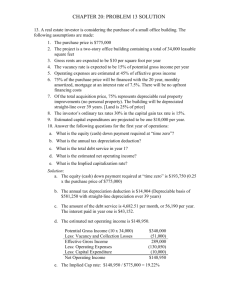

Federal Income Taxation Chapter 3 Compensation for Losses Professors Wells Presentation:

advertisement

Presentation: Federal Income Taxation Chapter 3 Compensation for Losses Professors Wells August 26, 2015 Clark v. Commissioner p.90 Facts: Clark paid $19,941.10 by tax counsel to compensate Clark for consequences of advising to file a joint tax return and not separate returns. IRS Position: What is their argument for income? Court’s holding: What is the underlying theory? 2 Recoveries for Personal and Business Injuries p.92 Issue: What are the damages a substitute for? Raytheon case: damages in antitrust action – ordinary income where damages represent payment for a loss of profits. Damages as a return of capital where destruction of the business and goodwill. Here: destruction of goodwill – but no tax basis proved and, therefore, assumed to be zero (and all proceeds as income –CG?). 3 Windfall Gains Glenshaw Glass p.96 Punitive portion of a treble damage antitrust recovery is includible as gross income under [now] Code §61. Income is to be determined based on “accession to wealth, clearly realized”. No requirement of “source-based” taxation (cf., Eisner v. Macomber re stock dividends). Can be recurring or non-recurring receipts. 4 Home Run Ball and Treasure Trove p.101 Supp. pp. 28-30 Treas. Reg. §1.61-14: “Treasure trove, to the extent of its value in United States currency, constitutes gross income for the taxable year in which it is reduced to undisputed possession.” IRS press release states that no gift tax if ball given back to McGwire but the tax consequences “may be different’ if the fan retained the ball for sale. Cesarini v. U.S. cash found in a piano. Included in gross income upon discovery because this was income from whatever source derived, citing Treas. Reg. §1.61-14(a). • What if discovered that the piano was a famous Cristofori piano that was purchased for $15 at a garage sale? • What if you discover oil on your land? 5 Damages for Personal Injury “Prior Law” p.104-106 Solicitor’s Opinion 132: • “[G]ross income does not include everything that comes in” • The statutory exclusion for personal injury damages, first enacted in 1918, may have merely codified the result reached under prior law, which had been based on the conclusion that damages for personal injury are not “income” under the early tax acts. • Emotional distress type damages, such as for alienation of affection, were apparently not thought to constitute damages for personal injury under the original understanding of the statutory exclusion (page 104); • Damages for slander or libel affecting business or professional reputation or property rights was apparently understood early on to constitute income (see limiting interpretation of Sol. Mem. 957, page 104); and • Most importantly, receipt of damages for invasion of nontransferrable personal rights (“not assignable and not susceptible of any appraisal in relation to market values”)— although a money that comes in—involves no derivation of gain or profit, and so is not within the general definition of income. Rev. Rul. 74-77: amounts received for alienation of familial rights is not gross income to the recipient. 6 Damages for Personal Injury Attn: Tort Lawyers p.108 Code §104(a)(2) – exclusion for damages received for personal physical injuries. The “physical injury requirement” cuts back the holdings of cases that involved discrimination claims, loss of familial rights (Rev. Rul. 74-77), and scope of Solicitor Opinion 132. The omitted Murphy case upheld the constitutionality of taxing nonphysical injury personal awards. Exclusion whether received as a lump sum payment or in periodic payments. Not including sex/race/age discrimination lawsuit proceeds. Not including payments for emotional distress (unless distress attributable to physical injury). Punitive damages are includible in Gross Income. See p. 128 7 Structured Settlements p.108 Supp. p. 31 What is a “structured settlement”? Code §104(a)(2) provides for exclusion whether amount received “as lump sums or as periodic payments” for amounts received for personal physical injuries. 1. What about the “interest” income component inherent in the delayed payments? 2. How assure that the agreed deferred payments will actually be made? EXAMPLE: Assume court petition/ complaint specifies $1 million compensatory and $9 million punitive. Parties then settle for $2 million: how allocate this amount to excluded and included amounts? Amend the petition prior to effective date of the settlement agreement? EXAMPLE: What is the result result of the NFL’s $765 million concussion settlement with former players reached on 8/29/2013? 8 Medical Expense Recoveries p.129 Tax Treatment of Insurance for Medical Care Funding Method Premiums Proceeds Employer Provided Coverage Excluded, §106 Individually Purchased Insurance Limited Deduction, §213(d)(1)(D) Excluded, §104(a)(3) Self-Insurance N/A Excluded, §105(b) Limited Deduction, §213(a) 1. §105(b): Health insurance payments made by an employer provided health plan do not represent income to the employee. 2. §104(a)(3) excludes insurance proceeds received under employee purchased health plan. 3. Premiums paid by employees for their health insurance are nondeductible except in limited long-term care situations (see §213(d)(1)(D) and (d)(6)), but the premiums paid by the employer are deductible for the employer (§162(a)) and not income to employee (see §106). 9 4. Tax Expenditure Impact in 2015: 207.2 billion (p.536). Disability Insurance p.146 Gross income if disability payments are made by employer provided health insurance as §105(b) only excludes amounts received to pay “medical care” and not to supplement wages. But, employer is entitled to deduction for these amounts (see §162(a)). Gross income excludes disability insurance payments for payments on individually purchased insurance under §104(a)(3) as §104(a)does not require amounts be paid for “medical care.” But, the employee is generally not entitled to a deduction for premium payments for disability policies (see §213(d)(1)(D)). 