been prepared on the accrual basis with net assets, revenues, expenses, gains, and losses classified into three categories based on the existence or absence of externally imposed restrictions. The net assets of the University are classified and defined as follows:

Unrestricted

Net assets that are not subject to donor-imposed stipulations. Unrestricted net assets may be designated for specific purposes by action of the Board of Trustees.

Temporarily Restricted

Net assets where use is limited by law or donor-imposed stipulations that will either expire with the passage of time or be fulfilled or removed by actions of the University.

Permanently Restricted

Reflects the historical value of contributions (and in certain circumstances investment returns from those contributions), subject to donor-imposed stipulations, which require the corpus to be invested in perpetuity to produce income for general or specific purposes.

Revenues are reported as increases in unrestricted net assets unless use of the related assets is limited by donor-imposed restrictions. Expenses are reported as decreases in unrestricted net assets. Realized and unrealized gains and losses on investments are reported as increases or decreases in unrestricted net assets unless their use is restricted by explicit donor stipulation or by law.

Nonoperating Activity

Nonoperating activity includes all contributions, investment income, gains and losses on investments, gains and losses on postretirement healthcare benefits, unfulfilled promises to give, gains on sale of property, debt extinguishment charges, and voluntary retirement incentive expenses. All other activity is classified as operating revenue or expense.

To the extent contributions, investment income, and gains are used for operations, they are reclassified as "nonoperating assets utilized or released from restrictions for operations."

Expirations of temporary restrictions on net assets or other clarifications from donors are presented as "net assets reclassified or released from restrictions.”

Contributions

Contributions, including unconditional promises to give, are recognized as unrestricted, temporarily restricted, or permanently restricted revenues in the year received. Contributions receivable are recorded at the present value of expected future cash flows, net of an allowance for estimated unfulfilled promises to give. Conditional promises to give are not recognized until the conditions on which they depend are substantially met. Contributions of noncash assets are recorded at fair market value.

5

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

Contributions and investment return with donor-imposed restrictions, which are reported as temporarily restricted revenues, are released to unrestricted net assets when an expense is incurred that satisfies the restriction.

Contributions restricted for the purchase of property, plant and equipment are reported as nonoperating temporarily restricted revenues and are released to unrestricted net assets upon acquisition of the assets or when the asset is placed into service.

Contributions received for which the designation is pending by the donor are classified as temporarily restricted net assets. Once a designation is made by the donor, the contributions are reclassified to the appropriate net asset category as part of "net assets reclassified or released from restrictions."

Sponsored Activities

Revenues associated with research and other contracts and grants are recognized when related costs are incurred. Facilities and administrative cost recovery on U.S. Government contracts and grants is based upon a predetermined negotiated rate and is recorded as unrestricted revenue.

Fundraising Activities

Expenses incurred in carrying out the fundraising activities of the University, which amounted to

$18,391,000 and $18,901,000 for the years ended May 31, 2010 and 2009, respectively, are included primarily in the general administration expense category on the statement of activities.

Investments

Short-term investments consist of cash and cash equivalents, operating funds deposited in cash management accounts, and other investments with maturities at the time of purchase of 90 days or less, and are carried at market value. Cash and cash equivalents held in the investment portfolio are excluded from short-term investments.

Investment transactions are recorded on the trade date, realized gains and losses are recorded using the weighted average basis, and dividend income is recorded on the ex-dividend date.

Split-Interest Agreements

The University has split-interest agreements consisting primarily of charitable gift annuities, pooled income funds, and charitable remainder trusts. Split-interest agreements which are included in investments amount to $20,472,000 and $17,336,000 as of May 31, 2010 and 2009, respectively.

Contributions are recognized at the date the trusts are established net of a liability for the present value of the estimated future cash outflows to beneficiaries. The present value of payments is discounted with rates that range from 2.4% to 10.6%. The liability of $9,537,000 and $8,044,000 as of May 31, 2010 and 2009, respectively, is adjusted during the term of the agreement for changes in actuarial assumptions.

Use of Estimates

The preparation of financial statements in accordance with generally accepted accounting principles (GAAP) in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the period. Actual results could differ from those estimates.

6

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

Income Taxes

The University is a qualified tax-exempt organization under section 501(c)(3) of the Internal

Revenue Code.

