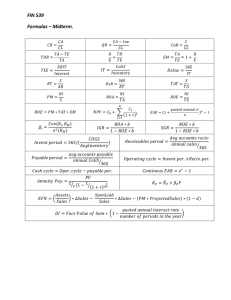

ppt - CRE Learning Home

advertisement

S1 AUTOMATED GROUP LEARNING (AGL)

AGL NO. 10 FINANCIAL MANAGEMENT

OF WORKING CAPITAL

DAILY WORK PACK - PART I

Copyright: RGAB/PW 2005/13

AGL

S2 WELCOME TO THE PROGRAM

a. AGL - two/three days of learning, tested with over 2000

managers in twenty countries around the world.

b. Helps you to understand and use the reports issued

by your finance and accounting division.

c. Provides a controlled learning environment where you

find the answers to all your questions in the groups

and materials provided.

e. Requires hard work, but you have fun and learn a lot.

S3 ABBREVIATIONS

IND

SG

CSG

MG

ASS

PL

L

D

LRT

CAI

-

INDIVIDUAL

SMALL GROUP

COMBINED SMALL GROUP

MAIN GROUP

ACCOUNTING STEP BY STEP

PROGRAM LEARNING

LECTURE

DISCUSSION

LEARNING RECALL TAPE

COMPUTER ASSISTED INSTRUCTION

S4 ASSIGNMENT 1.0 - INTRODUCTION

(30 minutes) 1.1 SPECIFIC OBJECTIVES

The program provides members with the opportunity to

understand financial management terms, techniques and

reports so that they become more complete managers.

This broadening of knowledge and skills will enable them to

capitalise on business opportunities and to accelerate their

career development.

S5 1.1 SPECIFIC OBJECTIVES

a.

Understand accounting language and the concepts of

financial management.

b.

Recognize the need for financial forecasting of : cash,

funds, income statements and balance sheets.

c.

Develop practical skills in using financial data to manage

working capital effectively.

d.

Recognize "creative accounting" in financial reporting,

despite IAS (International Accounting Standards) and

motivate further study in the future

S6 1.2 AUTOMATED GROUP LEARNING

(AGL)

The AGL method is designed to achieve rapid

individual learning using special materials and the

stimulus of group activity without a formal instructor.

The groups use the materials to find the answers to

all problems and questions.

S7 1.3 GROUP ARRANGEMENTS

The work will be done:

IND - Individually, or in

SG - Small Group (in small groups of four members

which will change daily), or in

CSG - Combined Small Group (two small groups

together), or in

MG - Main Group (for short taped lectures on key

learning points with visual aids).

S8 1.4 SG - SMALL GROUPS

Group names provided on the flip charts.

Please note the name of your SG and names

of the other members.

S9 1.5 LEARNING MATERIALS

(a) Retained by members

Text

Notebook - for recording every key point

Daily Course Diary

Learning Recall Tape

Articles (2)

(b) Used but not retained by members:

Daily work packs including: lectures, cases,

exercises and key learning points.

S10 1.5 LEARNING MATERIALS (continued)

Use your notebook. Do not mark the Daily Workpack

which must be handed back at the end of each day.

You receive all the materials in your SG.

Don't look ahead in the workpack until you are

specifically asked to do so!

S11 1.6 METHOD

Try to complete every task in the time allowed.

A pattern of learning methods will be used including:

• Study notes

• Case analysis

• Lectures

• Quizzes

• Learning patterns

• Homework reading

• Learning Recall Tape (LRT) & CAI

S12 1.7 LEARNING PATTERNS - REVIEW

1. Objectives

Language

Ratios

Concepts

Forecasting

Risk & Return

Working Capital

Creative Accounting

CONFIDENCE

S13 1.7 LEARNING PATTERNS - REVIEW

2. Learning

IND

SG

CSG

MG

S14 1.7 LEARNING PATTERNS - REVIEW

3. Methods

Study Notes

Lectures

Small Groups

Combined Small Groups

Cases & Exercixes

LRT

Main Group

CAI

LEARNING FOR YOU

S15 1.8 INSTRUCTIONS (15 minutes)

Assemble in SG's to introduce yourself, indicate your past

experience in finance and what you hope to contribute

to and gain from the course.

