Week 3 Lecture Notes

advertisement

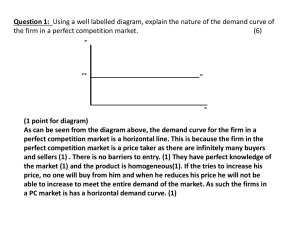

1 Class Reading • Remainder Part B: 118- 176 • Part C: 117- 217 • Knowing the diagrams in this section is very important • Book: CIMA (certificate 4) Fundamentals of Business Economics -Chapter 6a: 118-131 -Chapter 6b: 132-157 -Chapter 7: 158-176 -Chapter 8a:177-191 -Chapter 8b:192- 217 2 Market Structures- Perfect Competition & Monopoly The firm’s output decision • Total revenue (TR): total proceeds of selling a given quantity of output • Average revenue (AR): price per unit • Marginal revenue (MR): the additional to total revenue from the sale of one extra unit A price maker can only sell a finite amount at $ $ per unit A price taker can sell all its output at the same price. MR & AR are constant & equal any given price. To sell more, the price must be reduced. This means that MR is always less than AR (to sell one more unit, the price of all units must fall) MR may become negative P AR=MR MR Sales AR= demand Sales 3 • Both the price taker and the price maker maximise profit at MC=MR, MC=MR is the profit maximisation position At outputs less than Q the extra cost of making an extra unit is less than the extra revenue from selling it Price Taker MC $ per Unit At outputs greater than Q the extra cost of making an extra unit exceeds the revenue from selling it Price Maker MC $ Loss Profit Profit Loss MR Q Sales Q Sales 4 Perfect Competition • Characteristics of the perfectly competitive market – Many buyers and sellers; each firm is a price taker, unable to influence market price – Buyers and sellers act rationally and have the same, perfect information – The product is homogenous (common throughout) – There is free entry and exit for firms – There are no transport or information costs – Normal profits are earned in the long run 5 • In the short run, the number of firms is fixed. Firms may make losses or supernormal profits by operating at the profit maximising level of output, ie. Where MC=MR Price $ MC Price $ MC AC AC D=AR=MR Super Normal Profit Loss P Max Output D=AR=MR P Max Output 6 • In the long run, because there are no barriers to entry or exit, super normal profit is competed away and lossmaking firms leave the industry. The remaining forms can only make normal profit and will operate where MC=MR=AC=AR=price per unit. Price $ MC $ S AC Market Supply Price Price D Qm Output (industry as a whole) Qf Output (Smaller Scale) 7 Monopoly • A monopolist is a price maker and the firm’s AR curve is the market and demand curve MC=S p x Figure 1 z y w AR=D Qm Qpc MR 8 • The monopolist has market power and can increase sales by reducing price. • As a result AR falls as output increases and MR is always less than AR • MR becomes negative when demand becomes inelastic and further price cuts, though increasing volume, reduce turnover. • By restricting output to Qm, the monopolist can charge a price greater than the average cost; thus making supernormal profit XYZP • This represents consumer surplus transferred to the monopolist. The area WYZ is consumer surplus totally lost and is called the deadweight loss of monopoly 9 • The monopolist restricts output to Qm in order to maximise profit by producing where MC=MR. • Qm is not at the lowest point on the AC curve: the monopolist produces less than under perfect competition Qpc and at a higher cost. Monopoly does not display allocative or technical efficiency Other features of monopoly: Barriers to Entry: • Barriers to entry prevent other firms from challenging the monopolist’s priviliged position 10 Barriers: • Legal (eg nationalisation law & patents) • Absolute cost (privileged access to cheap raw materials) • High fixed costs regardless of market share (eg creating the infrastructure for a phone market) • Economies of scale where the long run average cost curve falls indefinitely and new entrants do not have sufficient market share to operate cheaply • Product differentiation: an existing product with a powerful brand can create customer loyalty, thus imposing very high promotion costs on a new entrant 11 Price Discrimination • Occurs when a firm sells the same product at different prices in different markets • The seller must be able to control the supply of the product. Clearly a monopolist can • The seller must be able to prevent the resale of the product. Grouping by status (eg age), time, geography, permits this. Customer ignorance helps the supplier • Elasticity of demand must vary between the markets, so that some customers are wiling to pay a higher price 12 X inefficiency • Apart from technical and allocative inefficiency, monopolies may display X inefficiency: they have little incentive to control costs so their AC curve moves upwards For Monopolies • If LRAC falls indefinitely as output increases and economies of scale continues to rise, the monopolist can charge lower prices than perfect competition. This is evident in a natural monopoly • Monopolies can spend more on R&D • Find it easier to raise capital for new ventures, which aids economic growth • Supernormal profits stimulate competition: a temporary monopoly under a patent may encourage improvements 13 • Patent rights reward innovation and entrepreneurial flair, both which are needed for economic growth Against Monopolies • The monopolist’s supernormal profit is obtained at the expense of the consumer • Monopolies display technical, allocative and X inefficiency (X-inefficiency is the difference between efficient behaviour of firms assumed or implied by economic theory and their observed behaviour in practice) • Resort to restrictive practices such as price discrimination to further increase their profits • Product differentiation wastes resources in the pursuit of monopoly advantages • Diseconomies of scale may arise • If a monopolist controls a vital resource, can take decisions that affect public interest adversely 14 Monopolistic Competition, Oligopoly & Duopoly Monopolistic Competition • Monopolistic competition differs from perfect competition in that firm’s products are comparable rather than homogeneous. • Under conditions of monopolistic competition, firms try to achieve monopoly profits by product differentiation. This gives each firm power over its own market price. They are thus price-makers and experience downward sloping demand (AR) and MR curves, see diagram on next slide. 