Chapter 6 PPT

advertisement

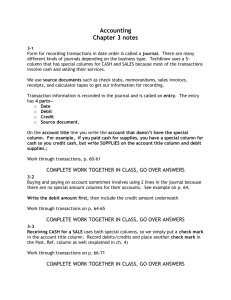

Chapter 6 Worksheet for a Service Business Today in Accounting, 12/15/14 • Get a copy of the book! Open to Page 157 • Be prepared to understand the • • purpose of adjustments and the correct way to record them in the worksheet! We will then review how to create the worksheet You will use the rest of class to retake the test or complete makeup work Terminology fiscal period-the length of time for which a business summarizes and reports financial information. work sheet-a columnar accounting form used to summarize the general ledger information needed to prepare financial statements. trial balance-a proof of the equality of debits and credits in a general ledger. Explanation Reporting accounting information for a fiscal period is very important…Why ???????? A fiscal period can begin on any date. However, most businesses begin their fiscal periods on the first day of a month. PREPARING THE HEADING OF page 153 A WORK SHEET 1 2 Name of Company Name of Report 3 Date of Report A WORK SHEET IS A PLANNING DOCUMENT PREPARING THE HEADING OF page 153 A WORK SHEET ALL FINANCIAL STATEMENT HEADINGS ANSWER THE QUESTIONS: WHO? WHAT? AND WHEN? A WORK SHEET IS A PLANNING DOCUMENT 6 PREPARING A TRIAL BALANCE ON A WORK SHEET •ALL ACCOUNTS ARE LISTED IN CHART OF ACCOUNTS ORDER ON A WORK SHEET WHETHER THEY HAVE A BALANCE OR NOT. •ACCOUNT TITLES ARE WRITTEN IN FULL UNLESS THERE IS NOT ENOUGH ROOM. IF THERE IS NOT ENOUGH ROOM, ABBREVIATIONS CAN BE USED •ACCURACY IS IMPORTANT WHEN COPYING ACCOUNT BALANCES TO THE WORK SHEET COLUMNS PREPARING A TRIAL BALANCE ON A WORK SHEET page 154 2 1 3 5 8 1. Write the general ledger account titles. 2. Write the general ledger debit account balances. Write the general ledger credit account balances. 3. Rule a single line across the two Trial Balance columns. 4 4. Add both the Trial Balance Debit and Credit columns. 5. Write each column’s total below the single line. 6. Rule double lines across both Trial Balance columns. 6 Question for YOU! How have we accounted for supplies up to this point? Answer: We have increased the asset account, Supplies, when we purchase supplies. We have NOT recorded the use of supplies. Today we will stress that if this continues, the balance in the supplies account will get larger and larger, even though supplies are being used each period. New VOCAB TERM ADJUSTMENTS: changes recorded on a work sheet to update general ledger accounts at the end of a fiscal period. (p. 157) Today’s lesson will discuss how to analyze adjustments for supplies and prepaid insurance. Don’t look too excited! Lesson 6.2 The concept Matching Expenses with Revenue means that amounts that helped earn revenue for a period must be reported as expenses in the same period. Again, Today we are going to look how adjustments are made for supplies and insurance. These adjustments will be planned on the work sheet. Good Habits You should establish the habit of asking the four questions to analyze each adjustment. 1.What is the balance of Supplies? 2.What should the balance be for this account? 3.What must be done to connect the account balance? 4.What adjustment is made? SUPPLIES ADJUSTMENT ON A WORK SHEET Supplies Account Balance – Supplies on Hand= Supplies Used $1025.00 - $310.00 = $715.00 SUPPLIES ADJUSTMENT ON A WORK SHEET page 158 2 3 1 1. Write the debit amount. 2. Write the credit amount. 3. Label the two parts of this adjustment. 14 PREPAID INSURANCE ADJUSTMENT ON A WORK SHEET Prepaid Insurance Balance – Insurance Coverage Remaining (Unused) = Insurance Coverage Used $1200.00 - $1100.00 = $100.00 PREPAID INSURANCE ADJUSTMENT ON A WORK SHEET page 159 2 3 1 1. Write the debit amount. 2. Write the credit amount. 3. Label the two parts of this adjustment. 16 PROVING THE ADJUSTMENTS COLUMNS OF A WORK SHEET •Reminder: If Debits equal Credits for each adjustment, the total debits and total credits in the Adjustments columns must also equal. •There are three steps for proving the Adjustments columns of a work sheet…. PROVING THE ADJUSTMENTS COLUMNS OF A WORK SHEET page 160 1 2 1. Rule a single line. 2. Add both the Adjustments Debit and Credit columns. Write each column’s total. 3. Rule double lines. 18 3 PREPARING A WORK SHEET page 160 C 1. Write the heading. 2. Record the trial balance. 3. Record the supplies adjustment. 4. Record the prepaid insurance adjustment. 5. Prove the Adjustments columns. 6. Extend all balance sheet account balances. 7. Extend all income statement account balances. 8. Calculate and record the net income (or net loss). 9. Total and rule the Income Statement and Balance Sheet columns. 