Prior Year Summarized Information

The financial statements include certain prior year summarized comparative information, but do not include sufficient detail to constitute a presentation in conformity with GAAP. Accordingly, such information should be read in conjunction with the University's audited financial statements for the year ended May 31, 2009, from which the summarized information was derived.

Subsequent Events

Effective June 1, 2009, the University adopted a new accounting standard that provides guidance on the accounting and disclosure of events that occur after the statement of financial position date but before financial statements are issued or are available to be issued.

The University has assessed the impact of subsequent events through September 13, 2010, the date the audited financial statements were issued, and has concluded that there were no such events that require adjustment to the audited financial statements or disclosure in the notes to the audited financial statements.

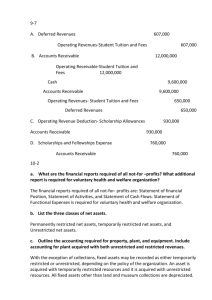

B. Accounts, Notes and Other Receivables

Accounts receivable and notes receivable are stated net of allowances for doubtful accounts. As of

May 31, 2010 and 2009 the allowance related to accounts receivable is $2,287,000 and $901,000, respectively.

Notes and other receivables consist of amounts due from students under U.S. Government sponsored loan programs and from the Weston Jesuit Community, Inc. under a ground lease agreement. The notes receivable due from students under U.S. Government sponsored loan programs are subject to significant restrictions and, accordingly, it is not practicable to determine the fair value of such amounts. As of May 31, 2010 and 2009, the allowance related to student notes receivable is $650,000.

On July 1, 2009, the University entered into a ground lease agreement with the Weston Jesuit

Community, Inc. Under this agreement, the University has commenced construction of a community residence for members of the Society of Jesus. The estimated total cost of

$22,100,000 for this community residence will be repaid to the University over a 30 year period with interest of 5%, beginning immediately following the issuance of a certificate of occupancy. At

May 31, 2010 the total receivable outstanding for construction in progress is $17,154,000.

7

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

C. Contributions Receivable

Contributions receivable are summarized as follows as of May 31:

(in thousands) 2010 2009

Unconditional promises scheduled to be collected in:

Less than one year

Between one year and five years

More than five years

Less discount and allowance for unfulfilled promises to give

Contributions receivable, net

$

$

56,669

137,220

42,619

(44,546)

191,962

$ 63,291

147,931

55,230

(45,041)

$ 221,411

A present value discount of $22,284,000 and $28,224,000 as of May 31, 2010 and 2009, respectively, has been calculated using discount factors that approximate the risk and expected timing of future contribution payments.

The University has reflected contributions received during fiscal 2010 and 2009 at fair value as determined in accordance with fair value accounting guidance.

Conditional promises of $8,616,000 and $9,474,000 as of May 31, 2010 and 2009, respectively, are not recorded in the financial statements.

D. Investments

Investments are stated at fair value and include accrued income. The value of publicly traded securities is based upon quoted market prices and net asset values. Other securities, for which no such quotations or valuations are readily available, are carried at fair value as estimated by management using values provided by external investment managers or appraisers. The

University believes that these valuations are a reasonable estimate of fair value as of May 31, 2010 and 2009, but are subject to uncertainty and, therefore, may differ from the value that would have been used had a ready market for the investments existed.

Included in the investment balances and investment return amounts, which follow, are funds held by trustees consisting principally of investments in United States Government obligations. These funds are maintained by the University to meet the requirements of certain licensing, secured note, and bond agreements, and as of May 31, 2010 and 2009, include $3,777,000 and $10,765,000, respectively, of construction funds held by trustees associated with the Boston College Series P and Series Q bond issues that will be drawn down to fund various construction projects.

Investments, including funds held by trustees, consist of the following as of May 31:

(in thousands)

Cost

2010

Market Cost

2009

Market

Equities

Fixed income

Real assets

Total

$ 1,067,944

349,644

126,973

$ 1,544,561

$ 1,257,890

391,546

108,775

$ 1,758,211

$ 1,061,093

316,900

134,323

$ 1,512,316

$ 1,091,131

339,348

119,923

$ 1,550,402

8

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

Equities include common stock, mutual funds, commingled funds and limited partnership interests.

Fixed income includes money market funds, treasury and agency securities and limited partnership interests.