15 Monopolistic Competition $ MC AC p AR=D Q Output MR 16 Features of Monopolistic Competition • In the short run the firm can make supernormal profits by shifting the demand/AR curve to the right. The previous diagram is then exactly like that of the monopolist in the long run • Because there are no real barriers to entry, these profits can probably be competed away: the demand curve shifts back left to produce the long run equilibrium shown in the diagram • Like monopoly, monopolistic competition does not produce where AC is at a minimum: it is technically inefficient • The firm will probably always have excess capacity, for the same reason • The extent to which the product differentiation is a real and thus a source of utility or spuriously created by advertising will vary from time and product to product 17 Contestable Markets • A contestable market is similar to perfect competition, even though there are few suppliers. • A lack of entry and exit barriers deters firms from trying to obtain supernormal profit. • The firm produces at minimum AC and where AC=MC=MR=AR, just as in perfect competition 18 Oligopoly • In an oligopoly a few large suppliers dominate the industry. These suppliers are independent in their decision making: they must consider their competitor’s responses to any changes they make • The kinked oligopoly demand curve illustrates the interdependent decision making of competing oligopolies. While the oligopolist has market power, any change in price is likely to be met with powerful response. • The demand is elastic at levels above P since a price rise by one firm would not be matched and purchasers would deal with other suppliers. • The demand curve is inelastic below P: competitors would match any price cut by one firm and so market share would not change very much • The kinked demand curve means an oligopolist has a discontinuous MR curve. This means there is a trend for price stickiness in oligopoly, because there is a range of points where MC=MR 19 Oligopoly $ MC Kink in the demand curve MR p X Y D Q MR Output 20 • Oligopolists may avoid competing by having an informally acknowledged price leader who sets the prevailing price or there may be a formal cartel agreement to control price by restricting output. This is illegal in the US and EU, though some countries have official schemes for favoured industries. • Because of the uncertainty over pricing decisions in oligopoly, non-price competition prevails in oligopolybranding and advertising. Duopoly • A duopoly is an oligopoly market structure containing only two firms. The two firms can either collude or compete • If the firms compete, one firm can only gain at the expense of the other firm • This highlights the interdependence between firms • A firm must decide whether to try increase its market shar at the risk of retaliation from the other, or allow market share to remain constant. • This decision can be seen as game theory 21 Market Concentration • Market concentration is the extent to which supply to a market is provided by a small number of firms Market concentration ratio: • The proportion of output (or employment) accounted for by, say, the largest three, four or five producers Herfindahl index • The market share percentages of all firms in the market are squared and the squares summed – Perfect competition index=0 – Pure monopoly index= 10,000 – Used by US to control development of monopoly: indices above 1000 attract review, above 1800 most unlikely to be approved 22 Problems with measures of market concentration • Defining the market: it may appear to be competitive overall but one firm may monopolise a segment. • Entry of new firms should reduce concentration but is unlikely to affect the concentration ratio and may not affect the Lorenz curve or the Gini co-efficient 23 Public Policy & Competition Government Control • Governments intervene in microeconomic matters when market forces do not produce the outcomes they wish to see • The various aspects of market failure invite government regulation. • The extreme form of intervention is nationalisation an this may be undertaken for other reasons Other justifications for Nationalisations: • Natural monopolies should not be allowed to exploit their positions, eg utility companies • Larger groupings coul exploit further economies of scale to natural advantage (aerospace) • Only government can supply enough finance for some industries (railway networks) 24 • Political control over strategic industries (oil production) • Marxist/socialist theory: the political left is more or less uncomfortable with capitalism and wishes to control industry for the benefit of its client groups (eg coal mining) Government response to market failure • Monopoly elements: controls on prices or profits- breaking up monopoly companies • Externalities: regulations (eg to control pollution, compel car insurance, ban smoking) • Imperfect information: product safety rules, public service advertising, provision of jobcentres 25 • There has been a move away from government control of industry in many countries over the last 20 years Reasons for reducing the degree of government control • Nationalised industries being run for the convenience of their staffs rather than their customers • Civil servants and