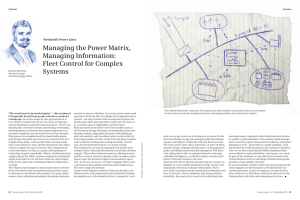

The Price of Oil over the Last Five Years

advertisement

Oil and Gas Decentralized Energy Volatile Prices – Balanced Response The Price of Oil over the Last Five Years 110.00 100.00 90.00 80.00 70.00 59.67 50.00 What do you do when the costs in your industry have doubled over the past couple of years, and then the price you can charge for your product halves in just six months? Welcome to the dilemma faced by developers and operators in the upstream oil and gas sector. 40.00 2,000,000 1,000,000 0 30.00 2011 2012 2013 2014 2015 Source for all data: www.nasdaq.com/markets/crude-oil.aspx?timeframe=5y, May 2015 Text: Ward Pincus oil production 56 Living Energy · No. 12 | July 2015 through the rest of the decade. Also, China is no longer increasing oil consumption at the same pace as it was over the past decades. On the supply side, there is plenty of oil coming into the market over the medium term. As outlined by Hasan Qabazard, OPEC’s Director of Research between 2006 and 2013, non-OPEC suppliers will continue to add to global supplies until the end of the decade. US shale oil currently produces just under 5 million barrels per day (bpd), up from less than a m ­ illion bpd only a few years ago. But despite the price decline, he expects total US shale oil production to grow to 6 million bpd by 2018/19, when it will then plateau. Other non-OPEC oil will also contribute to medium-term supply, says Qabazard, who is the Chief Executive Officer of the Kuwait Catalyst Company and also a ­former Director of the Petroleum ­Research and Studies Center at the Kuwait Institute for Scientific Research. Longer term, however, both Qabazard and Dubaibased Robin Mills, Head of Consulting at Manar Energy, see oil prices rising as global demand continues to grow while non-OPEC production fails to maintain its recent heady pace. OPEC estimated in late 2014 that global energy demand will increase by 60 percent by 2040 compared to 2010 levels, with world oil output projected is expected to grow to 6 million bpd by 2018/19 OPEC estimates that global energy demand will increase by 60 percent by 2040 compared u Photo: Getty Images E veryone is aware of the sharp fall in oil prices that began in mid-2014, and uncertainty ­continues to cast a shadow over the prices in the medium term. What seems likely, however, is that oil will remain at more moderate prices ­until, at least, the next decade. This is driven both by the demand and the supply side. On the demand side, emerging market growth isn’t expected to hit the same pace as it had over the past ten years, when ­many of those years saw real GDP growth between 6 and 9 percent a year. The IMF forecasts emerging market growth at 4.3 percent this year, 4.7 percent next year and just over 5 percent US shale to 2010 levels World oil output is projected to grow from 81.8 million bpd to 99.6 million bpd until 2040 Living Energy · No. 12 | July 2015 57 Decentralized Energy “However the oil and gas market ­develops in the short term, it offers uniquely attractive perspectives over the long term.” Lisa Davis, responsible for Oil & Gas and Member of the Managing Board at ­Siemens AG Comprehensive Oil and Gas Portfolio With its recent acquisition of the Rolls-Royce Energy gas turbine and compressor business, and the announced agreement to acquire Dresser-Rand, ­Siemens is building a comprehensive portfolio across the entire oil and gas value chain, from power generation, distribution and control systems to ­f ield-proven compressors, water processing, automation and control and electric-drive-related products, systems and solutions. These acquisitions are not only a matter of technology, but also of valuable human capital. “The recent additions to our oil and gas ­portfolio almost double our pool of talent and create a truly global strategic partner for all of ­Siemens’ oil and gas customers,” says Lisa Davis. The acquisition expands the ­Siemens portfolio to include high-efficiency, compact aeroderivative gas turbines. ­Especially attractive in offshore applications where costs grow as equipment weight and space increases, the lighter, more compact aero­ derivative gas turbines offer significant advantages. Furthermore the aeroderivative ­turbines offer high availability and reliability, delivering operational advantages with short maintenance cycles. 58 Living Energy · No. 12 | July 2015 Looking to expand the port­ folio in the oil and gas field equipment. Rising Costs in the Field Photos: Getty Images, ­Siemens, Chris McEniry Light and compact: aeroderivative gas turbine. The agreement to acquire Dresser-Rand will enable ­Siemens to expand its oil and gas field equipment portfolio, including high-pressure field injection and oil recovery, gas ­liquefaction, gas transmission and refinery process equipment. DresserRand also adds additional distributed power generation technologies to the S ­ iemens Oil & Gas solutions, including reciprocating engines that provide power to field equipment such as compressors, and micro liquefied natural gas solutions that are ideal for smaller-volume associated gas found in fields such as unconventional shale oil. to grow from 81.8 million bpd to 99.6 million bpd over the same period. The OPEC study also predicts that the share of oil in the global energy mix will fall from nearly 32 percent to 24.3 percent, while the share of all fossil fuels, including oil, coal and gas, in the global energy mix will decline from 81.6 percent to 78.4 percent. Mills said he is more bullish than the market consensus regarding ­renewable energy’s ability to take a larger share of the energy mix, but says that fossil fuels will “probably still be the major source” of energy by 2040. This is driven by renewable energy’s technology mismatches, most notably in transport, Mills says. Furthermore, disruptive technologies such as carbon capture and storage could change the calculus by making fossil fuels as “clean” as renewables, he says. But there is another part of the p ­ icture that was putting