19 20 1 21 1 2 496400 10000 15000 10000 102500 120000 6 (a) (b) 71500 10000 20000 5000 500000 62500 4 356500 356500 21300 (b) 10000 (a) 71500 2800 30000 11000 881500 881500 8 81500 21300 10000 7 2800 30000 71500 5 11000 81500 146600 356500 734900 525000 209900 209900 356500 356500 734900 734900 9 22 20000 5000 500000 3 62500 Net Income 496400 10000 15000 10000 31000 110000 The Difference Is 1 • For example, if the totals of the two columns are debit $14,657 and Credit $14658, the difference between the two columns is $1.00. The error is most likely in addition. • Add the columns again. The Difference Can Be Divided Evenly By 2 • For example, the difference between two column totals is $48, which can be divided by 2 with no remainder. Look for $24 amount in the Trial Balance columns of the work sheet. If the amount is found, check to make sure it has been recorded in the correct Debit or Credit column. The Difference Can Be Divided Evenly By 2 • A $24 debit amount recorded in a credit column results in a difference between column totals of $48. • If the error is not found on the work sheet, check the general ledger accounts and journal entries. An entry for $24 may have been recorded in an incorrect column in the journal or in an account. The Difference Can Be Divided Evenly by 9 • For example, the difference between two columns is $45. which can be divided by 9 with no remainder. When the difference can be divided equally by 9, look for transposed numbers such as 54 or 19 written as 91. • Also, check for a “Slide”. A “Slide” occurs when numbers are moved to the right or left in an amount column. For example, $12 is recorded as $120 or $350 is recorded as $35. The Difference Is An Omitted Account. Look for an amount equal to the difference. If the difference is $50, look for an account balance of $50 that has not been extended. Look for any $50 amount on the work sheet and determine if it has been handled correctly. Look in the accounts and journals for a $50 amount and check if that amount has been handled correctly. Failure to record a $50 account balance will make a work sheet’s column totals differ by $50. Checking For Errors in the Work Sheet. 1.Check for Errors in the Trial Balance Column 2.Check for Errors in the Adjustment Columns 3.Check for Errors in the Income Statement and Balance Sheet Columns. Check for Errors in the Trial Balance Column 1.Have all general ledger account balances been copied in the trial balance column correctly? 2.Have all general ledger account balances been recorded in the correct Trial Balance Columns? Check for Errors in the Adjustment Columns Do the Debits equal the Credits for each adjustment? Use the small letters that label each part of an adjustment to help check accuracy and equality of debits and credits. Is the amount for each adjustment correct? Check for Errors in the Income Statement and Balance Sheet Columns. Has each amount been copied correctly when extended to the Income Statement or Balance Sheet column? Has each account balance been extended to the correct Income Statement or Balance Sheet columns? Has the net income or net loss been recorded in the correct Income Statement or Balance Sheet columns? Has the net income or net loss been recorded in the correct Income Statement or Balance Sheet Columns. POSTING TO THE WRONG ACCOUNT 2 page 168 Correct entry 1 Incorrect entry 1. Draw a line through the entire incorrect entry. Recalculate the account balance and correct the work sheet. 2. Record the posting in the correct account. Recalculate the account balance, and correct the work sheet. 32 CORRECTING AN INCORRECT AMOUNT page 169 2 1 3 1. Draw a line through the incorrect amount. 2. Write the correct amount just above the correction in the same space. 3. Recalculate the account balance, and correct the account balance on the work sheet. 3 Steps for correcting an incorrect amount in the account. 33 CORRECTING AN AMOUNT POSTED TO THE WRONG COLUMN 2 1 3 5 4 6 4. Draw a line through the incorrect item in the account. 5. Record the posting in the correct amount column. 6. Recalculate the account balance, and correct the work sheet. 34 page 169 Check Your Understanding • What is the first step in checking for arithmetic errors when two column totals are not in balance? • What is the one way to check for an error caused by transposed numbers? • What term is used to describe an error that occurs when numbers are moved to the right or left in an Amount Column. Check Your Understanding • What is the first step in checking for arithmetic errors when two column totals are not in balance? • Subtract the smaller total from the larger total to find the difference. Check for Understanding. What is the one way to check for an error caused by transposed numbers? Answer- The difference between the two column totals can be divided evenly by 9. Check for Understanding •What term is used to describe an error that occurs when numbers are moved to the right or left in an Amount Column. Answer: A slide Aplia • Work Together 6-4 •On Your own 6-4 •Application 6-4 •Chapter 6 Study Guide •Century21accounting.com Tutorial Test for Chapter 6 Exit Ticket •