INTERMEDIATE

ACCOUNTING

Sixth Canadian Edition

KIESO, WEYGANDT, WARFIELD, IRVINE, SILVESTER, YOUNG, WIECEK

Prepared by

Gabriela H. Schneider, CMA; Grant MacEwan College

CHAPTER

18

Dilutive Securities and

Earnings Per Share

Learning Objectives

1. Describe the accounting for issuance,

conversion, and retirement of convertible

securities.

2. Explain the accounting for convertible

preferred shares.

3. Contrast the accounting for stock warrants

and stock warrants issued with other

securities.

Learning Objectives

4. Describe the accounting for stock

compensation plans under GAAP.

5. Explain the controversy involving stock

compensation plans.

6. Calculate earnings per share in a simple

capital structure.

7. Calculate earnings per share in a complex

capital structure.

Dilutive Securities and

Earnings Per Share

Dilutive Securities and

Compensation Plans

Convertible debt

Convertible preferred shares

Stock warrants

Stock compensation plans

Disclosure

Computing

Earnings per share

Simple capital

structure

Complex capital

structure

Dilutive Securities

• Instrument entitling holder to obtain

common shares

• When exercised cause existing

shareholder interest to dilute

• Ownership interest (percentage) impact

• Impact on EPS

• A.k.a. potential common shares

Convertible Debt

• Bonds that are convertible to other forms of

securities (e.g. common shares) during a

specified period of time

• Combines the benefits of a bond (interest

payments, principal repayment) with the

privilege of exchanging the bond for shares at

the bondholders option

• Once the bond is converted, all interest

payments and principal are no longer payable

Convertible Debt

•

Issued for two main reasons

1. Corporation can raise equity capital without

giving up ownership control

2. It can also achieve equity financing at a lower

cost

•

•

Conversion feature allows the corporation to offer

the bond issue at a lower coupon or stated rate

Conversion feature provides investor with an

opportunity to own equity. This feature generally

results in the investor accepting a lower coupon

rate than they would with non-convertible debt

Convertible Debt –

Accounting Issues

•

The reporting of convertible debt and

the conversion feature result in three

issues:

1. Reporting at the time of issuance

2. Reporting at the time of conversion

3. Reporting at the time of retirement

Reporting at the

Time of Issuance

• On issue date, part of the proceeds are

allocated to liability and part to equity

• This reflects the nature of the security –

since a convertible debt is part liability

and part equity

• The amounts allocated to liability and

equity are determined by using either:

• The Incremental Method

• The Proportional Method

The Incremental Method

• The value of the most easily measured

component is determined and allocated

to that component

• Debt generally the easier component to

value

• Remainder of the proceeds become the

value of the other component

The Incremental Method Example

Given:

$20,000,000 par value, 10% convertible bonds

issued at 99

If the bonds were not convertible, it is

estimated they would have been sold at 95

Bond issue costs were $70,000

What portion of the proceeds are allocated to Bond

Liability, and what portion to equity?

The Incremental Method Example

Total proceeds for the bond issue

($20,000,000 * .99)

=

$19,800,000

conversion option ($20,000,000 * .95) =

$19,000,000

Residual allocated to option

$

Fair value of the liability without the

Cash

Discount on Bond

Bonds Payable

=

800,000

19,800,000

1,000,000

20,000,000

Contributed Surplus – Stock Options

800,000

The Proportional Method

• When values for both the liability and

equity components are known or

determinable

• The Bond Discount (or Premium)

becomes a calculated amount under the

Proportional Method

The Proportional Method

Given:

• $10,000,000 of 8% convertible debentures due

in 20 years issued for $10,800,000

• Market value of the company’s common shares

(on issue date) $80 per share

• Present value of bonds at time of issuance was

$8,500,000

• Corporation believed the difference between

the present value and the amount paid was

attributable to the conversion feature

The Proportional Method

Present value (fair value) of the bonds

$8,500,000

Fair value of conversion rights

(10,800,000 – 8,500,000)

Cash

$2,300,000

10,800,000

Discount on Bonds Payable

Bonds Payable

Contributed Surplus

1,500,000

10,000,000

2,300,000

Note that in this case we are clearly given the fair

values for both the liability and the conversion feature

Reporting at Time of Conversion

• Main issue is determining the amount at

which to record the securities which are

being exchanged

• Two approaches available

• Market value approach

• Gain or loss on conversion can occur

• Book value approach

• Gain or loss on conversion does not occur

• Most common approach

• Either method acceptable under GAAP

Book Value Approach

• When market price of bonds or shares not

known

• Book Value of the bonds and conversion rights used

to record the conversion

• The basis for this method is that a “swap” or

exchange of security has taken place

• The values were established when the bonds

were originally issued and therefore should not

be changed, as there was a contract in place

Induced Conversion

• When the corporation wants to entice

or induce the bondholders to convert

their bonds into shares

• Additional consideration – the

“sweetener” – offered to the

bondholders to convert (cash, common

shares, etc.)