10 Life Insurance - Code §101 GI Exclusion p.147 What is “life insurance”? A payment for dying – ordinarily paid in a lump sum. If paid at death, why not call it “death insurance,” rather than “life insurance”? Gross income exclusion (§101) is available when proceeds are paid at death for both: (i) the pre-death interest buildup, and (ii) the mortality gain (i.e., “windfall” because of early death). The “transfer for consideration” limitations may apply. §101(a)(2). Purpose of limits? The gross income exclusion is not applicable to any post-death interest accumulation. continued 11 Life Insurance, cont. p.148 No income tax deduction is available for policy premiums paid. §264(a)(1). Policy loans are not treated as distributions. Code §72(e)(5)(A). Policy settlement options after maturity at death: a deferred receipt produces taxable interest income; see Code §101(c) & (d) (concerning the annuity option). continued 12 Life Insurance, cont. Defining Life Insurance p.148 If not treated as “life insurance,” then taxed as if a “savings account”: i.e., inclusion in current income of: (i) increase in cash surrender value of the account, and (ii) value of current insurance coverage. 13 Employer Paid Life Insurance p.150 Employer’s payment of premiums – gross income inclusion (unless employer is the beneficiary). Same as Old Colony? But, §79 – exclusion from gross income for first $50,000 of group term insurance provided by employer. What is “term life” insurance? Employer deduction available? Tax Expenditure impact of this exclusion is $28.9 billion (see p. 17) 14 Problems Life Insurance 1. 2. 3. 4. p.150 A purchased a $100,000 life endowment insurance policy. At age 65, after A had paid total premiums of $80,000, the policy matured and the insurance company began to make payments to A under the policy. A will be paid $10,000 a year for as long as she lives; if she dies before age 75, any excess of $100,000 over what has previously been paid to her will be paid to her estate or designated beneficiary. How are periodic payments under this policy taxed? How much, if any, of the lump-sum payment will be taxed if A dies before age 75? B owned a life insurance policy on his own life. In order to remove it from his estate for federal estate tax purposes, B transferred the policy to his daughter in exchange for securities worth $45,000. Shortly thereafter, B died and the policy was paid off at the face amount of $100,000. Is any part of the proceeds taxable as income? C purchased a $100,000 paid-up life insurance policy for $60,000. With the remaining $40,000 she purchased a life annuity, which will pay $5,000 a year. C then transferred the life insurance policy as a gift to her daughter. How will payments under the annuity contract and the life insurance policy be taxed? National Bank lent D $100,000 and required D to purchase credit life insurance in that amount, payable to the bank. D defaulted, and Bank deducted $100,000 as a bad debt loss. Subsequently D died, and Bank collected $100,000 from the insurer. Is that recovery taxable to Bank? McCamant v. Commissioner, 32 T.C. 824 15 (1959). Sanctity of Annual Accounting Period p.151 Burnet v. Sanford & Brooks For the period 1913-1916 had reported gross income for receipts and offsetting expenses. The expenses exceeded income during this period. Work abandoned & suit to recover. In 1920 taxpayer received $192,578 (176,272 for return of losses and accrued interest of 16,306). Held: Inclusion in gross income of the amount received in 1920. 16 Tax Benefit Rule Limitations: Dobson v. Commissioner p.156 Facts: Taxpayer purchased 300 shares of stock and found the stock was not registered correctly and recovered $45,150.63 • $23,296.45 allocable to 100 shares taxpayer had sold in 1930 (prior tax deductible loss of $41,600.80) • $6,454.18 allocable to 100 shares sold in 1931 (prior tax deductible loss of $28,163.78) • $15,400 related to 100 retained shares. IRS treated $15,400 received for the 100 retained shares as a return of capital but treated the amounts received for sold shares as income. Issue: Must the proceeds of settlement attributable to shares sold in 1930 and 1931 be included in gross income? Held: The recoveries allocable to the shares sold were taxable only to the extent that the earlier year losses produced a tax 17 benefit—i.e., a reduction in taxes in the earlier years. The Inconsistent Events Rule (Supp. pp. 32-37) Hillsboro and Bliss Dairy cases – 1) Repayment to bank shareholders of taxes on shareholders paid by bank corporation. No recognition required of the bank when refunds to shareholders. 3) Distribution of previously expensed assets (cattle feed) in a corporate liquidation. Recovery required to the corporation on the distribution. Dissent: file revised returns 18 Alice Phelan Sullivan (Supp. pp. 38-39) Charitable Contribution Deduction & Gift Returned 1) Property transferred to charity 2) Charitable deduction claimed for tax 3) Property returned to donor 4) Inclusion in donor’s gross income? Yes to extent of lesser of earlier deduction or fair market value of property 19 Modifications – The Tax Benefit Rule p.165 Transactions treated as closed and completed transaction – but the tax treatment of the subsequent transaction will be colored in light of the earlier transaction. Two Prongs: Inclusionary Prong (Alice Phelan/Hillsboro): A recover in later year is included in gross income if the loss in the earlier year provided a tax benefit. Exclusionary Prong (§111): A recovery of a loss in a later year is excluded from gross income to the extent the earlier deduction produced no tax benefit. 20