The EU Financial Crisis and the Middle East

advertisement

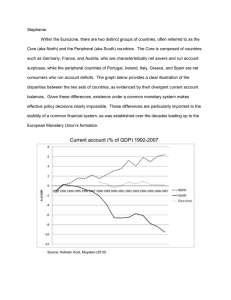

The EU Financial Crisis and the Middle East Don’t bother? Dr. Rolf Freier FNF Jerusalem May 2012 Ludwig von Mises Austrian Liberal Economist 1881 – 1973 „...the housewife is the only rational economic being, she usually does not spend more than she has got...“ The Debt Champions 2010 Public debts in billion € What constitutes financial crisis is not just debt alone: • • • • • • • • Lack of restraint Lack of regulation Easy money Private debt Public debt Lack of trust of lenders Lack of credit for business Lack of growth watch: The Crisis of Credit, splendid video animation under http://vimeo.com/3261363 The Eurozone and the Debt Crisis EU Countries International Credit Ratings both in % of GDP Budget deficits Public debts Returns on state bonds 10 years in % GDP since pre-crisis 2008 = 100% Economic growth in Germany GDP change in % Elements of the Euro Debt Crisis • Bank crisis (debts, high risk assets, bank interdependence) • Public debts (national and foreign debts) • Private debts • Real estate bubble (Spain) • EU Target accounts ‘pre-finance’ balance of payment deficits • Trade imbalances • ECB: indirect state financing (state bond buying) • Governance deficiencies • Cultural incompatibilities (institutions & preferences) ? Four Scenarios Scenario 1 EU manages crisis • Euro Zone remains as it is • Fiscal pact and austerity work (Maastricht criteria: budget deficit <3%, Sovereign debt <60% GDP • Markets regain trust • Euro Zone stabilises • Continuing reform efforts Scenario 1 Probability • Fiscal Pact not yet ratified • Elections dooming, politicians want to be reelected • It needs a change in governments/voters attitudes • Austerity without growth measures a painful long-term cure without success guaranteed? Scenario 2 EU introduces Eurobonds • Countries do not (re)finance debt by national bonds but through collective bonds (no ECEP) • Harmonizing effect on interests to be paid by successful and less successful economies • Structural imbalances could grow long term (no reform discipline enforced on crisis countries) Scenario 2 Probability • Eurobonds violate existing EU-law (no bailout) • Germany still resists, would have to foot the bill • To maintain reform pressure on PIGSF need to advance with controversial ECEP • Higher probability of so called ‚project bonds‘ intended to spur growth in EU countries (highly problematic because of its focus on infrastructure) Scenario 3 ECEP • • • • • • Eurozone becomes political union Eurozone becomes fiscal union Harmonizing tax systems Harmonizing social security Union issues Eurobonds Eurozone could stabilise and Euro probably appreciate Scenario 3 Probability • • • • Differences in political culture Differences in social policies Differences in savings Differences in political and economic weight and size • Differences in preferences? • Long term goal or European pipe dream? Scenario 4 Eurozone Breaking • • • • • • • Individual PIGS countries departing from Eurozone Northern core Eurozone? Loss of credits and guarantees Capital flight International containment possible? Bank and state insolvencies Monetary renationalisation = political renationalisation? • Europe fractious and inward looking? Scenario 4 Probabiliy • • • • Possible but not high probability Risk of 20% or higher??? Eurozone fragmenting or only weakest go? Greek could go and the rest gets the act together?? • Should Germany foot the big bill to keep everybody happy and going???? Why bother, nothing to loose for the Middle East? Israel Budget 2013 ?? • Increases in government outlays 2011: 18 Billion NIS 2012: 15 Billion NIS Needs > 6% growth to be accommodated Growth currently 3% Balance of payment negative Sovereign debt currently 72% of GDP EU Programmes incl. MENA • • • • • • • ECFR FRIDE (EU Democracy/ Human Rights) Tempus (Higher education) Middle East watch E-Mail service Pegase (Palestine socio-economic) ENPI (refugees) PfP Last but not least The European Unions Role in the Middle East Quartet dealing with the conflict