• The inducement is recorded as an

expense in the period of conversion

Reporting at the

Time of Retirement

• Treated the same as debt retirement

from Chapter 15

• Clear any outstanding premiums,

discounts, bond issue costs, interest

accrued to bondholders

• The conversion rights account must be

reallocated

• Equity components remains in Contributed

Surplus

Convertible Preferred Shares

• Convertible preferred shares are considered

equity

• Convertible debt considered liability and equity

• At the time of issuance no allocation between

debt and equity components

• Exception is redeemable preferred shares

• When conversion occurs the book value

method is always used

• Deemed the exchange of one equity for another

equity instrument

Stock Warrants

• Entitle the (share)holder to acquire shares

at a specified price, within a specified

period of time

• Attached to senior securities (bonds,

preferred shares)

• Difference between convertibles and

warrants

• With warrants the holder must pay an

amount of money in order to acquire the

shares

Stock Warrants

•

Warrants (options to purchase additional

shares) occur under three scenarios

1. To make the original security more

attractive to the investor

2. To provide evidence of the pre-emptive

right to acquire more common shares

3. Used as compensation for executives and

employees

Stock Warrants

• “Rights” are similar to warrants except that

rights have a shorter lifespan and are

attached only to common shares, in order to

purchase more common shares

• No journal entry required when rights are issued

• Use either the proportional or incremental

method of accounting when dealing with

detachable stock warrants

• If warrants are non-detachable, no allocation

to warrants is needed

Stock Compensation Plans

•

•

•

A form of stock warrant — a stock option

Provides the employee with an opportunity to

purchase shares at a given price, within a

specified period of time

Two accounting issues associated with stock

compensation plans

1. Determination of compensation expense

2. Periods of allocation for compensation expense

amounts

Stock Options - Important Dates

Work

start date

Grant

date

Vesting

date

Exercise

date

Expiration

date

Options

are

granted to

employee

Date that

employee

can first

exercise

options

Employee

exercises

options

Unexercised

options

expire

Compensation Cost

Measurement

•

Two available methods

1. Intrinsic Value Method

•

•

Excess of market price over exercise price at grant date

Requires expanded note disclosure

– Pro-forma net income and EPS under fair value

method

2. Fair Value Method

•

•

•

Measured at fair value of the stock options granted

Preferred method of measurement

Either method acceptable under GAAP, based

on newly developed and accepted standard

The Measurement Date

Compensation expense is determined as of

Measurement date (usually the grant date)

Measurement date

is:

Grant date - if both the

number of shares offered

and option price are known

Exercise date - if facts

depend on events after

grant date

Options: Allocating

Compensation Expense

Compensation Expense

is determined as of the

measurement date

and is allocated over

the service period

• The service period is the period benefited by

employee’s service

• It is usually the period between the grant date

and the vesting date

Compensation Expense - Example

Given:

5 Stock options granted January 1, 2001

Option to purchase:

2,000 shares each

Option price per share:

$60.00

Market price per share:

$70.00 (at grant date)

Stock option expires:

10 years

Service period:

2 years

Intrinsic Value Method:

Market value at grant date (5*2,000)*$70 = $700,000

Option price at grant date (5*2,000)*$60 = 600,000

Compensation expense

$100,000

Fair Value Method:

Expense calculated by applying an option pricing model

Compensation Expense – Example:

Journal Entries

Intrinsic Value

Fair Value

Grant Date

No Entry

December 31, 2001

Compensation Expense

50,000

Contributed Surplus–Stock Options

50,000

(100,000 2 years) // (220,000 2 years)

