2.5.1-2.5.2 market s..

advertisement

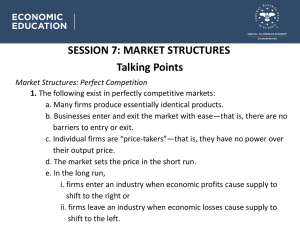

You’ve likely played the game, but have you ever stopped to ask yourself why it was called that? Notice there are 4: Monopoly Oligopoly Monopolistic Competition Pure Competition Let’s look at them one at a time and compare Monopoly Exists when a specific person or enterprise is the only supplier of a particular commodity Monopolies are thus characterized by a lack of economic competition to produce the good or service and a lack of viable substitute goods. Monopolies have relatively high barriers to entry. A monopoly can preserve excess profits because barriers to entry prevent competitors from entering the market. Examples: The school cafeteria or NS Power Oligopoly An oligopoly is a market form in which a market or industry is dominated by a small number of sellers. Because there are few sellers, each oligopolist is likely to be aware of the actions of the others. The decisions of one firm influence, and are influenced by, the decisions of other firms. Barriers to entry are high. In some situations, the firms may employ restrictive trade practices (collusion, market sharing etc.) to raise prices and restrict production in much the same way as a monopoly. Where there is a formal agreement for such collusion, this is known as a cartel. A primary example of such a cartel is OPEC which has a profound influence on the international price of oil. Oligopolies are typically composed of a few large firms. Each firm is so large that its actions affect market conditions. Therefore the competing firms will be aware of a firm's market actions and will respond appropriately. This means that in contemplating a market action, a firm must take into consideration the possible reactions of all competing firms and the firm's countermoves Examples: Three companies (Rogers Wireless, Bell Mobility and Telus) share over 94% of Canada's wireless market. Pure Competition Ah, the Holy Grail of western culture. perfect competition describes markets such that no participants are large enough to have the market power to set the price of a homogeneous product. Because the conditions for perfect competition are strict, there are few if any perfectly competitive mark Infinite consumers with the willingness and ability to buy the product at a certain price, and infinite producers with the willingness and ability to supply the product at a certain price. ets. Zero entry and exit barriers – It is relatively easy for a business to enter or exit in a perfectly competitive market. Perfect factor mobility - In the long run factors of production are perfectly mobile allowing free long term adjustments to changing market conditions. Perfect information - Prices and quality of products are assumed to be known to all consumers and producers Example: Soft drink beverages, pizza shops in Sack-vegas! Monopolistic Competition Monopolistic competition is a form of imperfect competition where many competing producers sell products that are differentiated from one another (that is, the products are substitutes but, because of differences such as branding, not exactly alike). There are many producers and many consumers in the market, and no business has total control over the market price. Consumers perceive that there are non-price differences among the competitors' products. There are few barriers to entry and exit. In a monopolistically competitive market, firms can behave like monopolies in the short run, including by using market power to generate profit. In the long run, however, other firms enter the market and the benefits of differentiation decrease with competition; the market becomes more like a perfectly competitive one where firms cannot gain economic profit. Examples: Computer operating systems or hair dressers. What about iPads or Blackberrys? In other words, what is the effect on you and I? Let’s think about the example of the various market structures we discussed. That should give us some clues. When not coerced legally to do otherwise, monopolies typically maximize their profit by producing fewer goods and selling them at higher prices than would be the case for perfect competition. Monoplies have great market power. That is, they can change the price at will. Prices tend to be higher in monopolies then they would be in pure competition. The case of AT&T. Oligopolies are price setters rather than price takers. Which tends to result in higher prices. Oligopolies can retain long run abnormal profits. High barriers of entry prevent sideline firms from entering market to capture excess profits. For example, an oligopoly considering a price reduction may wish to estimate the likelihood that competing firms would also lower their prices and possibly trigger a ruinous price war. Or if the firm is considering a price increase, it may want to know whether other firms will also increase prices or hold existing prices constant. In monopolistic competition, a firm takes the prices charged by its rivals as given and ignores the impact of its own prices on the prices of other firms. Producers have a degree of control over price. In general, monopolies, oligopolies and monopolistic competitions result in both higher prices and general inefficiencies.