INTERMEDIATE

ACCOUNTING

Seventh Canadian Edition

KIESO, WEYGANDT, WARFIELD, YOUNG, WIECEK

Prepared by:

Gabriela H. Schneider, CMA

Northern Alberta Institute of Technology

CHAPTER

20

Pensions and Other Employee

Future Benefits

Learning Objectives

1. Distinguish between accounting for the employer’s

pension costs and accounting for the pension fund.

2. Identify types of pension plans and their

characteristics.

3. Identify the accounting and disclosure requirements

for defined contribution plans.

4. Explain alternative measures for valuing the pension

obligation.

5. Identify the components of pension expense.

6. Identify transactions and events that affect the

projected benefit obligation.

Learning Objectives

7. Identify transactions and events that affect the

balance of the plan assets.

8. Explain the usefulness of—and be able to complete—

a work sheet to support the employer’s pension

expense entries.

9. Explain the pension accounting treatment of past

service costs.

10. Explain the pension accounting treatment of

actuarial gains and losses, including corridor

amortization.

Learning Objectives

11. Identify the differences between pensions and postretirement health care benefits.

12. Identify the financial reporting and disclosure

requirements for defined benefit plans.

13. Identify the financial accounting and reporting

requirements for defined benefit plans whose

benefits do not vest or accumulate.

14. Explain the basics of what current service cost, the

projected benefit obligation and past service cost

represent. (Appendix 14A)

Pensions and Other

Employee Future Benefits

Introduction

and

Terminology

Nature of

pension

plans

Defined

contribution

plans

Defined

benefit plans

The role of

actuaries

Defined Benefits

that Vest or

Accumulate Basics

Alternative

measures of the

liability

Capitalization vs.

non-capitalization

Major components

of pension

expense

Projected benefit

obligation and

plan assets

Basic Illustration

Defined Benefits

that Vest or

Accumulate Complexities

Past service costs

Actuarial gains and

losses

Corridor

amortization

Other benefits that

vest or accumulate

Comprehensive

illustration

Reporting defined

benefit plans

Perspectives

Plan complexities

Defined

Appendix ABenefits Example of a

that do not One Person

Vest or

Plan

Accumulate

Current

Postservice cost

employment Projected

benefits

benefit

and

obligation

compenPast

sated

Service

absences

Cost

Pension Plans

• A pension plan provides benefits to retirees for

services provided during employment

• Employer sponsors and contributes to fund,

and incurs the cost of the pension plan

– Accounting for the employer

• Pension plan receives the contributions,

administers pension assets, and makes

pension payments to the beneficiaries

– Accounting for the pension plan

Pension Fund Stream

TRUST

COMPANY

Pension Expense

Cash paid to pension

plan (funding)

Accrued pension

asset/liability

$

Plan

Assets

Projected Benefit

Obligation

Employees (pension benefits)

Pension Terminology

• Contributory

– Employee and employer make contributions to the

plan

• Non-contributory

– Employers bear the full cost of the pension plan

– No contributions made by employee

• Vested

– Amounts in the plan become the legal property of

the employee

• Employee is entitled to receive benefits even after

leaving the employ of the corporation

– Governed by provincial law

Defined Contribution Plans

• Employer contributes a defined sum to a third

party – plan trustee

– Ownership of plan assets assumed by trustee

• Employee assumes the economic risk

– No guarantee made by employer as to benefits

paid

• Cost of the plan in the current year is known

with certainty

Defined Contribution Plans

• Liability reported if contribution (funding) is

less than required

• Asset reported if the amount contributed is

more than required for the period

• Disclosure requirements:

– Annual pension expense amount

– Nature and effect of matters affecting

comparability

Defined Contribution Plans:

Employers’ Journal Entries

Contribution made

is less than

the pension expense

Contribution made

is more

than pension expense

Pension Expense Dr

Cash

Cr

Accrued Pension

Liability

Cr

Pension Expense Dr

Accrued Pension

Asset

Dr

Cash

Cr

Liability

Asset

Exercise 20-1: LinDu Limited

Given: Defined Contribution Plan

Employee Contribution:

5% of gross pay

Employer Contribution:

Equal amount

November 30, 2005:

$25,500 combined

employee and employer contribution owing

December 2005:

$274,300 gross pay

Exercise 20-1: LinDu Limited

Requirement a)

December 10, 2005 Journal Entry:

Pension Liability

Cash

25,500

25,500

To record payment to pension trustee

Exercise 20-1: LinDu Limited

Requirement b)

5% of December gross pay =

$274,300

x .05

Employer Contribution Expense

13,715

Exercise 20-1: LinDu Limited

Requirement c)

Current liability:

Pension Contributions Payable

($13,715 + $13,715)

$ 27,430

This assumes amounts for previous months

were remitted as required each month. At

December 31st all that remains as payable is the

amount withheld from employees in December

and the required employer matching amount.

