PS-3-Croft 2719KB Dec 14 2009 01:08:49 PM

advertisement

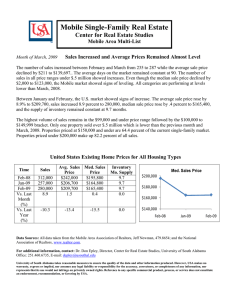

Economic Outlook A Brave New World April 15, 2009 Presented by: Patricia Croft, Chief Economist RBC Global Asset Management The Great Recession of 2009 We are all looking for answers 1. Have stock markets bottomed? 2. Is the worst of the economic downturn behind us? 3. Have we found a solution to the credit crisis? 4. What are the longer term implications of today’s epic policy response? The Great Recession of 2009 World economy set to contract for first time since WWII Recession is global with hardest hit countries those that are most reliant on exports There is no quick fix Global financial system is still dysfunctional Enormous negative wealth effect Debt overhang still considerable Key to recovery: Recapitalization of world banking system Policy response The Fiscal Policy Response Country Package Size % GDP China $ 586 billion 14.0% US $ 787 billion 5.5% UK $ 50 billion 2.5% India $ 26 billion 2.4% Canada $ 34 billion 2.0% Japan $ 85 billion 1.7% Eurozone $ 260 billion 1.5% Germany $ 39 billion 1.3% TOTAL $2292 billion 2.8% The Monetary Policy Response The Race Towards Zero US 0.0 to 0.25% UK 0.5% Canada 0.5% 5 ECB 1.25% 4 Japan 0.1% G7* Real Central Bank Policy Rate 3 1 0 -1 2008 2006 2004 2002 2000 1998 1996 1994 1992 1990 1988 1986 1984 -3 1982 -2 1980 % 2 *GDP weighted average of US, Japan, Eurozone, UK & Canada target interest rates minus inflation Source: National Central Banks, National Statistical Agencies, PH&N. Dec 2008 is an estimate. A Challenging World The Patient Has Yet to Respond Nominal policy rates are already at zero – but this is not a cost of money problem Quantitative easing now underway in the US, Japan and the UK – Canada headed that way Today’s fight is against deflation and depression – tomorrow’s battle is against inflation and reversing fiscal trends Financial Market Stress is Easing 80 70 60 50 40 30 20 10 0 U.S. Dollar LIBOR % Index CBOE Volatility Index (VIX) Source: U.S. Federal Reserve, Bank of England CDX Credit Default Swap Index Source: Bloomberg 900 US$ billions Index Source: Chicago Board Options Exchange 300 275 250 225 200 175 150 125 100 75 50 25 0 5.5 5.0 4.5 4.0 3.5 3.0 2.5 2.0 1.5 1.0 U.S. Financial Commercial Paper Outstanding 850 800 750 700 650 600 550 500 450 Source: Federal Reserve Bear Market Rally A Welcome Relief Major Markets Since January 2008(local currency terms) 110 Index, Jan. 1, 2008 = 100 100 90 Lehman Bros Fails 80 70 60 50 S&P 500 S&P/TSX MSCI EAFE MSCI Emerging 40 Source: Datastream Key is Estimate of Credit Losses Estimated Losses ($ Billions) Residential Mortgages US Banks 1,100 508 Commercial Real Estate 234 125 Credit Cards 226 169 Auto Loans 133 78 C&I Loans and Corp Bonds 390 81 2,083 962 TOTAL Source: GS Equity Research Leading Indicators Plunge Leading Economic Indicators: OECD & Selected Non-OECD 105 Index 100 95 OECD Non-OECD* 90 * Trade-weighted average of China, India, Brazil, Russia, Indonesia & South Africa 85 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Source: Organization for Economic Cooperation & Development, PH&N No Region Spared, But Trading Nations Worst Hit Quarterly % change, annualized Q4 Real GDP Growth 6 0 -6 -12 -18 -24 Source: The Economist When the US Consumer Catches a Cold… The