politicians not good at commercial decision making • Sale of state assets permits tax cuts and reduces need for government borrowing • Enhanced competition seen as likely to improve efficiency and promote growth • Reduction in enforcement costs and unintended consequences of regulation • Wider share ownership 26 Privatisation • It is possible to discern several strands in privatisation – 1) Deregulation, to allow private firms to compete with state-owned ones, (postal service) – Contracting out of government work previously done by government employees (waste collection) – Outright sale of business to private shareholders (BT) Privatisation has been criticised: – Creation of private monopolies – Sale of assets at a discount – Enhanced top executive benefits – Decline in the quantity and quality of service 27 Promoting Competition • Western governments promote competition in most areas of economic activity since it is simple and cheap way to achieve economic efficiency and growth • Competition Act 1998: anti-competitive arrangements are necessarily against the public interest and so should be illegal • Enterprise Act 2002: This act makes operating a cartel a criminal offence in the UK • The Uk Competition Commission: investigates mergers and market share over 25% 28 Finance & Financial Intermediaries Functions & Qualities of Money • 4 Main functions: – – – – Medium of exchange Act as a store of value (impaired by inflation) Unit of account Standard of deferred payment Qualities of money: – – – – – Durability Acceptability of both buyers and sellers in a transaction Transportability Maintains a stable value and purchasing power (reduced by inflation) Not easily counterfeited 29 The flow of funds Households Firms • • • • Government Funds flow between the three main parts of the economy Households, firms and governments borrow in order to obtain funds in addition to income Funds may be used for capital investments or to cover a gap in the flow of income Households and firms may have a surplus of income that they are prepared to lend in order to earn interest 30 • Governments also lend, but mostly in order to finance activity they wish to promote, rather than to earn interest Solvency requires a balance between income and expenditure but payments and receipts cannot always by synchronised since there may be irregularity of income and expenditure will cover both small and large items (see table 1 below) 31 Table 1 Reason for Irregularity of income Reasons for peaks of expenditure Households Variations in fees & overtime: causal Household purchase; labour; periodic receipt of investment holidays; property income maintenance; major purchases Firms Seasonal and cyclical variations in trade receipts; periodic receipt of investment income Capital expenditure; tax payments; finance of working capital Governments Seasonal and cyclical variation in tax receipts Seasonal & cyclical variation in welfare & other payments; natural disasters and other contigencies 32 Financial Intermediation • Financial intermediaries provide the facilities and financial instruments to transfer funds from surplus units, or lenders, to deficit units or borrowers in the business, personal, overseas & government sectors • Clearing or retail banks provide banking services to the public • Investment banks or “merchant banks” provide advice and major finance to corporate clients • Insurance companies, pension funds, unit trusts & investment trusts make longer term investments for clients Functions of Financial Intermediaries • Aggregation: relatively small deposits can be combined into major loans for borrowers • Maturity transformation: by receiving a constant flow of savers and lending to a large number of borrowers, intermediaries can spread risk of any non-payment of debt, whereas that risk may have been too high for an individual 33 lender to lend to a single borrower • Source of funds: borrowers are assisted to obtain the funds they need Financial Instruments Borrowing Lending Short Term Short Term Overdraft Deposit a/c Bills of exchange payable Money market Bills of exchange receivable Medium Term Medium Term Bank loans Term deposits Hire purchase Certificates of deposit Finance leases Bank loans Long Term Long Term Debentures Bank loans Mortgages Mortgages Equity (way of raising capital) Equity Bank loans Debentures 34 Institutions & Markets Capital Markets: • London stock exchange – 1) Main market; with firm regulation, for raising funds through new issues of shares and trading existing shared – Alternative Investment Market: for newer companies, less firmly regulated • Gilt edged market for UK government stock • International capital markets are operated between banks in larger countries to provide major finance for very large companies and institutions. Confusingly, their securities are known as Eurobonds • Certain stocks not traded on recognised stock exchanges are traded in over the counter markets 35 Money Markets: • Short term investment and borrowing of funds is handled on the money markets. These are operated by the banks and other financial institutions and include markets for: – – – – – Certificates of deposit Bills of exchange and commercial paper Treasury bills Building society bulk borrowing Local authority bills and other short term borrowing 36 Insurance • Insurance transfers risk from one party to another, in return for a payment, called a premium. Insurance companies are intermediaries in the risk market • An underwriter is a person who estimates and accepts risk, normally on behalf of an insurance company or other risk bearer • Assurance deals with risk of something definitely happening 37 Credit & Banking Banks & Credit Functions of Commercial Banks: • Payments mechanism: payments made by cheque cleared and net balances transferred via banks’ deposits at the