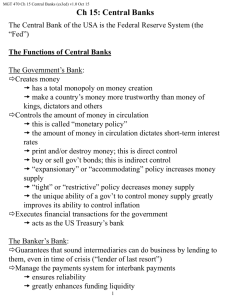

Class # 3. 26 January 2016 Why are central banks in advanced economies so fixated on raising inflation to 2%? Mario Draghi said yesterday in Frankfurt that the European Central Bank must fulfill its inflation mandate in order to maintain its credibility. Last month EZ core inflation was 0.9 percent, and headline inflation at 0.2%. . The first FOMC rate meeting of 2016 begins today. After the recent market turmoil, it would be quite surprising if the Fed announces another rate hike tomorrow. BoJ meeting on Thursday. Consumer prices, excluding fresh food and energy, rose 0.9% in November, which matches the high since the effect of the 2014 sales tax increase dropped out of the comparison. Moreover, some officials note that rents in Japan are falling, and this is more of a structural issue than one subject to monetary policy. If rents were excluded, this would push the "core" CPI a bit higher still. But a month ago the BoJ mildly expanded its QE operation with no reaction; since then the yen has risen 3.5% against the dollar, while the Nikkei 225 is down about 11.5%. Globally, at 2.4 per cent in December, core inflation has only been higher once since 2000 — in July-September 2008, when it peaked at 2.5 per cent. In the US, consumer price inflation rose to 2.1 per cent in December, its highest level since July 2012. US dollar and CB policy. IMS. Currency wars. Secular stagnation and the global savings glut. What information do government bond yields contain? S&P last year downgraded 892 issuers, representing 69 percent of all ratings actions, according to a report published on Wednesday. That’s the most since 2009, when it downgraded 1,325 issuers, or 83 percent of total actions. Downgrade potential remains under historical averages, S&P said. Based on the number of defaults in the first three quarters of the year, S&P expects 109 defaults by year-end, the largest total since 268 borrowers ran into problems in 2009. There were only 60 defaults worldwide in 2014. Last week it was reported that China's economy grew 6.8 percent in the fourth quarter from the same period of 2014. That left full-year growth at 6.9 percent, the least since 1990. ITALY STORY: Fear of bank bail-in in Italy. Currently attention is focused on the world’s oldest bank, Banca Monte Dei Paschi Di Siena (BMPS). After it failed the ECB’s 2014 Asset Quality Review, BMPS won regulatory approval for a proposed restructuring. But although the bank successfully raised €3bn in new capital with a May 2015 share issue, it has since failed to find either a merger partner or buyers for more than a handful of its €42bn in bad loans—a bad debt pile equal to 31% of its total loan book. As a result, the bank’s share price has continued to slide, falling -66% since its May rights offering. One difficulty is that the Italian government has struggled to come up with a plan that would allow Italian banks to dispose of the €350bn in non-performing loans sitting on their balance sheets—a sum which equates to a sector-wide NPL ratio of some 18%. In an attempt to speed up the resolution of insolvency cases, last August Rome overhauled credit recovery procedures and passed reforms making loan write-downs and write-offs tax deductible. However, these measures were not enough to kick-start a secondary market for impaired debt. To solve the problem, the Bank of Italy is calling for the establishment of a special purpose asset management company, or “bad bank”, to purchase and recover or dispose of non-performing loans under market conditions. However, new EU banking regulations under the Bank Recovery and Resolution Directive have hampered Italy’s plans. Under the new rules, which were partially introduced in Italy last year, the shareholders and creditors of a failing bank must be bailed-in in an attempt to absorb losses and recapitalize the bank before any state funds can be used to mount a bail-out. Shareholders and junior bond-holders are hit first, followed by senior bond-holders and depositors with balances over €100,000. The aim is to protect tax-payers from bearing the cost of a bank crisis. But much of the junior debt issued by Italian banks is owned by retail investors, who in recent years were encouraged to buy the debt instead of leaving their cash on deposit (“Of course the investment is safe. This bank has been here for over five hundred years!”). As a result, Italian retail investors now find themselves directly in the firing line. According to a Bruegel think tank report, bank bonds make up as much as 40% of Italian household bond portfolios. However, this number is now falling fast as retail investors wake up to the risks they face. The alarm was sounded in July last year, when Banca Romagna Cooperative (BRC) was forced to bail-in shareholders and junior bond holders after the new rules prevented the government from following its initial plan of using funds from Italy’s Deposit Guarantee Insurance Fund to recapitalize the bank. As a small mutual bank, all of BRC’s equity and junior debt was held by retail investors, who consequently bore the entire cost. Then in November another four small banks where hurriedly restructured before the new regulations came fully into force at the end of year, which could have seen depositors also bailed-in. The Italian bank resolution fund paid €3.6bn to restructure the four, with €1.65bn used to write down the value of their bad debts and move them into a separate bad bank. The remaining €1.75bn went to boost the banks’ capital adequacy ratios, before the Bank of Italy put them up for sale earlier this week. Officially no public funds have been used, but this is a moot point because the resolution fund is financed by loans from Italy’s biggest