Duty of Loyalty

advertisement

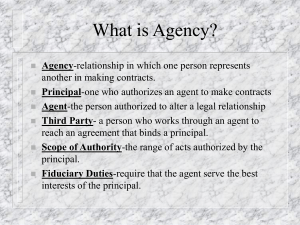

An Overview of Fiduciary Duties Ron A. Rhoades, JD, CFP® Chief Compliance Officer, Director of Research Joseph Capital Management, LLC Hernando, Florida Alpharetta, Georgia Durham, North Carolina August 3, 2009 NASAA INVESTMENT ADIVISER CONFERENCE 1 A Necessary Disclosure The views expressed herein are those of the speaker only, and do not (necessarily) represent the views of: 1. NASAA; 2. any organization to which the speaker belongs; or 3. my mother. 2 Today … The 3 Main Fiduciary Duties: FIDUCIARY Where Do They Come From? What Are They? What Do They Require? How Does An Investment Adviser “Add Value”? Case Study Discussion Questions (and an occasional answer) 3 The ATTORNEY … and the ANGEL 4 iduciary duties: What Are They? “To Act In The Best Interests of the Client” "This is a simple statement to make, but one that is more difficult to apply.” - Lori Richards, Director, SEC’s OCIE, Feb. 27, 2006 “I believe that it is important that the Commission explain what a fiduciary standard requires.” - Elisse Walter, SEC Commissioner, May 5, 2009 5 iduciary duties: What Are They? Where Do They Come From? 1. Due Care Federal Advisers Act 2. Utmost Good Faith State Securities Acts 3. Loyalty Common Law 6 Duty of Due Care PRUDENCE An investment adviser in providing investment and financial advice shall exercise such care and skill as a prudent investment adviser would exercise in dealing with his or her own financial affairs. Prudence, one of the four Cardinal Virtues from classical and religious texts, is depicted in Simon Vouet’s Allegory of Prudence 7 Duty of Due Care KNOWLEDGE & SKILL The investment adviser is under a duty to utilize the “care, knowledge and skill ordinarily possessed and exercised in similar situations by the average member of the profession” Erlich v. First Nat. Bank of Princeton, 505 A.2d 220 (N.J.Super.L., 1984) For investment advice, knowledge of ??? 8 Duty of Due Care PROCEDURAL DUE CARE Did the adviser follow a good process in providing investment or financial advice to her or his clients? 9 Duty of Due Care SUBSTANTIVE DUE CARE When called upon to do so, did the adviser exercise good judgment? 10 Duty of Due Care: A HOT BUTTON DILIGENCE Was the adviser diligent in … Understanding the needs of the client; and In reviewing both the suitability and soundness of the investment products recommended In the development of the investment strategy 11 Duty of Due Care CONFIDENTIALITY There exists a duty of due care in handling client’s personal information. 12 Duty of Utmost Good Faith “most abundant good faith” “absolute and perfect candor or openness and honesty” “the absence of any concealment or deception, however slight” “NO reckless behavior” 13 Duty of Utmost Good Faith Did the adviser believe that : (1) any statements or representations made to your client are completely truthful? (2) your conduct is within the realm of decent and appropriate behavior of a professional? (3) Your actions are in the best interests of your client? YOUR GOOD FAITH WILL BE TESTED BY OTHERS, PUTTING THEMSELVES IN THE ADVISER’S SHOES, NOT MERELY BY THE ADVISER’S OWN PERCEPTION. 14 Duty of Loyalty … No Conflict Rule No Profit Rule Undivided Loyalty Rule 15 Duty of Loyalty The “NO CONFLICT” rule “A fiduciary must not place herself, himself, or itself in a position where its own interests conflict with those of its client.” 16 Duty of Loyalty The “NO PROFIT” rule “A fiduciary must not profit from her, his, or its position at the expense of the client.” 17 Duty of Loyalty Reasonable compensation – fully disclosed in advance and agreed to by the client – is permitted Under GENERAL FIDUCIARY LAW, there is no restriction on the form of compensation (AUM, commissions, fixed fees, hourly fees, combinations thereof, etc.) 18 Duty of Loyalty The “UNDIVIDED LOYALTY” rule A fiduciary owes undivided loyalty to each of her, his, or its clients. The fiduciary should avoid placing the interests of one client ahead of another client. 