Defined Benefit Pension Plans

• End benefit received by employees is predefined

– Contributions based on formula:

• Employee’s years of service and expected salary

level at retirement

– Actuarial assumptions used extensively in

accounting for defined benefit plans

– Cost of plan in current year not known with

certainty

• The employer remains liable to ensure benefit

payments

• Employer is the trust-beneficiary

Defined Benefit Pension Plans

•

Pension obligation valuation

1. Vested benefit obligation

– Based on current salary levels

– Includes only vested benefits

2. Accumulated benefit obligation

– Based on current salary levels

– Includes both vested and nonvested service

3. Projected benefit obligation

– Based on future salary levels

– Includes both vested and nonvested service

Pension Liability Measurement

Recommended

method - CICA

Handbook, Section

3461

Pension obligation

Present value of

the estimated

future benefits to

be paid to

employees

Vested benefit obligation

Accumulated benefit

obligation (ABO)

Projected benefit obligation

(PBO)

Pro-rated on salaries Pro-rated on service

Projected Benefit Obligation

(PBO)

• Pro-rated on salaries

• Annual funding based on percentage of

total estimated compensation earned by

the employees over their career

• Pro-rated on services

• Annual funding based on the total

estimated benefit being allocated evenly

over the years of service of the employee

Projected Benefit Obligation

(PBO)

• Defined as the portion of the defined

obligation attributed to services provided to

date

– Based on the present value of vested and

nonvested benefits

• Also referred to as accrued benefit obligation

Capitalization vs.

Noncapitalization

• Capitalization

– Full obligation recognized as liability

– Pension plan assets reported as assets

– Liability and assets reduced by payment of

benefits

• Noncapitalization

– Follows substance of the plan as separate

legal and accounting entity

– Obligation on B/S = amount of expense

recognized less amount funded

– Adopted by Accounting Standards Board

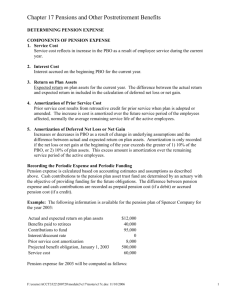

Components of

Pension Expense

Service Cost for

Current Year

+

Interest on the

Liability

+

Expected return on

Plan Assets

Pension Expense

+

Amortized

Past Service Costs

+ or

Amortized

Net Actuarial Gain

or Loss

+ or

Amortized

Transitional

Asset or Obligation

Components of

Pension Expense

• Service Cost

– The amount of pension benefit earned in the

current period

• Interest

– Consider PBO as a long-term liability (albeit offbalance sheet) that accrues interest

– Interest rate used is the current yield on highquality debt, or current settlement rate

Components of

Pension Expense

• Expected Return on Plan Assets

– The assets in the pension plan earn income and

this income including any capital appreciation

reduces the eventual cost of the pension

– Long-term rate of return applied to fair value of

plan assets

Components of

Pension Expense

• Amortization of Past Service Costs (PSC)

– PSC are from either the initial adoption of a

pension plan or an amendment to improve the

existing plan

– PSC are the present value of those additional

future benefits

– Amortized over the expected period to full

eligibility of the employee group

Components of

Pension Expense

•

Amortization of Net Actuarial Gains/Losses

–

Two sources for these gains and losses

1. Change in plan’s actuarial assumptions

2. Plan experiences gains and losses

–

Amortized using “corridor approach”

Components of

Pension Expense

• Amortization of Transitional Asset or

Obligation

– Stem from CICA Handbook, Section 3461

(introduced in 2000)

– When Section 3461 is applied prospectively,

any difference between plan assets and PBO

is amortized

– Amortization period is the Expected Average

Remaining Service Life (EARSL)

Notes on EARSL

• EARSL is the expected average remaining

service life of the employee group

• It is another number determined by the

actuary

• Consider the following example

EARSL

Picture a bus full of employees heading for retirement.

Given an EARSL of 10 years in 2005, what is a reasonable

EARSL in 2006?

Are the same employees on the

bus at retirement as were on at

the beginning?

2005

2006

Retirement

Some got on the bus, others got off the bus…

A reasonable estimate for 2006 might be 10 years.

Summary of Pension Expense

Components and Methods

Pension expense

component

Method used to Effect on pension

determine cost

expense

1 Service Cost

Present Value

+

2 Interest Expense

Current Rate

+

3 Expected Return

on Plan Assets

Long-Term Expected Rate

of Return

-

4 Prior Service Cost

Amortize

+

5 Actuarial Gains

and Losses

Corridor method

(amortize excess)

+/-

6 Transition Gains

and Losses

Amortize over EARSL

+/-

PBO Transactions

PBO, beginning of period

+ Current Service Cost

+ Interest Cost

+ PSC during period

Benefits paid to retirees

Actuarial Gains

+ Actuarial Losses

= PBO, end of period

• The PV of pension

benefits earned to date

by employees

• Most information

relating to PBO

provided by actuaries

Plan Assets Transactions

Plan assets (FV) beginning

of period

+ Employer/employee

funding

Actual return

Benefits paid out

= Plan assets (FV) end of

period

Actual return

= expected return

+ experience gain or

Experience loss on assets

Funded Status

• Funded status = PBO FV of plan assets

• PBO > Plan assets = underfunded

• PBO < Plan assets = overfunded

Notes on Pension

• CICA Handbook, Section 3461 recommends the

noncapitalization approach

– Pension amounts recorded by the company (most

are disclosed in notes)

