Slide 7

advertisement

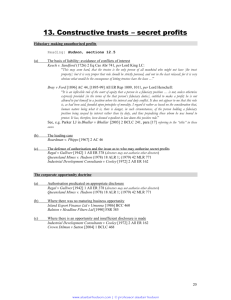

Eternal Issue No Perfect Solution Principal-agent problems • Can be present in any contract. • Agent has better information than principal; costly for principal to assure himself of agent’s performance quality. • Reduces value of agent’s performance. • Greater as complexity and discretion increase. 2 Regulatory Strategies Governance Strategies Agent Constraints Affiliation Terms Appointment Decision Rights Rights Agent Incentives Ex ante Rules (tender offers) Entry (disclosures on borrowing) Selection (appointing directors) Trusteeship (outside directors on audit comm.) Ex post Standards (self dealing) Exit (right to Removal sell stock) (removing directors) Initiation (resolutions) Veto (merger Reward ratification) (stock options) 3 Coase’s “Theory of the firm” • Some people get the Nobel prize for complicated and technical work that is difficult to understand. Coase is at the other extreme. His contribution to economics has consisted of thinking through certain questions carefully and in the process demonstrating that ideas accepted by virtually the entire profession were false. 4 Why are there firms? • Markets coordinate economic activity without conscious direction. • Firms are “supersession of the price mechanism”. – “islands of conscious power in this ocean of unconscious cooperation like lumps of butter coagulating in a pail of buttermilk.” • D.H. Robertson 5 Price mechanism has costs. • Discover prices • Negotiate/write/enforce contracts • Price fluctuation risks • Firms are institutional arrangements that coordinate some types of economic activity more cheaply than markets. • Key is absence of price mechanism – Precontracted resources (labor, capital) 6 Explaining firms • “People adopt other forms which they hope will produce the right result. They change the forms of contracts, taking account of it. They do lots of things. The firm itself is a response to that, but lots of contracts are as well. Even the form of markets, what you can trade: The rules and regulations of the submarket or produce exchange are designed to reduce transaction costs.” – Ronald Coase 7 8 Why we care • “What Coase – and everything that follows from him – helps us do is answer the question ‘What is the boundary of the firm, and how hard should that boundary be?’ It helps you think about things like whether to buy, build or partner.” – Charles Conn, Pres. Ticketmaster Online 9 Regulatory Strategies Governance Strategies Agent Constraints Affiliation Terms Appointment Decision Rights Rights Agent Incentives Ex ante Rules (tender offers) Entry (disclosures on borrowing) Selection (appointing directors) Trusteeship (outside directors on audit comm.) Ex post Standards (self dealing) Exit (right to Removal sell stock) (removing directors) Initiation (resolutions) Veto (merger Reward ratification) (stock options) 10 Fiduciary Duty • • • • • Hamburger v. Hamburger, 1995 WL 579679 (Sup.Ct. Mass. 1995) David (son of Joe) becomes sales manager. Uncle Ted “increasingly resentful”, tries to fire David. Ted tells David future depends on whether Joe or Ted lives longer. David leases space, gets financing, quits, starts competitor, solicits Ace’s employees and customers. • No violation of fiduciary duty to arrange financing and lease space, despite being “key employee”. • No violation in post-employment solicitations of EE and customers. • “Under the circumstances in which he found himself, David took the only reasonable course open to him and did so in a way which the court finds did not violate any legal obligation to Ted or Ace.” 11 CCS & Hamburger • Background fiduciary obligation – Impact of employment contract (CCS) vs. at-will status (Hamburger) – Can be supplemented via additional contracting (covenant not to compete) – But, courts limit scope of some contractual provisions. 12 Fiduciary duties & creditors • Role of background agency principles – Actual authority: P manifests consent to A (expressly or by implication) – Apparent authority: P manifests consent that A act for P to 3rd Party (expressly or by implication) – Inherent authority: P has not manifested consent for A to act to anyone, but based on expectations of 3rd Parties 13 Blackburn v. Witter 19 Cal. Rptr. 842 (Ca.App. 1962) • “Respondent is a widow….” • Sharp Dean Witter salesman (Long) flimflams widow by persuading her to sell stocks and invest in special promissory notes (from non-existent company). • Did Blackburn know (or should she have known) that Long’s actions in connection with the notes were unauthorized? • If there were warning signs that a reasonable person would have heeded pointing to lack of authority, then no apparent authority. – Long using “rediform” receipts, omission of transactions from monthly accounts • But – Dean Witter knew of Long’s gambling debts and drinking problems and that he was “churning” accounts to get commissions. 14 California Law on Point • CA Civ Code s2317: “Ostensible authority is such as a principal, intentionally or by want of ordinary care, causes or allows a third person to believe the agent to possess.” • CA Civ Code s2334: “A principal is bound by acts of his agent, under a merely ostensible authority, to those persons only who have in good faith, and without want of ordinary care, incurred a liability or parted with value, upon the faith thereof.” 15 Sennott v. Rodman & Renshaw 474 F.2d 32 (7th Cir. 1973) • Fraudulent securities activity by former associate of firm who was son of partner. • Jordan leaves firm in 1958. • Sennott asks Jordan to buy stock for him in 1964 via R&R; Jordan uses special phone to place order. • Jordan offers Sennott options in Skyline via his father at large discount; Jordan simply takes $. • Sennott does not cooperate with R&R investigation. • Sennott learns of Jordan’s past. • Court finds no reliance on apparent authority of Jordan in fraudulent transactions for options. 16 Blackburn & Sennott • Standard, not rule – harder to find contractual solutions ex ante. • Unifying approach: who is in the best position to prevent problem? 17 Self Dealing • What is it? • Does it exist any time a partner is on both sides of a transaction? • Is it curable by advance disclosure? • Is it OK if the partnership suffers no harm? • Vigneau v. Storch Engineers – Merluzzo and Vigneau violate their fiduciary duties by not disclosing involvements in projects and so must disgorge all profits – Connecticut puts burden of proof on the fiduciary to prove fair dealing and providing clear and convincing evidence to support fair dealing. 18 Fiduciary duty & management • Covalt v. High, 675 P.2d 999 (NM App. 1983) – C & H Partnership owns building it rents to C&H, Inc. C leaves C&H, Inc. Demands C&H Partnership raise rent. H refuses to agree. No breach of duty. • Issue turns on whether there is a gap in partnership contract that should be judicially filled by fiduciary duty. • Would rational investors in the shoes of the parties intend to grant each other the right to vote selfishly without risk of judicial review? 19 Recap • Fundamental problem is solving principalagent issue. • Governance issues are critical to successful operation of businesses. • Choosing the proper entity is important. • You have great flexibility to design an organization to meet your needs 20