19 Duty of Undivided Loyalty How Did The Adviser Address … Allocations of IPOs, etc.? Rebalancing during market downturn? Taking on more clients? “Outside activities” (CPA, attorney, real estate, etc.) 20 “No Conflict” and “No Profit” Rules: Disclosure and Consent Fiduciary law protects the client by requiring … Disclosure of all material facts The client’s intelligent, independent, informed consent Each transaction be a substantively fair arrangement The fiduciary to act in good faith 21 Your Disclosure Obligation What is a MATERIAL FACT? Anything Which Might Affect the Client’s Decision Whether or How to Act 22 Duty to Disclose Material Facts No “half-truths” No omissions of material facts 23 Duty to Disclose Material Facts If the adviser does not have the information needed – he or she should obtain it The Adviser (not the client) have the duty to investigate to determine all material facts The Adviser must disclose all material facts which might be reasonably discovered 24 Duty to Disclose Material Facts “Readiness and willingness to disclosure are not equivalent to disclosure.” DISCLOSURE MUST BE AFFIRMATIVELY MADE The client’s duty to “discover” facts is reduced when being advised by a fiduciary. See Wolf v. Brungardt, 215 Kan. 272, 524 P.2d 726 (Kan., 1974) 25 Duty to Disclose Material Facts Does Providing “Access” = “Delivery” of Material Facts? Example: “See our web site for additional information” Example: “See the prospectus for additional information” But – delivery by custodian after purchase? Example: Furnishing ADV, Part II 26 No “Casual Disclosures” Permitted Examples of “casual disclosure” … “There may be other facts which may be of interest to you” “I may possess a conflict of interest.” 27 “Full Disclosure” or “Casual Disclosure” ? “My affiliated broker-dealer may receive 12b-1 fees, payment for shelf space, and soft dollar compensation from mutual fund companies.” 28 The Disclosure Obligation Disclosures Must Be Clear and Understandable The less the client’s sophistication, the greater the disclosure (a more extensive explanation is required) 29 The Disclosure Obligation RELATIVELY SOPHISTICATED …. NOW 30 The Disclosure Obligation What about clients with diminished capacity? How do you obtain INFORMED CONSENT? 31 The Disclosure Obligation The duty to ensure understanding rests first and foremost on the investment adviser But - what about the “duty to read” a customer normally possesses? “The failure to read a contract may be excusable where a fiduciary or confidential relationship exists between the parties” Lin v. John Hancock (2007) (Client trust and reliance upon representations made may excuse a client’s duty to read.) 32 The Disclosure Obligation A client who relies upon expert advice, instead of reading disclosures, is entitled to rely upon that expert advice. Duty to read excused when client “accustomed to signing documents at the (advisor’s) request without reading the documents” Strotz v. Dean Witter (Calif., 1990) 33 33 The Disclosure Obligation Disclosures Must Be Timely Made The client must know all the material facts before he or she is required to provide consent to the transaction or course of action 34 What Is Required to Be Disclosed? All fees paid in connection with … Fees paid for your advisory services By the client Any MATERIAL third-party compensation Custodial services Termination fees which might be applied Your receipt of benefits from custodians 35 What Is Required to Be Disclosed? Investment products: Disclosed Hidden Fees and Costs Fees and Costs See “Estimating the Total Costs of Stock Mutual Funds” 36 What Is Required to Be Disclosed? What About The Tax Ramifications Of Investment Decisions? 37 Is a “Conflict of Interest” Always a “Material Fact”? 38 Is a “Conflict of Interest” always a “Material Fact”? YES. (Nearly) Always. (if the conflict of interest is “material”) Example of “nonmaterial” conflict: 39 Must the adviser disclose conflicts of interest which the adviser cannot avoid? 40 YES. Unavoidable conflicts of interest are still conflicts! 