• PBO

• Plan Assets

• Unrecognized Past Service Costs (PSC)

• Unrecognized Net Actuarial Gains/Losses

• Unrecognized Net Transitional Asset/Liability

The Pension Worksheet

• Used to accumulate information needed to

record both the formal journal entries and

the memo entries to keep track of the

relevant pension plan items and

components

The Pension Worksheet

General Journal Entries

Items

Annual

Pension

Cash

Expense

Accrued

Pension

A/L

Memo Record

Projected

Benefit

Obligation

Plan

Assets

Beginning Balances recorded here

An ending credit

An ending debit

balance here is

balance is

reported with

reported with

Long-term

other Deferred

Liabilities

Charges

Pension transactions are recorded through the worksheet,

using debits and credits (all entries must therefore balance)

The Pension Worksheet Example

General Journal Entries

Items

Annual

Pension

Cash

Expense

Bal.

a)

b)

c)

d)

e)

Accrued

Pension

A/L

Memo Record

Projected

Benefit

Obligation

Plan

Assets

100,000 Cr. 100,000 Dr.

9,000 Dr.

10,000 Dr.

10,000 Cr.

9,000 Cr.

10,000 Cr.

8,000 Cr.

7,000 Dr.

9,000 Dr.

10,000 Dr.

8,000 Dr.

7,000 Cr.

9,000 Cr.

8,000 Cr. 8,000 Cr.

1,000 Cr. 112,000 Cr. 111,000 Dr.

Pension Entries

To record:

Pension Expense

9,000

Accrued Pension/Liability

To record contribution:

Accrued Pension Liability 8,000

Cash

9,000

8,000

Actuarial Gains and Losses

• Caused by:

1.

2.

3.

Actual return on plan assets differing from

expected return

Changes in actuarial assumptions affecting the

PBO

Actual experience in PBO differing from expected

experience

• If changes large enough, including full amount of the

gains or losses in expense results in substantial

fluctuations in reported pension expense

• Amortization allows for “smoothing” the impact of

these changes

Actuarial Gains and Losses

• Over time, accumulated effect of the changes (net

gains/losses) may even out

• Corridor approach adopted to allow for

circumstances where no accumulating offset occurs

• Amortization used only when the opening

unrecognized gains/losses are greater than 10% of

the larger of the opening balance of the PBO and the

FV of Plan Assets

• Amount calculated under the Corridor Approach

uses Beginning Balances only

Corridor Approach - Example

Opening Balance 2004

$400,000 2005

PBO, JanuaryLess:

1

Corridor $2,100,000

280,000 $2,600,000

$120,000 2,800,000

FV Plan Assets, Jan. 1

2,600,000

Amortized

–

Net Actuarial Loss

(gain) over 5.5 years

400,000

300,000

average remaining service life

$678,182280,000

Corridor –Opening

10% of theBalance

larger of

260,000

(400,000

– 21,818 + 300,000)

the PBO or

PA

Less:

Corridor

Cumulative

Net Actuarial

Loss

(Beginning of Year)

290,000

0

400,000

$388,182

2006

$2,900,000

2,700,000

(170,000)

290,000

678,182

Amount to be Amortized

0

120,000

388,182

Current Year Amortization

0

21,818

70,579

Disclosure Requirements –

Defined Benefit Plans

• All enterprises must disclose:

– Amounts recorded in the financial statements

– Off-balance sheet accounts

– Underlying assumptions

• Financial institutions and public enterprises have

additional disclosure requirements

– Reconciliation of PBO and Plan Assets beginning

and ending balance

– Unamortized balances of PSC, Net actuarial

Gains/Losses, Net Transitional amounts; and

amortization amount for each

Defined Benefit Plans

• E.g. parental leave plans (in excess of what

government provides), some long-term

disability plans

• No basis on which to accrue expense –

benefits not related to service provided.

Entitlement comes with being an employees

Defined Benefit Plans

• Therefore use “event accrual” method to

accrue full cost

• When event occurs that obligates entity:

Benefit Expense

xx

Benefit Liability

xx

Defined Benefit Plans

• When the compensated absence is taken

event occurs that obligates entity:

Benefit Liability

xx

Cash

xx

COPYRIGHT

Copyright © 2005 John Wiley & Sons Canada, Ltd.

All rights reserved. Reproduction or translation of

this work beyond that permitted by Access Copyright

(The Canadian Copyright Licensing Agency) is

unlawful. Requests for further information should be

addressed to the Permissions Department, John

Wiley & Sons Canada, Ltd. The purchaser may make

back-up copies for his or her own use only and not

for distribution or resale. The author and the

publisher assume no responsibility for errors,

omissions, or damages caused by the use of these

programs or from the use of the information

contained herein.