A three level hierarchy of valuation inputs has been established based on the extent to which the inputs are observable in the marketplace. Level I is considered observable based on inputs such as quoted prices in active markets. Level II is considered observable based on inputs, other than quoted prices in active markets, and Level III is considered unobservable. Investments with annual redemption provisions are classified as Level II. The University's investments included in Level II and III primarily consist of alternative investments (principally limited partnership interests). Limited partnership interests with quarterly or annual redemption provisions are classified as Level II, others are classified as Level III.

The following tables present the financial instruments carried at fair value as of May 31:

(in thousands)

Level I

2010

Level II Level III Total

Equities

Fixed income

Real assets

Total

$ 551,880

304,380

9,711

$ 865,971

$ 512,172

7,055

28,679

$ 547,906

$ 193,838

80,111

70,385

$ 344,334

$ 1,257,890

391,546

108,775

$ 1,758,211

(in thousands)

Equities

Fixed income

Real assets

Total

Level I

$ 494,664

252,181

6,200

$ 753,045

2009

Level II

$ -

-

-

$ -

Level III

$ 596,467

87,167

113,723

$ 797,357

Total

$ 1,091,131

339,348

119,923

$ 1,550,402

9

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

The fair values of limited partnerships are represented by the net asset value of the partnership.

The objective of these investments is to generate long term returns significantly higher than public equity markets on a risk adjusted basis. Redemption terms for those investments valued at net asset value consist of the following as of May 31, 2010:

(in thousands)

Redemption Terms Equities

Fixed

Income

Real

Assets Total

Within 30 Days

Monthly

30-60 days prior written notice

Quarterly

30-90 days prior written notice

Semi-Annually, Annually

30-180 days prior written notice

1-5 years

6-10 years

Total

$ 81,759

51,290

112,545

266,577

126,533

67,267

$ 705,971

$ -

-

-

77,167

-

-

$ 77,167

$ -

-

12,321

16,359

22,100

14,715

$ 65,495

$ 81,759

51,290

124,866

360,103

148,633

81,982

$ 848,633

The University is committed to invest up to an additional $149,700,000 in private equity investments as of May 31, 2010.

As a result of new guidance related to estimating fair value of investments, certain investments which can be redeemed in the near term have been classified to Level II in 2010. The following tables include rollforwards of investments classified by the University within Level III as defined previously as of May 31:

(in thousands)

Fair value, June 1, 2009

Classified to Level II

Investment income, net

Realized and unrealized

gains(losses), net

Purchases and sales, net

Fair value, May 31, 2010

(in thousands)

Fixed

Income

2010

Real

Assets Equities Total

$ 596,467

(413,843)

(3,439)

$ 87,167

(6,347)

(893)

$ 113,723

(30,218)

(605)

$ 797,357

(450,408)

(4,937)

29,897

(15,244)

$ 193,838

13,561

(13,377)

$ 80,111

(10,588)

(1,927)

$ 70,385

32,870

(30,548)

$ 344,334

2009

Total

Fair value, June 1, 2008

Investment income, net

Realized and unrealized gains(losses), net

Purchases and sales, net

Fair value, May 31, 2009

$ 907,980

(5,961)

(160,844)

56,182

$ 797,357

10

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

The University recognized net realized and unrealized gains of $177,441,000 and investment income of $4,512,000, net of investment advisory fees of $12,127,000, for the year ended

May 31, 2010.

The University recognized net realized and unrealized losses of $408,366,000 and investment income of $4,871,000, net of investment advisory fees of $11,337,000, for the year ended

May 31, 2009.

E. Endowment

On July 2, 2009, the Commonwealth of Massachusetts adopted the Uniform Prudent Management of Institutional Funds Act (UPMIFA). UPMIFA provides new standards governing the investment accumulations and expenditure of the University’s endowment funds. The net assets associated with the University’s endowment funds are classified in accordance with relevant state law as interpreted by the Board of Trustees. These classifications are unrestricted, temporarily restricted, and permanently restricted based on the existence or absence of donor-imposed restrictions.

Unrestricted net assets include Board-designated funds, and any accumulated income and appreciation thereon. Temporarily restricted net assets include contributions not yet designated by donors and accumulated appreciation on temporarily and permanently restricted funds.

Permanently restricted net assets include contributions designated by donors to be invested in perpetuity to produce income for general or specific purposes.