central bank • Storage & safeguarding of wealth: most accounts attract interest • Lending money: earn income by charging interest • Financial Intermediation • Business Services: foreign exchange dealing; bill discounting; business advice; insurance broking...etc 38 Banks & Assets & Liabilities: • Banks aim to use money in their possession to make profits. At the same time they have to ensure the security of their assets and maintain sufficient liquidity to meet their customers’ requirements for cash. They therefore maintain an asset structure of graduated liquidity & profitability • Cash: – – – – Market loans Bills (usually repayable in 90 days) Advances (term loans) Investments More Liquid Less Liquid • Central banks use the Basle Agreement rules on capital adequacy to supervise their banks and ensure they have sufficient provision for bad debts 39 The Credit Multiplier • The bank or credit multiplier is the name given to banks’ ability to create credit and hence money, by maintaining their cash reserves at less than 100% of the value of the deposits they hold The basics of credit creation: – The total amount of money in a modern economy is many times the amount of cash in circulation – A bank receiving a deposit is able to lend most of it out, retaining only a small proportion to meet the depositor’s needs – The money lent is in turn deposited and supports a further loan 40 Calculating the credit multiplier • The relationship between the amount of a deposit and the credit that can be based on it is called the credit multiplier and takes the form: Deposits= Cash/Cash Ratio or D=C/R • Where the cash ratio is the % of the cash deposited the bank feels is prudent not to lend. • Thus with a cash ratio of 20%, a cash receipt of 1,000euro can support total deposits of 5,000euro • The 1,000euro originally paid in and 4,000euro credited to borrowers’ accounts. 41 Yield • There are two aspects of yield on an investment: – Interest (on dividends) – Capital Growth • Interest is paid separately from repayment of the principal. Capital growth can only be realised when the investment is repaid or sold • Bonds normally pay a fixed rate of interest: this is the nominal or coupon rate. Running or current yield on a bond is found by dividing its market price into its nominal rate • Net dividend yield on equities is similar: current share price is divided into the annual net dividend income • Bills of exchange and other bills such as treasury bills provide yield by being offered at a price lower than their maturity or face value: the bill rate is thus a measure of capital growth • Yield Maturity includes both interest and capital appreciation 42 43 The Term Structure of Interest Rates R% This normal yield curve illustrates the way interest rates vary with the term of the loan. There is greater risk of losses from default and inflation the longer the term of the loan . Longer term loans therefore attract higher interest rates Term 44 • The normal yield curve rises in the longer term – – Increased uncertainty about the more distant future increases the risk premium Investors wish to avoid being locked into low yields in case interest rates generally rise • Reverse yield curves indicate market expectation of future interest rate reductions 45 The Central Bank • A country’s central bank plays a vital role in the management of the monetary system. • The functions of any given central bank may vary from those of another, especially in the areas of monetary policy and financial supervision. Functions of The Central Bank: • Provides a banking service to the government • Central note issuing authority • Manages the National Debt • Lender of last resort • Banker to the commercial banks, holding operational deposits to permit interbank transfers: can require special deposits to control money supply • Manages national foreign currency reserves • Monetary Policy Committee sets the UK benchmark interest rate 46 Setting the Interest Rates • The bank’s interest rate policy must also take account of the need to expand the money supply to support economic growth 47 Key points from Section B to know for the assessment (i) identify the equilibrium price in a product or factor markets likely to result from specified changes in conditions of demand or supply; (ii) calculate the price elasticity of demand and the price elasticity of supply; (iii) identify the effects of price elasticity of demand on a firm’s revenues following a change in prices; (iv) explain market concentration and the factors giving rise to differing levels of concentration between markets; (v) explain market failures, their effects on prices, efficiency of market operation and economic welfare, and the likely responses of government to these; (vi) distinguish the nature of competition in different market structures; (vii) identify the impacts of the different forms of competition 48 on prices and profitability. Key points from Section C to know for the assessment (i) identify the factors leading to liquidity surpluses and deficits in the short, medium and long run in households, firms and governments; (ii) explain the role of various financial assets, markets and institutions in assisting organisations to manage their liquidity position and to provide an economic return to holders of liquidity; (iii) explain the role of insurance markets in the facilitation of the economic transfer and bearing of risk for households, firms and governments; (iv) explain the role of the foreign exchange market and the factors influencing it, in setting exchange rates and in helping organisations finance international trade and investment; (v) explain the role of national and international governmental organisations in regulating and influencing the financial system, and the likely impact of their policy instruments on businesses. 49