Complete the registration sheet in the Daily Course Diary.

NOTE: Please check that you have a full set of learning

materials now.

S16 ASSIGNMENT 3.0 - STUDY

(60 MINUTES)

3.1 INSTRUCTIONS - INDIVIDUAL WORK

a.

Re-assemble in SG and study the lecture and discuss in

SG.

b.

Record significant points on the flip chart.

c.

Review the glossary for any difficulties with new words

d.

Record significant points in your noteboo and ssemble

in MG when the bell rings

S17 ASSIGNMENT 4.0 - LECTURE ON

FINANCIAL MANAGEMENT

4.1 METHOD

Read aloud, listen carefully and respond verbally to

any questions.

S18 4.2 FINANCIAL MANAGEMENT

a.

Deals with four major problems:

SIZE - what size should the firm be?

GROWTH - what rate of growth of sales, assets, cash

flow, profits. etc.?

FINANCING - how should the firm be financed, and

at what risk?

INVESTMENT - what kind of assets should be acquired,

and at what rate?

S19 4.2 FINANCIAL MANAGEMENT

(continued)

b.

Most important is ... CASH FLOW and SURVIVAL ...

to increase the long term VALUE of the business for ALL

of the "players": customers, shareholders, management,

workers, suppliers, banks, communities, government,

trade unions, environmental groups etc

S19A 4.2

FINANCIAL MANAGEMENT

(continued)

c. To achieve EVA in a company, the manager of each

division must produce:

OP/NAE X 100% = above CoC

where:

OP = Operating Profit after tax

NAE = Net assets employed (FA & CA & OA less CL)

CoC = Cost of Capital

S19B 4.2 FINANCIAL MANAGEMENT

(continued)

d. The value of a business or a share may be simply

computed as: OCF/(r-g) which is explained later.

In 1995, shareholders may be powerful pension funds,

insurance companies and mutual funds, who may

REQUIRE management to provide both dividends and

increased share value ... or move over ...

S20 4.3 FINANCIAL OBJECTIVE,

METHOD AND SKILLS

a.

business with EVA (Economic Value Added) and SVA

(Share Value Added).

b.

Method - raise money and use it effectively to achieve

standards of financial performance

c.

Skills - risk evaluation, raising cash, using time effectively,

and maintaining relationships with the “stakeholders”:

customers, employees, owners, bankers, financial

markets. government, auditors, community etc.. by

developing appropriate attitudes towards risk- taking.

Objective - increase the long term value of the

S21 4.4 SHORT AND LONG TERM

FINANCIAL MANAGEMENT

a. Diagnosis to determine whether business has a short

term or long term need for funds

b. Short term:

1. Investment in cash, receivables (debtors) and inventory

(stock)

2. Finance from payables (creditors). advances. bank

loans etc.

S22 4.4 SHORT AND LONG TERM

FINANCIAL MANAGEMENT (continued)

c. Long term

1. Investment in fixed assets, investments, R&D. etc.

2. Finance by long term loans or equity.

Note: NET working capital is:

current assets less current liabilities.

S23 4.5 FINANCIAL ANALYSIS

Use the LAPP system to evaluate the health

of a business:

Rough Standard

Liquidity (and Gearing):

Quick assets : quick liabilities

1/2 : 1

Current assets : current liabilities

2:1

Equity : debt

2 ; 1 or 1 : 1

ActivityS/A (times turned over)

Cost of goods sold/Inventory

Days of Sales

Days of Purchases

1+

2-50

30-90

30-90

S24 4.5 FINANCIAL ANALYSIS (continued)

Rough Standard

Proftability:

Gross profit/sales x 100%

Net profit/sales x 100%

Net profit/owners equity x 100%

Operating profit/assets empluyed

improving

improving

improving

greater than CoC

Note:

Rough standards are not adequate!