a squeeze on producers long before prices collapsed: the skyrocketing costs associated with drilling and producing oil and natural gas around the world. Energy consultancy IHS studied the return on capital among upstream players and found that it had fallen by more than half between 2000 and 2013, from a 23 percent net income return on net cumulative capital costs in 2000 to an 11 percent return in 2013. That was even as average oil prices tripled from just above US$22 per barrel of oil equivalent to US$63. As Mills notes, the reasons for the price rise were manifold, including companies losing discipline in the face of high prices, overstretched equipment and qualified mid-career experts in the face of so many projects, more difficult and complex ­projects, and these complex projects turning out to be even more difficult than expected. Operators React to Price Collapse The sharp fall in prices is forcing ­operators and service companies to address these cost issues more consequently than was required with oil at US$100. The first step being ­taken by most operators, both national oil companies and international oil ­c ompanies, are sharp and widespread cutbacks in capital spending. This means canceling and delaying nonstrategic investments, retendering others and renegotiating fees with suppliers, both because of the need to share the pain of lower ­prices, and also to capture the gains of falling material prices, which have begun to come down in recent months. BP is halving its exploration activity and slashing capital expenditure by 20 percent; Shell plans to reduce costs by US$15 billion over the next three years, and Statoil is cutting its capital spending for 2015 by 10 percent. In turn, some of the world’s biggest oil field services firms, including ­Baker Hughes, Schlumberger and Halliburton, are laying off thousands of employees. Regional Responses The steep drop in oil price is impacting all regions, though each in its own way. In the North Sea, there is a big mismatch between current prices and operating costs. That worries Dr. Patrick O’Brien, Chief Executive of the Industry Technology Facilitator (ITF), whose organization is based in Aberdeen. “We are much later in the life of the [North Sea] basin, compared to other regions, so the threat is that [with low oil prices] we start to shut down and decommission ­before we should. […] This should drive people to think how to do things differently.” In North America, there is urgency to bring down costs in the face of lower prices. Qabazard says that the ability of North American unconventional producers to leverage technology and improve system and operational efficiencies to lower costs is ­ eing seen in the declining already b break-even curve for those fields. Before the oil price collapse, these operators had a break-even point of between US$40 and US$120/barrel, he says, but now, they are reportedly operating at ­between US$20 and ­US$70/barrel. In the Middle East, the national oil companies are less exposed to the price drop because they have ­lower-cost operations, and also ­generally have a longer time horizon. This means most upstream projects are strategic in nature and not ­subject to suspension or cancellation, Living Energy · No. 12 | July 2015 59 u Field Innovation and Technology Advances One of the most effective ways to reduce costs in an oil and gas field – whether onshore or offshore – is to use electric-drive pumps, compressors and process equipment that is connected to a power grid and a control system, instead of diesel-powered mechanical-drive equipment. Electricity powering the grid can come from a high-efficiency gas turbine, from a combined “We’re focusing our innovative strength on ­setting new standards for ­efficiency and reliability.” Digitization With digitization and automation, operators can collect real-time data on equipment and operations, and also remotely manage the equipment more efficiently. Big data and other analytics help operators cut costs and improve efficiencies by optimizing performance and enabling ­predictive and preventive maintenance. With sensors and control equipment located across the field system, operators require fewer field ­engineers, something that delivers big cost advantages particularly in offshore and remote fields. Digitization allows for real-time monitoring of wellheads so operators can manage equipment better. For example, through real-time monitoring of the mix of fluid, sand, rock and hydrocarbons coming through a wellhead, pumps can be adjusted accordingly to reduce wear and tear, and prevent damage. Another exciting implementation of digitization is to take the extensive experience S ­ iemens has in image processing in fields such as health care and bring them to the visualization of oil and gas reservoirs. It is a key challenge in the exploration and development phase to take the extensive information from ultrasound, seismic, core samples and flow data to build a picture of what the subsurface reservoir looks like. Using ­Siemens software, exploration companies can get a better view of the reservoir in real time or near real time, allowing them to make decisions faster, thereby reducing costs associated with expensive leased rig and other field equipment. Lisa Davis heat and power plant, or even from a combined renewable and fossil-fueled plant. Operators benefit most significantly from electrification through improved reliability and availability, and thus better field efficiency. Furthermore, Subsea Power Grid electrification can reduce operating costs through greater fuel efficiency and the lower maintenance and operating costs associated And while the initial capital outlay is larger with electrification, overall capital costs can be lower because production generally can begin sooner and is less likely to face start-up delays. Electromagnetic heating can be used to unlock much more of a thick oil reservoir’s potential. Electromagnetic Heating Further out the innovation curve is the ­Siemens development of electromagnetic