41 Examples of Unavoidable Conflicts: Client asks: “Should I pay down my mortgage or invest my cash with you?” Client desires advice on whether to purchase a lifetime annuity, instead of investing additional cash with adviser. “How much money should I give to my kids this year?” 42 Conflicts of Interest and Compensation Your Method, Amount of Compensation Certain business affiliations or arrangements Any receipt of third-party compensation Ex: commissions received on sale of product Ex: custodial platform services (TD Ameritrade, Schwab, Fidelity, Trust Company of America, etc.) Ex: attending educational events (custodian, fund-sponsored) Ex: receipt of non-de minimus gifts from custodians and others Ex: “proprietary products” of your firm or an affiliate Any commitment made to custodian (min. AUM) Many others … 43 Is disclosure of a conflict of interest sufficient to meet the adviser’s fiduciary duty of loyalty? What is the PURPOSE of Disclosure? 44 The Purpose of Disclosure is to … Obtain a Client’s Consent 45 The Purpose of Disclosure is to … Obtain a Client’s INFORMED Consent 46 “Disclosure by the adviser and the informed consent of the client, based on full and fair disclosure, is at the heart of the Adviser's Act.” - Lori Richards, Director, SEC Office of Compliance Inspections and Examinations, March 12, 2009 47 “Ex-Fidelity brokers claim sales pressure” – InvestmentNews, 4/3/2009 Sale of higher-margin separate account management products And sale of higher-cost insurance products Instead of lower-cost mutual funds 48 Not Present if …. 1. Any material fact is not disclosed 2. Lack of understanding by facts by the client 3. Use of fiduciary’s position to induce client consent 4. Transaction was not in all respects fair and reasonable 49 Will Informed Consent Exist If … 1. A conflict of interest exists 2. Disclosure of all material 3. facts exists BUT - the best interests of the client are NOT kept paramount? 50 How to Disclose … Form ADV, Part II SEC Release IA-2711 (March 2008) www.sec.gov Proposed Rule, new Form ADV, Part 2 Recommendation: Investment advisers may desire to go ahead and implement the new Part 2, and furnish the new Part 2 – with enhanced disclosures - to all existing clients, with a cover letter highlighting the sections which discuss conflicts Even though the rule has not been finalized 51 How to Disclose … Is Form ADV, Part II, the Only Disclosure Required? “Delivering a [Form ADV Part II] brochure …. does not relieve you of any other disclosure obligations you have to your advisory clients or prospective clients under any federal or state laws or regulations.” 52 How to Disclose … Client Services (Fee) agreement Ex: Your compensation Ex: Other fees and costs client may bear (if known at the time) Ex: Non-exclusive relationship Ex: What the adviser is responsible for; What the client is responsible for 53 Some Closing Thoughts … Fiduciary duties of an investment adviser lead to specific requirements imposed by regulation: IA Code of Ethics IA Compliance Supervisory Procedures Chief Compliance Officer (Trained) Business Succession Plan Disaster Recovery Plan Form ADV, Part II disclosures … and more 54 Some Closing Thoughts … Fiduciary duties of an investment adviser lead to other specific requirements NOT EXPRESSLY FOUND IN REGULATIONS 55 Suggested Action Steps – For Advisers (and Examiners) 1. Read the case - SEC vs. Capital Gains Research Bureau 2. Read the handout (book excerpts) on fiduciary duties, generally, and the fiduciary duty of loyalty 3. Review carefully SEC Release IA-2711 (Form ADV, Part 2) (www.sec.gov / Proposed Rules / March 3, 2008) 4. Study SEC and/or State Securities Regulations 5. Attend seminars to keep abreast in developments affecting fiduciary duties 56 Suggested Action Steps 6. Indentify Core Competencies Needed - Investment Advice 7. Obtain core knowledge and skills (or outsource) EXAMINERS TOO!!! 8. Maintain and enhance skills (ongoing reading, education) 57 Suggested Action Steps 9. Learn more about FIDUCIARY DUTIES 10. EXAMINERS: THINK OUTSIDE THE BOX: ARE YOU EXAMINING COMPLIANCE BY AN ADVISER WITH ALL OF THEIR FIDUCIARY DUTIES? HOW CAN YOU GET TRAINING TO INVESTMENT ADVISERS SO THEY MAY BETTER ADHERE TO THEIR FIDUCIARY DUTIES? 58 He’s an investment adviser. Ron A. Rhoades, JD, CFP® 59 He’s an investment adviser. Ron A. Rhoades, JD, CFP® 60 He’s an investment adviser. Ron A. Rhoades, JD, CFP® 61 Discussions: How Do Investment Advisers “Add Value”? Case Study Q&A 62

![Literature Option [doc] - Department of French and Italian](http://s3.studylib.net/store/data/006916848_1-f8194c2266edb737cddebfb8fa0250f1-300x300.png)