U.S. Consumer in Perspective (% share of GDP: 2008) Exports Crater Across the Globe (year-over-year % change) 18.0 16.0 0.0 14.0 -5.0 12.0 -10.0 10.0 % -15.0 8.0 -20.0 % 6.0 4.0 -25.0 -30.0 -35.0 2.0 0.0 -40.0 -45.0 -50.0 Source: Bureau of Economic Analysis, IMF, Banc of America Securities – Merrill Lynch Source: Bloomberg, Banc of America Securities – Merrill Lynch U.S. in Recession – Now What? Recession began in December 2007 – 16 months old Now spread beyond the consumer in a negative feed back loop No meaningful recovery expected until 2010 Layoffs Pile Up 160,000 140,000 120,000 100,000 80,000 60,000 40,000 20,000 0 Source: WSJ Research, Updated March 3, 2009 Consumer Net Worth Eviscerated U.S. Household Net Worth Year-over-year Change 10,000 $ billions 5,000 - -5,000 -10,000 -15,000 1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 Source: U.S. Federal Reserve, Merrill Lynch From Conspicuous Consumption to Thrift? US Household Debt Relative to Disposable Income 150 Household deleveraging will be a drawnout process 130 % 110 90 70 Source: U.S. Federal Reserve Flow of Funds 2004 2000 1996 1992 1988 1984 1980 1976 1972 1968 1964 1960 1956 30 1952 50 U.S. House Prices – Close to a Bottom S&P/Case-Shiller US Home Price Index 25 Housing affordability at 250 Year-over-year growth rate (LHS) record high 20 Home sales up in 15 200 February 10 5 0 150 Housing starts have plunged But foreclosures still -5 -10 100 -15 rising and inventories remain high Further 10 to 15% Source: MacroMarkets LLC 50 2009 2007 2005 2003 2001 1999 1997 1995 1993 1991 1989 1987 -20 -25 Index % change year-over-year Index level (RHS) decline in house prices but bulk of the adjustment is behind us U.S. Deficit Set to Soar Debt and Deficit (% of GDP) 25 20 80 Financial balance (left) Net debt (right) 48 10 32 5 16 0 0 -5 -16 -10 -32 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 Debt to GDP ratio will rise sharply Higher private sector savings will offset public sector dissaving Longer term issue: intergenerational transfer of taxes 64 15 Source: Finance Canada, OECD Economic Outlook No. 84, Nov 2008. Data is general government, national account basis Fed’s Balance Sheet Explodes but Velocity of Money Plummets U.S. Federal Reserve Assets Money Velocity 2.5 19 18 17 2.0 Times GDP US$ Trilions 16 1.5 1.0 9/11 Y2K 15 14 13 12 0.5 11 10 Source: Federal Reserve 9 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 0.0 1999 Nominal GDP / Monetary base (M0) Source: Federal Reserve, BEA, PH&N Canada - Last In First Out? Canadian Q1 job losses worst in 26 years – unemployment rate to rise to over 9% Consumer confidence weak – home sales and car sales plunge Impact of lower commodity prices now feeding through Lower C$ offers some relief Harper/Carney optimistic – for now Canadian Economy: Slam on the Brakes Canadian Real GDP Growth 2009 2010 6.0 –2.2% +1.0% 4.0 % 2.0 0.0 -2.0 Month-over-month -4.0 Year-over-year Quarterly GDP (ann.) -4.8% BoC -5.5% PH&N -6.2% Built-in -6.0 -8.0 2006 2007 Source: Statistics Canada, PH&N 2008 2009 Regional Variations Set to Narrow Retail Sales Change, Jan. 2008 - Jan. 2009 0 Provincial Unemployment Rates 16 Canada 15 -1 Ontario 14 -2 Quebec Year-over-year % change 13 12 -3 11 % -4 10 9 -5 8 -6 7 6 -7 Source: Statistics Canada Source: Statistics Canada 2008 2004 2000 1996 