banks which are supposed to be paid back when assets held by the fund are sold off. However, the loans are guaranteed by the state bank Cassa Depositi e Prestiti, which will have to pay up to €1.65bn to the big banks if the restructured institutions cannot be sold at book value within 18 months or if recoveries from the bad assets are worse than expected. The restructuring of the four banks attracted adverse public attention not just because the government rushed it through, but also because one junior bondholder—an elderly retail investor—committed suicide when he learnt of the financial losses he would be forced to take. Coming on top of the earlier losses born by BRC bond-holders, news of the investor’s death triggered a wave of criticism directed at the EU–imposed rules and the way Renzi’s government has handled Italy’s bank restructuring. It’s not entirely clear what will happen in the near term, but the financial markets are already pushed to extremes by central-bank induced speculation. With speculators massively short the now steeply-depressed euro and yen, with equity margin debt still near record levels in a market valued at more than double its pre-bubble norms on historically reliable measures, and with several major European banks running at gross leverage ratios comparable to those of Bear Stearns and Lehman before the 2008 crisis, we're seeing an abundance of what we call "leveraged mismatches" - a preponderance oneway bets, using borrowed money, that permeates the entire financial system. With market internals and credit spreads behaving badly, while Treasury yields, oil and industrial commodity prices slide in a manner consistent with abrupt weakening in global economic activity, it is rather ominous. So how do we get out of this slow growth, over-indebted liquidity trap? To do that, we need to understand how we fell into it. Why, in 2008, did private spending collapse way below private income, not just in the US but in most of the OECD? It’s important to note that what happened 8 years ago was not what economists expected. Rather we expected: the unsustainable disequilibrium, or Larry Summers’ “balance of financial terror” but we got a different kind of crisis… Recall WEO in Davos in February 2005: the issue was only one of “soft” landing vs. “hard” landing but it didn’t crash or even start to adjust. The economics profession is, in my view, has made no progress since then. In my view, a big part of the answer is that a series of bubbles helped keep the world economy driving forward over the past three decades. Behind these, however, lay a credit super-bubble, which burst in 2008. This is why private spending imploded and fiscal deficits exploded. Some of the most famous economists in the world such as Stiglitz, Summers, Krugman, Rogoff, William White, take divergent views. And the IMF, BIS, OECD. Bretton Woods 2, as it evolved, hinged both on the willingness of foreign central banks to take the currency risk associated with lending to the US at low interest rates in dollars despite the United States large current account deficit AND the willingness of private financial intermediaries to take the credit risk associated with lending at low interest rates to highly-indebted US households. The second leg of the chain collapsed before the first. And its collapse has delivered a nasty shock to everyone – including the countries that supply the US with financing. US financial institutions were neither willing nor able to take on the risk of lending more to US households. For a while the US government was able to ramp up its lending to households (notably through the Agencies) and in the process effectively take over the function previously performed by the private financial system, but it has not avoided a sharp fall in the overall availability of credit. In retrospect, the fact that (reported) bank profits didn’t fall as the Fed raised rates in 2005-6 should have been a clue that risks were building. An inverted yield curve isn’t good for institutions that borrow short and lend long – but it initially didn’t seem to have an impact on financial sector profitability. It is now clear how the financial sector kept profits up: it took on more risk, as it shifted from borrowing short to buy safe long-term assets (Treasuries and Agencies) to borrowing short to buy risky longterm assets. Leverage in the system also increased (and for some broker dealers that seems to be an understatement), as more and more financial institutions believed that the US had entered into an era of little macroeconomic or financial volatility [“great moderation”]. The net result seems to have been a truly explosive concentration of risk in the hands of a core set of financial intermediaries in the US and Europe. Securitization – it seems – actually didn’t disperse risk into the hands of institutions able to handle it. Shadow banking issues. Many have highlighted the role that loose US monetary policy played in supporting the housing boom. And there is no doubt much truth in this story: pushing rates down to help “clean” up the bursting of the dot.com bubble and holding them down for several years certainly helped induce the rise in home prices and the housing boom. At the same time, this story leaves out what to me is a crucial part of the story: the housing boom didn’t end when the Fed reversed course and raised long-term rates. The really risky loans were made in late 2005, 2006 and early 2007 – after policy rates had increased. Private institutions kept on lending – in part because they decided that it was safe, in a world of low assumed macroeconomic volatility – to take on more leverage and more credit risk to keep profits up. Foreign central banks that kept on lending to the US despite