chapter 3 - McGraw Hill Higher Education - McGraw

advertisement

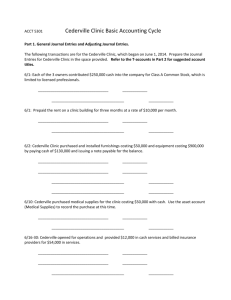

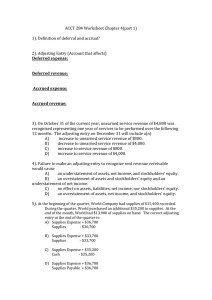

3 Completing the Accounting Cycle © 2012 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. Accounting Cycle Analyze and record the transactions Prepare the financial statements Chapter 3 Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Close the accounts and prepare trial balance 2 Matching Principle All revenues must be recorded in the accounting period in which the goods are sold or services are rendered and all expenses must be recorded in the accounting period in which they are incurred to produce such revenues Chapter 3 3 Adjusting Entries • Some journal entries are made at the end of the accounting period just to separate the effect of an event into its proper periods. • Each adjusting entry affects: 1) a revenue or expense account 2) an asset or liability account (except cash) • Examples include: 1. Recognition of accrued revenues and receivables, 2. Interest calculations, 3. Recognition of accrued expenses and payables, 4. Allocation of prepaid operating costs, and 5. Recognition of depreciation. Chapter 3 4 When do we need adjusting entries? Prepayments Accruals 1. Allocation of costs between accounting periods 3. Expenses incurred but not recorded 2. Allocation of unearned revenues between accounting periods 4. Revenues earned but not recorded Chapter 3 5 Trial Balance Chapter 3 6 Adjusting Entries Prepayments Accruals 1. Allocation of costs between accounting periods 3. Expenses incurred but not recorded 2. Allocation of unearned revenues between accounting periods 4. Revenues earned but not recorded Chapter 3 7 Adjustment (1) Prepaid Rent 1-Jan Balance 31-Jan Balance Chapter 3 Prepaid Rent 600 31-Jan 200 400 Rent Expense 200 200 8 Adjustment (2) Prepaid Insurance Prepaid Insurance 3-Jan 120 31-Jan Balance 31-Jan Balance Chapter 3 10 110 Insurance Expense 10 10 9 Adjustment (3) Office Supplies 10-Jan Balance Office Supplies 2500 31-Jan 500 2000 Supplies Expense 31-Jan 500 Balance Chapter 3 500 10 Adjustment (4) Depreciation of Property Plant & Equipment Chapter 3 11 Express Travel Agency Partial Statement of Financial Position 31 January 2014 Plant and Equipment Office Equipment and Furniture Less: Accumulated Depreciation Plant and Equipment, net Chapter 3 TL 15.000 (250) 14.750 12 Adjusting Entries Chapter 3 1. Allocation of costs between accounting periods 3. Expenses incurred but not recorded 2. Allocation of unearned revenues between accounting periods 4. Revenues earned but not recorded 13 Adjustment (5) Unearned Revenues Unearned Revenues 31-Jan 4500 22-Jan Balance Service Revenues 31-Jan 31-Jan Balance Chapter 3 7500 3000 12500 4500 17000 14 Adjusting Entries Chapter 3 1. Allocation of costs between accounting periods 3. Expenses incurred but not recorded 2. Allocation of unearned revenues between accounting periods 4. Revenues earned but not recorded 15 Adjustment (6) Accrued Salary Expense Salaries Payable 31-Jan Balance 24-Jan 31-Jan Balance Chapter 3 2500 2500 Salary Expense 9000 2500 11500 16 Adjustment (7) Accrued Interest Expense Interest Payable 31-Jan Balance 31-Jan Balance Chapter 3 210 210 Interest Expense 210 210 17 Adjusting Entries Chapter 3 1. Allocation of costs between accounting periods 3. Expenses incurred but not recorded 2. Allocation of unearned