1992 1988 BC AL ON MB QC NS NL PEI NB SK 1984 -9 4 1980 -8 1976 5 A Rare Synchronized Global Economic Recession Europe in recession led by Germany – periphery countries under pressure Bank of England slashes interest rates, recognizing economy in deep trouble Japan’s economy fragile – depression? India slowing – central bank cutting rates China easing massively as economic growth stalls World growth set to contract in 2009 – Recovery a 2010 story Starting to See Green Shoots! US – car sales, home sales, retail sales, housing starts, PMI Canada – car sales, retail sales, trade balance UK – house prices, leading indicator, PMI China – electricity production, cement demand, car sales, home sales, PMI Appears the worst is behind us but the contours of the recovery remain uncertain 140 80 120 75 100 70 Hungarian Forint 240 200 180 160 Mar-09 10 Jan-09 11 Nov-08 12 Sep-08 13 Jul-08 14 Mar-09 Jan-09 Nov-08 Sep-08 Jul-08 May-08 Mar-08 Jan-08 160 150 140 130 120 110 100 90 80 70 60 May-08 15 KNR per USD Mexican Peso Mar-08 220 USD per CAD Mar-09 Jan-09 Nov-08 Sep-08 Jul-08 May-08 Mar-08 MXN per USD 16 Jan-08 Mar-09 Jan-09 Nov-08 Sep-08 Jul-08 May-08 Mar-08 260 Jan-08 9 Jan-08 Forint per USD Currency Markets Incredibly Volatile Icelandic Kronor 105 Canadian Dollar 100 95 90 85 Canadian Dollar Parity Not Justified Labour Productivity, Canada & US 160 6 Index, 1997 - 2007 = 100 5 3 2 1 0 150 United States 140 Canada (in USD terms) 130 120 110 100 90 Source: Statistics Canada, US BLS 2003 2005 2007 2009 1999 2001 1997 1995 1991 1993 2009 2008 2007 2006 2005 2004 2003 2002 60 2001 -2 2000 70 1999 -1 1987 1989 80 1998 % Year-over-year 4 Manufacturing Unit Labour Costs Source: Bank of America-Merrill Lynch, Statistics Canada, Bureau of Economic Analysis “In regione caecorum rex est luscus” In the land of the blind, the one-eyed man is king - Desiderius Erasmus 150 U.S. Dollar Trade-Weighted Index 140 130 Index 120 110 100 90 80 70 Major currency index 60 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 Source: U.S. Federal Reserve 2009/10 – Risky Business 1. Global credit deadlock 2. Global depression and deflation – paradox of thrift 3. Further fallout from credit crisis - sovereign defaults 4. President Obama/protectionism/populism 5. Unrest in China, Russia as unemployment rises 6. U.S. dollar collapses Long Term Downtrend Not Over Yet U.S. 10-Year Treasury Bond Yield 16 10-year yield 14 60 per. Mov. Avg. (10-year yield) 12 8 6 4 Source: U.S. Federal Reserve 07 04 01 98 95 92 89 86 83 80 77 74 71 68 65 62 59 0 56 2 53 % 10 Equity Valuations Look Very Attractive Reflation vs. Deflation Forward P/E Ratios 28 26 24 P/E Ratio 22 20 18 16 14 S&P 500 12 TSX 10 MSCI EAFE 8 1998 1999 2000 2001 2002 2003 2004 Source: I/B/E/S 2005 2006 2007 2008 2009 A Brave New World - Implications for Investors 1. Bears are in vogue – great contrarian indicator 2. Epic policy response will put a floor under global economy – will take time to work through the credit/deleveraging/economic cycle 3. Equity markets look extremely attractive although bottoming process may be prolonged 4. Legacy of the credit crisis: more government intervention, more regulation, more transparency, less leverage, change in world order 5. Lower equity risk premium? 6. Inflation will be an issue post 2011 – US dollar ultimately debased