The University has an endowment spending policy, as approved by the University's Board of

Trustees, which aims to preserve the purchasing power of the endowment. Under this policy, 5% of a three-year quarterly moving average of market values can be expended for operations. The long-term performance objective of the endowment portfolio is to attain an average annual total return that exceeds the University's spending rate plus inflation within acceptable levels of risk over a full market cycle. To achieve its long-term rate of return objectives, the University relies on a total return strategy in which investment returns are achieved through both capital appreciation and current yield.

As of May 31, 2010 and 2009 the market value attributable to certain endowment funds was less than the historical value of the related permanently restricted contribution by an aggregate of

$2,463,000 and $11,287,000, respectively. This has been reflected as a reduction of unrestricted net assets and will be restored to unrestricted net assets when the market value exceeds historical value. These deficits resulted from unfavorable market fluctuations.

11

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

F. Property, Plant and Equipment

The physical plant assets of the University are stated at cost on the date of acquisition or at fair market or appraised value on the date of donation in the case of contributions. Physical plant assets consist of the following as of May 31:

(in thousands) 2010 2009

Land and improvements

Buildings

Equipment

Library books

Rare book and art collections

Purchase options

Plant under construction

Property, plant and equipment, gross

Accumulated depreciation/amortization

Property, plant and equipment, net

$ 231,345

$

1,004,577

191,622

145,851

18,888

2,855

17,610

1,612,748

(573,137)

1,039,611

$ 229,967

962,539

179,000

138,162

17,652

2,855

38,242

1,568,417

(530,929)

$ 1,037,488

Annual provisions for depreciation of physical plant assets are computed on a straight-line basis over the expected useful lives of the individual assets, averaging 20 years for land improvements,

25-60 years for buildings, and 2-15 years for equipment. Depreciation for the years ended

May 31, 2010 and 2009 amounted to $45,042,000 and $43,598,000, respectively, and are allocated to functional expense categories on the statement of activities based on square foot usage calculations.

Library books are amortized over 50 years. Amortization amounted to $2,917,000 and $2,763,000 for the years ended May 31, 2010 and 2009, respectively. Rare book and art collections are reflected at historical cost and are not amortized.

Maintenance and repairs are expensed as incurred, and improvements are capitalized. When assets are retired or disposed of, the cost and accumulated depreciation thereon are removed from the accounts, and gains or losses are included in the statement of activities. The University retired or disposed of $7,865,000 and $18,245,000 in gross plant assets for the years ended

May 31, 2010 and 2009, respectively.

Property, plant and equipment additions of $6,577,000 and $4,670,000 included in accounts payable are reflected as a noncash item in the statement of cash flows for the years ended

May 31, 2010 and 2009, respectively.

The University recognized $369,000 and $372,000 of operating expenses relating to the accretion of liabilities associated with the retirement of long-lived assets, for the years ended May 31, 2010 and 2009, respectively. Conditional asset retirement obligations of $7,654,000 and $7,101,000 as of May 31, 2010 and 2009, respectively, are included in accrued liabilities.

The University has commitments of $23,065,000 to complete various construction projects as of

May 31, 2010.

12

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

G. Bonds and Mortgages Payable

Bonds and mortgages payable consist of the following as of May 31:

(in thousands) 2010 2009

Massachusetts Health and Educational Facilities Authority (MHEFA)

Boston College Issues (fixed rate)

Series K, 5.25 - 5.38%, due 2010 - 2015

Series L, 4.75 - 5.25%, due 2010 - 2032

Series M, 5.00 - 5.50%, due 2023 - 2036

Series N, 4.13 - 5.25%, due 2010 - 2038

Massachusetts Development Finance Agency (MDFA)

Boston College Issue (fixed rate)

Series P, 4.75 - 5.00%, due 2020-2043

Series Q, 3.00 - 5.00%, due 2011-2030

Department of Education

Library building bonds, 3.41%, due 2010 - 2023

Secured note, 3.00%, due 2010 - 2018

Bonds and mortgages payable, par

Net unamortized original bond issue premium

Bonds and mortgages payable, net

$ 23,495

107,665

134,285

102,255

176,980

95,695

7,735

1,312

649,422

22,265

$ 671,687

$ 27,510

108,955

134,285

103,340

176,980

95,695

8,180

1,455

656,400

23,036

$ 679,436

The Department of Education building bonds are collateralized by a mortgage on the O'Neill Library and the secured note is collateralized by funds held by trustees.