revenues between accounting periods 4. Revenues earned but not recorded 18 Adjustment (8) Accrued Revenues Accounts Receivable 31-Jan 7500 31-Jan 3450 Balance 10950 Service Revenues 31-Jan 31-Jan 31-Jan Balance Chapter 3 12500 4500 3450 20450 19 Effects of Adjusting Entries Chapter 3 20 Worksheet – Unadjusted to Adjusted Accounts Chapter 3 21 Accounting Cycle Analyze and record the transactions Prepare the financial statements Chapter 3 Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Close the accounts and prepare trial balance 22 Steps to Close Accounts • • • • Chapter 3 Close temporary accounts with credit balances to income summary Close temporary accounts with debit balances to income summary Close income summary Close dividends or owners’ withdrawals 23 Express Travel Agency Adjusted Trial Balance 31-Jan-14 Accounts Cash Accounts Receivable Office Supplies Prepaid Rent Prepaid Insurance Office Furniture and Equipment Accumulated Depreciation Bank Loan Accounts Payable Unearned Revenues Salaries Payable Interest Payable Capital Withdrawals Service Revenues Salary Expenses Rent Expense Insurance Expense Supplies Expense Depreciation Expense Interest Expense Total Chapter 3 Debit TL 102.280 10.950 2.000 400 110 15.000 Credit TL 250 15.000 5.000 3.000 2.500 210 100.000 3.000 20.450 11.500 200 10 500 250 210 TL 146.410 TL 146.410 24 Closing Credit Balances Chapter 3 25 Express Travel Agency Adjusted Trial Balance 31-Jan-14 Accounts Cash Accounts Receivable Office Supplies Prepaid Rent Prepaid Insurance Office Furniture and Equipment Accumulated Depreciation Bank Loan Accounts Payable Unearned Revenues Salaries Payable Interest Payable Capital Withdrawals Service Revenues Salary Expenses Rent Expense Insurance Expense Supplies Expense Depreciation Expense Interest Expense Total Chapter 3 Debit TL 102.280 10.950 2.000 400 110 15.000 Credit TL 250 15.000 5.000 3.000 2.500 210 100.000 3.000 20.450 11.500 200 10 500 250 210 TL 146.410 TL 146.410 26 Closing Debit Balances Chapter 3 27 Closing Income Summary Account 31-Jan Income Summary 12670 31-Jan Balance Chapter 3 20450 7780 28 Closing Withdrawals Chapter 3 29 Post Closing Trial Balance Chapter 3 Express Travel Agency Post Closing Trial Balance 31 January 2014 Accounts Debit Cash TL 102.280 Accounts Receivable 10.950 Office Supplies 2.000 Prepaid Rent 400 Prepaid Insurance 110 Office Furniture and Equipment 15.000 Accumulated Depreciation Bank Loan Accounts Payable Unearned Revenues Salaries Payable Interest Payable Capital Withdrawals 0 Service Revenues Salary Expenses 0 Rent Expense 0 Insurance Expense 0 Supplies Expense 0 Depreciation Expense 0 Interest Expense 0 Total TL 130.740 Credit TL 250 15.000 5.000 3.000 2.500 210 104.780 0 TL 130.740 30 Trial Balance after Closing Entriesincludes the accounts of which statement? Chapter 3 31 Accounting Cycle Analyze and record the transactions Prepare the financial statements Chapter 3 Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Close the accounts and prepare trial balance 32 Income Statement Chapter 3 33 Statement of Financial Position Chapter 3 34 Appendix 3 Closing Entries for Limited Liability Corporations and Corporations Chapter 3 35 Corporation Trial Balance Chapter 3 36 Closing Credit Balances Chapter 3 37 Closing Debit Balances Chapter 3 38 Closing Income Summary Account Chapter 3 39 Post closing trial balance Chapter 3 40 Chapter 3 41