Relate ratios to industry averages.

Look at past trends, compare with target.

Forecast forward to see the future effect of operations!

S25 4.5 FINANCIAL ANALYSIS (continued)

Potential:

Sales

Products

Markets

Facilities

Finance

Organization

Research

etc.

S26 4.6 FORECASTING FUNDS

Funds flow shows source and use of funds.

Sources are: profit, depreciation, new capital and loans.

Uses are: fixed assets, dividends, working capital.

Funds flow statements reveal key management decisions past and future.

Forecast forward to provide funds as required 1 - 5 years

ahead.

S27 4.7 FORECASTING - CASH

Arrange now for the cash required in the future.

Cash flow is cash (received and paid) in the shorter term.

Continually re-forecast monthly for 12 months ahead to be

sure cash is available when required.

Some businesses need weekly or even daily cash forecasting

and control due to seasonal fluctuations of the industry.

Review the past cash flows against target, and plan future

cash flows.

S28 4.7 FORECASTING - CASH (continued)

Look for peak requirement and duration - watch seasonal

and monthly effects.

Don't keep too much cash in hand earning nothing.

Debt capacity (equity: debt relationship) is real KEY to

liquidity.

The quick ratio and current ratio are only part

of the story!

S29 4.8 MANAGEMENT OF

WORKING CAPITAL

(a) Manage the assets and sources of finance:

(b) Assets:

Cash - reduce amount on hand, get it to the bank faster!

Inventory - reduce inventory or get suppliers to hold it!

Research high values and slow moving items ...,

S30 4.8 MANAGEMENT OF

WORKING CAPITAL (continued)

Receivables - reduce by credit control, expediting

payment, cash discounts, change of customers,deposits,

factoring, etc.

Identify the long paying receivables. Research the reasons

why ... Invoice errors? Credit note delays? Documents ?

Forex? Special needs? ...

Get all the managers (marketing, production, finance etc.)

to “own” the WC problem ....

S31 4.8 MANAGEMENT OF

WORKING CAPITAL (continued)

(c) Liabilities:

Suppliers - "stretch" but don't miss discounts; get longer credit;

seek alterative suppliers?

Banks - borrow more from the same or several banks?

Leasing - lease rather than buy fixed assets, to release cash

for working capital.

S32 4.8 MANAGEMENT OF

WORKING CAPITAL (continued)

Management of short term working capital is the

management of CASH FLOW.

Watch out for contingent liabilities for: FOREX, legal and

environmental claims, lease payments etc.

S33 4.8 MANAGEMENT OF

WORKING CAPITAL (continued)

(d) Cash is vital - so many businesses that go bankrupt

are making a profit - they just run short of cash. Cash

needs vary at different times both within the month

and the season.

(e) Plan for sustainable positive OCF (Operational Cash Flow)

which provides for : increase in working capital needs

and “normal” new capital expenditure, A positive OCF

makes cash available for new profitable investments

that give EVA.

S34 4.8 MANAGEMENT OF

WORKING CAPITAL (continued)

(f)

"Benchmark" with other companies to set new WC

performance standards,

Get ALL managers (production, marketing and finance)

to "own" the working capital problem!

S35 4.9 CHECK LIST ON

ANNUAL REPORTS

Be careful with company's annual reports; evaluate

reports using a check list:

(a)

(b)

(c)

(d)

(e)

(g)

(h)

Cash, orders and activity

Profitability, prospects and resources

Long term finance

Shareholders and management

Exceptional transactions and notes to the

financial statements

Secret reserves and contingent liabilities for :

leasing, legal, environment, FOREX and INTEREST

DERIVATIVES etc.

Check for reconciliation of net profit with IAS.