As of May 31, 2010, principal payments due on all long-term bonds and mortgages payable are as follows: 2011 - $11,472,000; 2012 - $12,012,000; 2013 - $12,627,000; 2014 - $13,286,000;

2015 - $13,996,000 and thereafter - $586,029,000.

As of May 31, 2010 and 2009, the estimated fair values of bonds and mortgages payable are

$706,466,000 and $697,938,000, respectively. The fair value of bonds and mortgages payable is based on rates currently available for instruments with similar maturities.

Interest expense for the years ended May 31, 2010 and 2009 amounted to $31,909,000 and

$27,876,000, respectively. Interest expense has been allocated to the functional expense categories on the statement of activities based on each functional area's corresponding use of the related space or equipment that was constructed or acquired through debt financing. The

University capitalized interest of $198,000 and $1,760,000 for the years ended May 31, 2010 and

2009, respectively.

The University has an agreement for a $75,000,000 unsecured line of credit. As of May 31, 2010 and 2009, there was no balance outstanding on the line of credit.

In May 2009, the University issued Massachusetts Development Finance Agency (MDFA) Series Q

Revenue Bonds in the amount of $95,695,000. The proceeds from this issue were used to retire outstanding debt, finance the acquisition of property located in Brighton, MA and fund project costs.

The University recognized a debt extinguishment charge of $104,000 and incurred costs of

$788,000 associated with this issue which have been capitalized and are being amortized over the life of the bonds. The MDFA Series Q Revenue Bonds were issued with an original issue premium of $9,123,000, which is being amortized over the life of the bonds.

13

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

H. Net Assets

I.

Net assets consist of the following as of May 31:

(in thousands)

2010

Unrestricted

2009

Endowment net assets,

beginning of year

Board designated

Donor restricted

Contributions

Investment return:

Investment income

Net appreciation/(depreciation)

Total investment return

Appropriation of endowed assets

for expenditure

Net assets reclassified or released

from restrictions

Other (losses) and gains, net

Endowment net assets, end of year

Board designated

Donor restricted

Designated for specific purposes

Net investment in plant

Program support

Contributions for plant assets

Student loans

Total net assets

Donor Restricted

Temporarily Restricted

2010 2009

Permanently Restricted

2010 2009

$ 659,934

-

-

(928)

89,663

88,735

$ 908,737

-

-

42

(211,704)

(211,662)

$ 196,740

7,448

$ 385,620

7,530

(313)

85,910

85,597

556

(176,153)

(175,597)

$ 634,484

44,371

$ 555,444

79,553

54

4,912

4,966

86

(13,535)

(13,449)

(42,453)

10,957

(103)

(41,801)

4,666

(6)

(40,651)

(2,137)

(1,224)

(36,955)

18,900

(2,758)

-

3,414

(2,425)

-

18,144

(5,208)

717,070 659,934

77,874

370,744

-

-

-

$ 1,165,688

58,518

367,682

-

-

-

$ 1,086,134

245,773

-

-

31,891

58,326

936

$ 336,926

196,740

-

-

30,913

61,002

958

$ 289,613

684,810

-

-

-

-

-

$ 684,810

634,484

-

-

-

-

-

$ 634,484

Retirement Programs

All eligible full-time personnel may elect to participate in a defined contribution retirement program.

Under the program, the University makes contributions, currently limited to 8-10% of the annual wages of participants, up to defined limits. Voluntary contributions by participants are made subject to IRS limitations. The limitation applicable to University contributions is on a combined plan basis. For the years ended May 31, 2010 and 2009, the University's contributions to the retirement program were $20,229,000 and $19,485,000 respectively.

The University provides certain health care benefits for retired employees who meet certain age and service requirements. Employees will become eligible for this benefit if they reach retirement while employed by the University. The plan does not hold assets and is funded as benefits are paid. The estimated future cost of providing postretirement health care benefits is recognized on an accrual basis over the period of service during which benefits are earned.

In fiscal 2010, the University increased the cost sharing for pre-65 retirees by 1%. The net impact of the change was a decrease in the benefit obligation of $16,000.

In fiscal 2009, the University announced a plan amendment under which contributions for future retirees will be based on a designated plan. The net impact of the change was a decrease in the benefit obligation of $4,120,000.