heating for use in unconventional heavy oil fields such as those found in Canada and Kuwait. While current technology gets this thick oil moving by ­using steam, electromagnetic technology offers a way to unlock much more of a reservoir’s potential, while having a dramatically smaller physical and environmental footprint that requires no water and avoids the inefficient twostep process of creating heat that then is applied to water to create steam. Photos: ­Siemens with electrical motors and drives. Cutting costs through digitization and automation. The subsea grid is operational to depths of 3,000 meters below sea level. ­ iemens is also leading innovation in the field of S subsea power grids for large-scale processing on the sea floor. Currently in the detailed design and test phase, this solution will provide offshore operators with a complete medium-voltage system that includes subsea transformers, subsea switchgear and subsea variable speed drives that are operational to depths of 3,000 meters below sea level. This brings processing closer to the reservoir and mitigates sea-surface platform risks, including those associated with weather. Also incorporating a comprehensive power control and communication system, the solution is ­designed to deliver long service intervals with ­exceptional availability, and includes an integrated condition monitoring system to identify and ­address unplanned downtime issues before they impact operations. ­Siemens’ recent investments in expanding its portfolio and bringing its expertise to the challenges of the oil and gas sector reflects the company’s commitment to the sector. “We’re now also focusing our ­innovative strength on the oil and gas sector and setting new standards for efficiency and ­reliability,” says Lisa Davis. u Oil and Gas ­ sing enhanced oil recovery techu niques – such as CO2 injection – and extending the service life of field infrastructure. Given these priority areas, operators and service companies can begin ­cooperating right away to realize ­systems and solutions enhancements. “However the oil and gas ­market ­develops in the short term, it offers uniquely attractive perspectives over the long term,” says Lisa Davis, ­responsible for Oil & Gas at ­Siemens and Member of the Managing Board at S ­ iemens AG. Solutions to Cut Costs “Better IT, field ­automation and virtual work could help staffers be more ­productive.” Robin Mills, Head of Consulting, Manar Energy Robin Mills, Head of Consulting at Manar Energy. 62 Living Energy · No. 12 | July 2015 There are many steps the industry and individual operators can take to bring down costs and increase production. In addition to adopting new technologies, experts agree that the industry also can bring down costs by managing fields more efficiently, pursuing cross-operator standardization, and improving field operations efficiency. Mills adds that streamlining the ­supply chain, implementing better ­contracting models that create a more collaborative relationship ­between operators and service companies also would help. To help address the shortage of qualified field engineers, he says better IT, field automation and virtual work could help ­existing staffers be more productive. Outside of North America, there is a sense that innovation moves more slowly than it could. “You hear a lot about technology that’s out there but that’s not being taken up,” says O’Brien, whose organization, ITF, is comprised of international oil and gas operating and service companies that collaborate on research and ­development initiatives to address shared technology challenges. Examples of ITF’s work include ­fundamental research on the basic ­algorithms for imaging subsurface reservoirs, understanding how cracks grow during hydraulic fracturing (fracking), and algorithms to more accurately model and predict weather that impacts offshore Australian oil fields. Hasan Qabazard, Chief Executive Officer of the Kuwait Catalyst Company, and OPEC’s Director of Research between 2006 and 2013. O’Brien recognizes the huge imperative for safety in this industry, given the human, environmental and commercial harm from a disaster. But he says this has created a different risk of “overspecifying, overdesigning, overcustomizing.” This not only makes operators and service companies more conservative in adopting new technologies, but it also makes it harder to share lessons learned and to reduce costs through some levels of standardization. Other areas of technology development that the experts mention ­include field electrification, the implementation of CO2 injection to ­support enhanced oil recovery, and technologies to unlock the potential of heavy oil and tar sands. O’Brien says that while the sharp drop in prices might be painful today, in the future “we may find ourselves saying it was a good thing because it made us focus on really trying to do things differently. Maybe it will help us achieve more innovation than we’ve had in recent times.” p Ward Pincus (Dubai) is a Middle East expert who writes on science, technology, health, and business issues for publications in North ­America, Europe, and the Middle East. He is a former correspondent for the Associated Press (AP) in the United Arab Emirates. Photos: Private, Getty Images though operators are pushing ­service companies on price. As Qabazard says, countries such as Saudi Arabia, the United Arab Emirates and Kuwait will continue to ­invest in production expansion to achieve their strategic goals of having the necessary production capacity ­onstream to deliver the residual supply to global markets that will be needed once non-OPEC supply plateaus in the early 2020s. Gulf operators are concerned about improving the efficiency of fields, “We may find ourselves saying that the sharp drop in prices was a good thing because it made us ­focus on really trying to do things differently. Maybe it will help us achieve more innovation than we’ve had in recent times.” Patrick O’Brien, Chief Executive of the Industry Technology Facilitator (ITF)