S36 4.10 SIMPLIFIED COST OF CAPITAL,

EVA AND SVA

(a)

In very simple terms, the Cost of Capital is the average

after-tax cost of raising long term funds for the business.

(b) Such funds can come either from long term debt

(liabilties) or equity. Normally debt (say 8%) costs less

than equity (say 16%).

(c) Hence the E:D ratio set by Management (2:1 or 1:1 or

1:2) can affect the average Cost of Captial (say 13.3%

or 12% or 9.3%).

S37

(d)

4.10 SIMPLIFIED COST OF CAPITAL,

EVA AND SVA (continued)

EVA (Economic Value Added) is produced when the

net assets employed (A-CL) produce an OCF after

tax (say 12%) which is greater than the Cost of

Capital (say 9.3%).

S38

4.10 SIMPLIFIED COST OF CAPITAL,

EVA AND SVA (continued)

EVA (Economic Value Added) is produced when the net

assets employed (A-CL) produce an OCF after tax (say 11%)

which is greater than the CoC (SAY 9.3%).

EVA may be simply computed as V = OCF/(r-g), where:

OCF

r

g

V

= Operating Cash Flow (say 100)

= Cost of Captal (say 9.3%)

= Growth Rate (say 5.3%)

= 100/(0.93-0.53) = 250

S39 4..10 SIMPLIFIED COST OF CAPITAL,

EVA AND SVA (continued)

(e)

(f)

SVA (Share Value Added) is produced when the

sustainable cash flows and dividends lead to

increased short term and long term share value.

Most companies control capital expenditure well

but fail to control investment in WC which is cr is

critical to achieving EVA and SVA.

S40 4.11 OVERALL (continued)

Plan short term cash and long term needs.

Set financial management objectives.

Manage the WC or it will manage itself - very badly!!

Seek SEVEN alternatives before setting financial policies.

Ensure that short term plans have good long term effects.

S41 4.11 OVERALL (continued)

Watch for daily, weekly, monthly and seasonal fluctuations in

cash needs!

Seek creative not merely routine financial management.

Always use good financial forecasts 1-3 years ahead ... with

the key underlying assumptions clearly outlined.

S42

4.11 OVERALL (continued)

There are always SEVEN alternatives ...

for every financial problem ...

so, seek them out ... before ...

you make that final decision ...

and ... do a PFD ... before you make the commitment ...

S43 4.12 LEARNING PATTERNS - REVIEW

1. FINANCIAL MANAGEMENT

• SIZE

• GROWTH

• FINANCING

• INVESTMENT ......................... FOR EVA/SVA

S44 4.12 LEARNING PATTERNS - REVIEW

2. W C MANAGEMENT

• SOURCES - P and I

• USES

- C, R and I

S45 4.12 LEARNING PATTERNS - REVIEW

3. FINANCIAL ANALYSIS

•

•

•

•

L&G

A

P

P

S46 4.13 INSTRUCTIONS (10 MINUTES)

(a) Reassemble in SG.

(b) Study the lecture very carefully and record key

points in your notebook.

(c) Discuss any outstanding questions in SG.

(d) When the bell rings carry on with the case study

which follows.

S47 ASSIGNMENT 6.0 LECTURE

PENELOPE TIMBER CO. (PTC)

6.1 STORY OF THE CASE

PTC an owner operated wholesale timber merchant of good

reputation with two buildings, 20 employees, no sales

representatives and annual staff bonuses of 40% of salaries.

Increased sales lead to increased receivables and inventory

financed by a bank loan and stretching of payables; sales

discounts increase but shortage of cash prevents taking

purchase discounts.

Should further planned expansion be financed by bank loans

S48 6.2 FINANCIAL HEALTH

a. Liquidity & Gearing :

Quick ratio and current ratios below industry average.

Equity: debt only .5:1 (industry 1:1)

Bank loan 48,000 insufficient to allow taking purchase

discounts; payables stretched; cash extremely short.

