Advanced Financial Reporting - FMT-HANU

advertisement

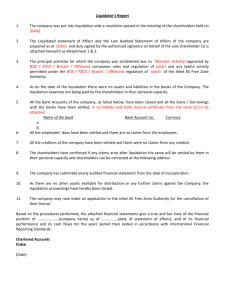

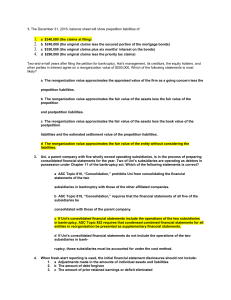

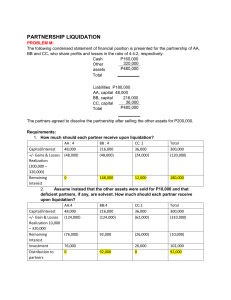

Advanced Financial Reporting FMT Week 15: Revision Foreign currency transaction • Foreign currency transactions are converted at the exchange rate ruling on the transaction date • Unhedged assets and liabilities are remeasured at each period-end at the period-end exchange rate and the resulting conversion difference is recorded below operating margin • Financial Instruments: all derivative instruments are recognized in the balance sheet at fair value. Foreign currency transaction • Derivative instruments may be designated as fair value or cash flow hedges. – Fair value hedges protect against a change in the fair value of assets and liabilities, – while cash flow hedges protect against a change in the value of future cash flows generated by existing or future assets or liabilities. – Cash flows hedge: Gains/losses are recorded as Comprehensive Income – Fair value hedge: Gains/losses are recorded on the Income Statement Foreign currency translation • Current rate method: All asset and liability balances are translated at the current exchange rate. All revenue and expense items are translated at their historical exchange rate, or at an average rate if there are multiple transactions of similar kind. The transaction adjustment is taken directly to translation adjustment in stockholders’ equity (on BS) • Temporal method: Assets and liabilities that are recorded in the accounts at historical cost are translated at their historical exchange rates. Assets and liabilities that are recorded in the accounts at current value are translated at the current exchange rate. All revenue and expense items are translated at the historical exchange rate, or at an average rate if there are multiple transactions of similar kind. The remeasurement gain or loss is taken to the income statement Foreign currency translation • The concept of functional currency • Integrated or independent subsidiary Liquidation and Reorganization • Insolvency and going concern • Voluntary (chapter 11) and Involuntary petitions (chapter 7 or chapter 11) • Classification of creditors: – Fully secured – Partially secured – Unsecured with priority – Unsecured Liquidation and Reorganization • Statement of Financial Affairs • Role of the Trustee • Statement of Realization and Liquidation Liquidation and Reorganization • Reorganization: reorganization plan • Fresh start reporting for company emerges from chapter 11 – Assets are restated to current market value – Liabilities are stated at PV of future cash pmts – RE set to zero – APIC is adjusted to balance Partnership • Partnerhip advantages and disadvantages • Alternative legal forms • Capital account: – Contribution – Profit and loss allocated – Withdrawal Partnership • Capital contribution: intangible asset using bonus and goodwill method • Allocation of income – – – – Interest on beginning balance Allocated compensation Bonus Sharing remaining income • Admission of new partner – Purchase of a current interest: BV and Goodwill method – Contribution to the partnership: Bonus and Goodwill method Partnership: Termination and liquidation • Termination of partnership: gains and losses on disposal of assets allocated to partner’s capital account according to profit sharing ratios • Schedule of Liquidation • Preliminary cash distribution: – Calculation of safe balances Partnership: Termination and liquidation • Deficit Capital balance – Contribution made – Absorption by other partners • Marshalling of Assets: raking of debts • Predistribution plan Exam Format • 2 hours exam • Closed book • Format: – 20 multiple choice – 4 short answer questions