14

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

The net periodic postretirement health care benefit cost and other changes in plan assets and benefit obligation recognized in unrestricted net assets were determined as follows for the years ended May 31:

(in thousands) 2010 2009

Service cost

Interest cost

Amortization of prior service cost

Amortization of loss

Net periodic postretirement benefit cost

Prior service cost related to plan amendment

Net (gain) loss

Amortization of prior service cost

Amortization of loss

Other changes in plan assets and benefit obligation

Total recognized in net periodic benefit cost and

unrestricted net assets

$ 2,364

3,175

(1,044)

387

4,882

(16)

10,766

1,044

(387)

11,407

$ 2,333

3,012

(499)

139

4,985

(4,120)

3,165

499

(139)

(595)

$ 16,289 $ 4,390

In fiscal 2011, the prior service cost credit of $(1,050,000) and unrecognized net loss of $1,030,000 are expected to be amortized as a component of net periodic postretirement benefit cost.

For measurement purposes, the assumed annual rates of increase for the year ending

May 31, 2011 were; 7.25% in the per capita cost of covered health care benefits for post-65 benefits, 7.50% in the per capita cost of covered health care benefits for pre-65 benefits, and

7.00% in the Medicare Part D subsidy integration threshold. All three rates were assumed to decrease gradually to 5.00% in 2015 and remain at that level thereafter.

A one percentage point change in the assumed health care cost trend rates would have the following effect:

(in thousands) Increase Decrease

Effect on total of service and interest cost components

Effect on postretirement benefit obligation

$ 942

8,343

$ (770)

(6,980)

The discount rate used to determine the accumulated benefit obligation is 5.75% and 6.50% as of

May 31, 2010 and 2009, respectively. The discount rate used to determine the net periodic postretirement benefit cost is 6.50% as of May 31, 2010 and 2009.

15

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

A reconciliation of the accumulated postretirement benefit obligation and plan assets are as follows as of May 31:

(in thousands) 2010 2009

Reconciliation of accumulated postretirement

benefit obligation

Benefit obligation, beginning of year

Service cost

Interest cost

Plan participant contributions

Part D subsidy received

Actuarial (gain) loss

Benefits paid

Plan amendment

Benefit obligation, end of year

Amounts recognized in statement of financial position

consist of:

Accrued liabilities

Amounts recognized in unrestricted net assets

Prior service cost

Net actuarial loss

$

$

$

46,556

2,364

3,175

302

216

10,766

(2,238)

(16)

61,125

61,125

$

$

$

43,919

2,333

3,012

286

-

3,165

(2,039)

(4,120)

46,556

46,556

$

$

(4,954)

16,222

11,268

$ (5,982)

5,844

$ (138)

Expected benefit payments, net of participant contributions and expected Medicare retiree drug subsidy is as follows: 2011 - $2,154,000; 2012 - $2,740,000; 2013 - $2,966,000;

2014 - $3,206,000; 2015 - $3,427,000; and the five fiscal years thereafter - $20,781,000. The expected Medicare retiree drug subsidy is as follows: 2011 - $606,000; 2012 - $244,000;

2013 - $243,000; 2014 - $241,000; 2015 - $238,000; and the five fiscal years thereafter - $1,089,000.

J. Related Party

Boston College Ireland, Ltd. ("BCI") is a nonprofit entity established as an institute of education in the Republic of Ireland. The University has an investment in the real estate used by BCI for educational and rental purposes. The value of the investment as of May 31, 2010 and 2009 amounted to $1,671,000 and $4,077,000, respectively, and is included in the University's real estate investments.

The University has mortgages, loans and notes due from various related parties of $23,482,000 and $23,320,000 as of May 31, 2010 and 2009, respectively.

16

Boston College

Notes to Financial Statements

May 31, 2010 and 2009

K. Commitments and Contingencies

The University has several legal cases pending that have arisen in the normal course of its operations. The University believes that the outcome of these cases will have no material adverse effect on the financial position of the University.

The University leases facilities and campus transportation under various operating lease agreements, the last of which expires in 2020. The University incurred operating lease expenses of $4,993,000 and $4,852,000 for the years ended May 31, 2010 and 2009, respectively. At

May 31, 2010, the minimum aggregate commitments for all current operating leases are as follows:

2011 - $4,876,000; 2012 - $4,952,000; 2013 - $1,021,000; 2014 - $400,000; 2015 - $333,000 and thereafter - $1,525,000.

17