S49 6.2 FINANCIAL HEALTH

(continued)

b. Activity:

Sales/assets ratio above average but inventory turnover

weaker;

Receivables 38 days (industry 30 days) and payables 85

days (industry 20 days).

Very active company possibly over trading for its low equity

base.

S50 6.2 FINANCIAL HEALTH

(continued)

c. Profitability:

Gross profit percentage to sales falling (12.2%) but up to

industry average (12%).

Net profit to owners equity good; very profitable company

even after charging very high staff bonuses!

S51 6.2 FINANCIAL HEALTH

(continued)

d. Potential:

Sales potential good, facilities and staff adequate,.

Management good.

But finance probably inadequate for the planned

expansion.

S52 6.3 FUNDS FLOW & OCF

Funds flow indicates key management decisions on sources

and uses of funds; no additional capital.

Very little expended on fixed assets and nothing on

dividends.

Funds flow confirms the need for further funds to finance a

higher level of activity. Will substantial new fixed assets also

be necessary soon?

OCF confirms poor EVA focus.

S53 6.4 EFFECT OF SALES EXPANSION

ON FINANCIAL HEALTH

Sales increase naturally lead to increase in receivables

and inventory; high sales cash discounts allowed to

get cash quickly.

Increased profits substantially distributed to employees

as bonus leaving relatively little in the business to

finance expansion.

In the past assets were financed equally by equity

and debt (1:1) but in the last year financed mainly by

liabilities (.5:1).

S54 6.4 EFFECT OF SALES EXPANSION

ON FINANCIAL HEALTH (continued)

Higher leverage and risk of failure!

Sales and profit expansion has led to high profitability,

high risk and relatively poor financial health.

Cost of losing purchase discounts of 2% 10 days net

30 days is 2%, for the additional 20 days of credit

i. e. 36% per annum (365/20 x 2%) ...

... but only 4% if the 30 days become 182 days

... 365/182 x 2% = 4% ...

S55 6.5 NEW FORECASTS AND CASH

REQUIREMENTS

Underlying assumptions may prove to be not valid:

(a) Gross profit optimistic 14% (last year 12.2%,

industry 12%).

{b) Receivables 30 days (last year 30 days).

(c) Inventory turnover 5 times (last year 4 times).

(d) Bank loan for 48, 000 may not continue.

NOTE: Forecast shows need of 64,000 but the existing bank

may withdraw, thus creating a need for more than 112, 000.

Can the company afford to give away so much in sales cash

discounts?

S56 6.6 PROVIDING NECESSARY CASH

(a) Asset Management

Cash - reduce the minimum cash balance?

Receivables - reduce by: selecting better paying customers,

expediting more efficiently, billing on time, changing the

cash discount policy, site research visits, error free invoicing,

rapid credit note processing, benchmarking, and getting all

managers to "own" the problem.

S57 6.6 PROVIDING NECESSARY CASH

(a) Asset Management (continued}

Inventory - reduce by: getting suppliers to hold inventory,

cutting back on requirements, standardisation, JIT, site

research visits, benchmarking, and getting all managers

to "own" the problem.

S58 6.6 PROVIDING NECESSARY CASH

(continued)

(b) New Sources

Payables well "stretched' but the discounts lost have cost

about 36% p.a. cheaper to borrow from the bank even at

10%!

Possible factoring of debtors to get immediate payment for

mounts outstanding!

Possible bank loan?

NOTE: Overall, to what extent can planned expansion be

cut back to reduce need for funds?

S59 6.7 FINANCIAL PROBLEMS AND

ALTERNATIVES

Difficult to determine whether the problem is short

term or long term without a five year financial forecasts.

Initial forecast shows need for at least 64,000 of

additional funds.

S60 6.7 FINANCIAL PROBLEMS AND

ALTERNATIVES (continued)

Profits must be retained in the business to reduce reliance on

suppliers (to avoid stretching payables excessively and to

take purchase cash discounts).