December 31, 2002

Compensation Expense

50,000

Contributed Surplus–Stock Options

50,000

No Entry

110,000

110,000

110,000

110,000

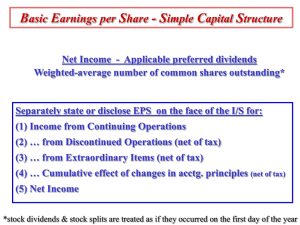

EPS - Simple Capital Structure

Net Income – Preferred Dividends

Weighted Average # of Shares Outstanding

• If the preferred shares are non-cumulative

• include only declared dividends

• If the preferred shares are cumulative

• include only declared dividends, or

• if no dividends declared, include only one

year’s dividends

EPS - Simple Capital Structure

• Weighted average number of common

shares outstanding

• To find the equivalent number of whole shares

outstanding for the year

• Stock splits and stock dividends require

restatement of the outstanding number of

shares from the beginning of the year

• Because there has been no change in the

company’s assets, or in the shareholders’ total

investment

EPS - Simple Capital Structure

• A final note (CICA Handbook, Section 3500)

• If there is a stock split or stock dividend

after the year end but before the

publication of the financial statements

• The weighted average number of shares

outstanding must be restated

• This applies to the current year, as well as

previous years if comparative statements are

issued

EPS Calculation Simple Capital Structure

Given:

January 1:

March 1:

June 1:

500,000 shares outstanding

Issued 20,000 shares

50% Stock dividend (60,000

November 1:

December 31:

Issued 30,000 shares

Ending Balance = 210,000

shares outstanding

additional shares issued)

Determine the weighted average number of shares

outstanding.

EPS Calculation Simple Capital Structure

Dates

O/S

Shares

O/S

Restatement

Fraction

of Year

Weighted

Shares

Jan-Mar 100,000 x

1.50

x

2/12 =

25,000

Mar-Jun 120,000 x

1.50

x

3/12 =

45,000

Jun-Nov 180,000

x

5/12 =

75,000

Nov-Dec 210,000

x

2/12 =

35,000

Weighted average shares outstanding

180,000

Complex Capital Structure

• Complex capital structure:

• When corporation has convertible securities, options,

warrants or other rights, and

• When converted these could dilute EPS

• Dilution is the reduction in EPS, if:

• securities, potentially convertible into common stock,

are converted [assumed at beginning of the year]

• Anti-dilutive securities

• Securities, when converted, increase EPS

• Anti-dilutive EPS are not reported, only basic EPS

EPS - Complex Capital Structure

• Requires dual presentation of EPS

• Basic earnings per share

• Presented for each separate class of

common share

• Fully diluted earnings per share

• Only securities that reduce earnings per

share (dilutive) are considered

• Securities that increase earnings per share

(anti-dilutive) are ignored

Diluted Earnings per Share Methods

• The dilutive effect of convertible securities is

measured by the if-converted method

• The dilutive effect of options and warrants is

measured by the treasury stock method

• For computing dilution, the rate of conversion

most advantageous to the security holder is

used (maximum dilutive conversion rate)

The If-Converted Method

• The conversion of the securities into common

stock is assumed to occur at the beginning of

the year

• The net income must be adjusted for:

• Interest (net of tax) on the convertible debt

• Dividends on the convertible preferred shares

• The weighted average number of shares is

increased by the additional common shares

assumed issued (at the beginning of year)

The Treasury Stock Method

• Options and warrants (and their equivalents)

are included in EPS computations

• Options and warrants are assumed exercised

at the beginning of the year

• The proceeds from the exercise of options are

assumed to be used to buy back common

shares

• The exercise price per share must be less

than the market price per share for dilution to

occur

Options and Warrants Treasury Stock Method

Given:

Exercise price of an option - [for one share of stock] $ 10

Market price of one share at exercise date:

$ 40

Options deemed exercised:

1,000

Compute the number of weighted shares for determining

diluted earnings per share

Total proceeds from exercise:

Shares assumed issued upon exercise:

Assumed reacquisition of shares:

Dilution: 1,000 - 250

=

(increase in outstanding shares)

$10,000

1,000

250

750 Shares

Earnings per Share:

Complex Structures - Summary

Dual EPS Presentation

Basic EPS

Net Income adjusted for interest

(net of tax) and preferred dividends

-----------------------------------------Weighted average number of

common shares assuming

maximum dilution

Diluted EPS

Dilutive Convertibles

Dilutive Options and

Warrants

Dilutive Contingent

Issues

COPYRIGHT

Copyright © 2002 John Wiley & Sons Canada, Ltd.

All rights reserved. Reproduction or translation of

this work beyond that permitted by CANCOPY

(Canadian Reprography Collective) is unlawful.

Request for further information should be

addressed to the Permissions Department, John

Wiley & Sons Canada, Ltd. The purchaser may

make back-up copies for his / her own use only and

not for distribution or resale. The author and the

publisher assume no responsibility for errors,

omissions, or damages, caused by the use of these

programs or from the use of the information

contained herein.