Manish, William, & Sarah

advertisement

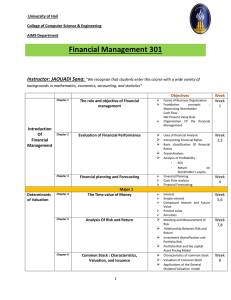

Manish, William, & Sarah CURRENT HOLDINGS AT&T Verizon China Mobile Ltd. NII Holdings 0% 0% 2.41% 0.98% SUGGESTED HOLDINGS • Buy: AT&T NII Holdings 2.14% 0.27% • Sell China Mobile Ltd. 2.41% Smallest company of the three with a market cap of 3.93B Competes in a foreign, niche market in South and Latin America Has a high beta of 2.02 and behaves more like a growth stock Is a young company with limited historical data. Growth: Credit: History: • Spin off of Nextel • Rapid growth in Latin and Central America • Downturn in profits associated w/unemployment and Mexico problems (N1H1, drug trafficking decreased tourism) 2009 Projected Sales Projected Earnings 5.27B 350M 2006 ROE GPM 72% 2010 2011 4.80B 320M 2007 4.20B 250M 2008 2.7 3.2 72% 73% Valuation measures: • Historical price ratios—the ratios have currently contracted, most likely due to the economy • Future valuations—as the economy improves, the ratios should expand Relative to the industry and • The ratios have contracted Target price: $33.86 Major S&P 500 determinants of value: operating margin on service revenues, depreciation expense and capital expenditures Relative to Industry P/Trailing E High Low Median Current Target Multiple Target E, S, B, Target Price etc/Share 3.2 0.15 1.4 0.19 P/Forward E 2.2 0.04 1.3 0.04 P/B 7.9 1.3 4.4 1.5 P/S 3.3 0.9 2.0 1.1 P/CF 5.7 1.2 2.7 1.5 EntValue/EBIT 4.10 DA P/Trailing E 3.2 1.06 2.67 1.28 0.53 2.0 0.63 P/Forward E 2.3 0.60 1.4 0.62 P/B 4.7 0.8 2.9 0.8 P/S 3.4 0.8 2.1 0.8 P/CF 3.0 0.4 1.7 0.5 EntValue/EBIT 2.92 DA P/Forward E 34.3 0.55 1.89 0.67 6.7 22.5 9.3 15.9 2.5 40.30 P/S 5.4 0.5 3.2 0.7 2.0 33.7 65.66 P/B 14.4 1.2 8.3 1.7 5.0 13.9 69.32 P/EBITDA 20.38 1.98 12.82 2.95 7.9 8.0 63.00 P/CF 32.8 2.8 18.7 4.1 11.4 5.7 65.54 Buy 0.27% of NIHD to bring the holding up to 1.25% of the total SIM Primary catalysts • Valuation: 80%/20% DCF/Valuation model gives a 1 year target price of $33.86 Risks: • Double Dip recession (high beta) • Political uncertainty China Mobile provides a wide variety of mobile communication services in 31 provinces in China Largest wireless provider in the world by customer In January 2009, the company started offering 3G services Beta: .91 Sell 2.41% of CHL Primary Catalyst: successful 3G network Risks: • High penetration rate • Strong competition in Chinese market • Market in certain large cities showing signs of maturity • iPhone?? Potential deal between Apple and China Unicom (competitor of China Mobile) Largest telecom company in US ( Market cap $147.68 billion) Best brand in Telecom - Ranked no. 1 company in telecom sector by fortune magazine (11 times in last 14 years) Business Segmentation • • • • Wireline Services – Voice and Data (55% of total revenues) Wireless Communications and Services (39% of total revenues) Advertising and publishing (4% of total revenues) Other Segment (2% of total revenues) Major competitors - Verizon, Sprint Nextel Corp. and Tmobile USA, Inc. ($MM) 2008 2007 2006 2005 2004 Revenue $124,028 Net Income Trend $118,928 $63,055 $43,848 $40,733 Up $12,867 $11,951 $7,356 $4,870 $4,487 Up EPS 2.17 1.95 1.89 1.42 1.78 Up Total Assets $265,245 $275,644 $270,634 $145,632 $110,265 Up Dividend 1.61 1.47 1.35 1.3 1.26 Up Capital Expenditure per year $25,000 $20,000 $15,000 $10,000 $5,000 $0 2008 2007 2006 2005 2004 Current Price Implied equity value/share Target Price Upside to DCF $24.45 $36.27 $26.99 48.35% Discount Rate Terminal Grow th Rate 9.5 10 10.5 11 11.5 12 12.5 2.5 40.23 37.46 35.03 32.88 30.98 29.28 27.75 3 42.02 38.94 36.27 33.94 31.88 30.06 28.42 3.5 44.09 40.65 37.69 35.13 32.90 30.92 29.17 4 46.55 42.64 39.33 36.50 34.04 31.89 30.00 4.5 49.50 45.00 41.25 38.08 35.35 33.00 30.93 5 53.10 47.83 43.51 39.91 36.87 34.26 31.99 5.5 57.60 51.29 46.23 42.09 38.63 35.71 33.20 Absolute Valuation Median Current #Your Target Multiple *Your Target E, S, B, etc/Share Your Target Price (F x G) P/Forward E 16.0 8.5 12.5 2.01 25.13 P/S 2.1 1.1 1.3 21.82 28.37 P/B 2.2 1.5 1.7 16.27 27.66 P/EBITDA 5.23 2.89 3.4 8.46 28.76 P/CF 6.7 3.9 4 6.27 25.08 Buy 2.14% of AT&T • Primary catalysts Valuation: 80%/20% DCF/Valuation model gives a 1 year target price of $34.14 Brand name, Market Cap and ability to form alliance- (Apple iPhone 3G) Pros: • 2008 annual report marked Consolidated revenues up by more than 4 percent to $124 billion in year. Reported earnings per share grew by 11.3 percent to $2.16 per share. Returned $15.6 billion to stockholders through dividends and share repurchases. Delivered strong cash flow - 25th consecutive year of dividend growth Cons: • Slow growth due to cut throat competition and worsening economy Buy AT&T (2.14%) • Very large upside, largest telecom company in the US Buy NII Holdings (0.27%) • Niche market, upside. Sell China Mobile (2.41%) • Reaching its maturity, small downside, increasing competition