large ongoing deficits – and poor returns, after taking into account the currency risk – on their dollars contributed too. If they had scaled back their financing more rapidly, the US would have been forced to adjust sooner – reducing the risk of the kind of severe crisis that began in 2008. There is still a real risk that the continuing adjustment won’t be gradual. And it certainly looks like the flow of Chinese (and Gulf) savings to US households [and to Europe] over the past few years has produced one of the largest misallocations of global capital in recent history. The US [and European] taxpayers are getting hit with the costs for much of the credit risk that supported the big increase in household consumption – as the FT’s Martin Wolf quipped, what looked to be private lending turned out to be public spending. And China’s taxpayers will get eventually have to pick up the bill for the currency risk associated with lending to the US in dollars and Europe in euros at low rates … This is again not the crisis that we all expected. And in terms of outcomes, one key difference has been that we thought the collapse of the balance of financial terror would push Treasury yields up. The credit crisis has pushed Treasury yields down. The BIS staff in Basel noted at the end of last year that globally, interest rates have been extraordinarily low for an exceptionally long time, in nominal and inflation-adjusted terms, against any benchmark. Such low rates are the most remarkable symptom of a broader malaise in the global economy: the economic expansion is unbalanced, debt burdens and financial risks are still too high, productivity growth too low, and the room for manoeuvre in macroeconomic policy too limited. The unthinkable risks becoming routine and being perceived as the new normal. Accommodative monetary policies continued to lift prices in global asset markets in the past year, while diverging expectations about Federal Reserve and ECB policies sent the dollar and the euro in opposite directions. As the dollar soared, oil prices fell sharply, reflecting a mix of expected production and consumption, attitudes to risk and financing conditions. Bond yields in advanced economies continued to fall throughout much of the period under review and bond markets entered uncharted territory as nominal bond yields fell below zero in many markets. Plummeting oil prices and a surging US dollar shaped global activity in the year under review. These large changes in key markets caught economies at different stages of their business and financial cycles. The business cycle upswing in the advanced economies continued and growth returned to several of the crisis-hit economies in the euro area. At the same time, financial downswings are bottoming out in some of the economies hardest-hit by the Great Financial Crisis. But the resource misallocations stemming from the pre-crisis financial boom continue to hold back productivity growth. Monetary policy continued to be exceptionally accommodative, with many authorities easing or delaying tightening. For some central banks, the ultra-low policy rate environment was reinforced with large-scale asset purchase programmes. In the major advanced economies, central banks pursued significantly divergent policy trajectories, but all remained concerned about the dangers of inflation running well below inflation objectives. In most other economies, inflation rates deviated from targets, being surprisingly low for some and high for others. The suitable design of international monetary and financial arrangements for the global economy is a long-standing issue. A key shortcoming of the existing system is that it tends to heighten the risk of financial imbalances, leading to booms and busts in credit and asset prices with serious macroeconomic consequences. These imbalances often occur simultaneously across countries, deriving strength from international spillovers of various types. The global use of the dollar and the euro allows monetary conditions to affect borrowers well beyond the respective issuing economies. Risks in the financial system have evolved against the backdrop of persistently low interest rates in advanced economies. Despite substantial efforts to strengthen their capital and liquidity positions, advanced economy banks still face market scepticism. As a result, they have lost some of their traditional funding advantage relative to potential customers. This adds to the challenges stemming from the gradual erosion of interest income and banks' growing exposure to interest rate risk, which could weaken their resilience in the future. Ritholtz Succinct Summations for the week ending January 22 nd, 2016 Positives: 1. After three straight weeks of selling, stocks get a reprieve, finishing positive on the week. 2. Existing home sales came in at a 5.46mm annualized rate, up 14.7% m/o/m. 3. MBA mortgage applications composite rose 9% w/o/w. 4. Bloomberg’s consumer comfort index came in at 44, down just slightly despite the lousy January for stocks. 5. Manufacturing PMI came in at 52.7, up from 51.3 previously. Negatives: 1. CPI still not budging, -0.1% m/o/m, core CPI rose 0.1%. 2. Housing starts came in at an annualized 1.149mm rate in December, down 2.5% from the previous reading. 3. Jobless claims rose came in at 293k, the 4-week moving average is up to 285k, from 278.5k previously. 4. Housing permits fell to 1.232mm SAAR, a 3.9% m/o/m decline.

0

0

advertisement

Related documents

Download

advertisement

Add this document to collection(s)

You can add this document to your study collection(s)

Sign in Available only to authorized usersAdd this document to saved

You can add this document to your saved list

Sign in Available only to authorized users