Equity: debt relationship of .5:1 is below industry average and

therefore not healthy.

Could be accepted as a "bridging situation" depending long

term finance from profits or new equity; will further fixed

assets be necessary with the increasing turnover?

S61 6.7 FINANCIAL PROBLEMS AND ALTERNATIVES

(continued)

Alternatives available: bank, suppliers, factoring, mortgage,

long term loans, new equity, or reduction of assets?

NOTE: Stretching payables is only cheap after cash discounts

already lost, but rather risky; when equity: debt becomes

very weak.

Survival may depend more on suppliers than management!

S62 6.8

DECISION AND JUSTIFICATION

(a) Decision - depends upon the risk level which Penelope

will accept, his personal objectives for expansion and

the possible need to expand merely to survive.

If sales can be kept to 1,200,000 (not 1,600,000) then

receivables and inventory could be cut back

substantially and very little additional finance needed

either from banks or equity.

S63 6.8 DECISION AND JUSTIFICATION

(continued )

If, however, business expansion is vital for survival t hen

new funds must finance the increased receivables and

inventory.

Funds from banks or stretching payables is high risk

approach. A lower risk approach to expansion would be to

provide new equity funds thus increasing the equity base

and improving the general financial health.

Bank may refuse new loan and (try to) withdraw existing loan

if PTC goes to another bank.

S64 6.8 DECISION AND JUSTIFICATION

(continued)

(b) Recommendation : increase the equity base now while

the business is very profitable; alternatively get a

temporary bank loan as "bridging" finance whilst

seeking new equity.

(c) Justification there is no point in taking excessive risks

with a successful business; don't push bank too hard

too soon!

S65 6.8 DECISION AND JUSTIFICATION (continued

Don't pursue sales regardless of financial risk and

requirements.

NOTE: There are several acceptable alternative

solutions; evaluate them in terms of the level of

risk PTC should accept!

S66 6.9 LEARNING POINTS

(a) Health of the business may be determined ln

terms of liquidity (and gearing), activity, profitability

and potential.

(b) Ratios must be compared with industry averages to

determine their significance.

(c) Increased sales lead to increased working capital in

receivables and inventory.

S67 6.9 LEARNING POINTS (continued)

(d) Profits produce funds for financing increased

working capital provided they are not distributed

as dividends.

(e) Working capital may be managed either by

reducing the uses, or increasing the sources,

of funds.

(f)

Must determine whether the financial need is

short term or long term, since the solutions will differ.

S68 6.9 LEARNING POINTS (continued)

(g) Creative financing considers all alternatives before

making a decision.

h)

Cash flow, funds flow and forecasted income

statements and balance sheets help to clarify

financial needs.

(i)

Funds flow reveals key management decisions.

S69 6.9 LEARNING POINTS (continued)

(j) "Bridging" finance is short term money pending

raising of long term funds.

(k) Management must decide the level of risk that

it will accept before deciding upon the expansion

and planning the financing.

(l)

Financing of working capital easier if company

has facilities from more than one bank.

S70 6.9 LEARNING POINTS (continued).

(m) Always seven alternatives ro every finnncial problem.

(n) Cut receivables and inventories in ten ways plus

benchmarking and getting all managers to "own" the

problem.

(o) Research inventory values, turnover, standardisation,

supplier cooperation opportunities.

S71 6.10 LEARNING PATTERNS

1. SALES EXPANSION

– RECEIVABLES +

• INVENTORIES +

• CASH

-

S72 6.10 LEARNING PATTERNS

(continued)

2. SHORT-TERM TO LONG-TERM

PROFIT NOW ..... DISASTER LATER?

S73 6.10 LEARNING PATTERNS

(continued)

3. WORKING CAPITAL

MANAGEMENT

PROBLEM "OWNED" BY ALL

MANAGERS ...

S74 6.11 INSTRUCTIONS

(a) Re-assemble in CSG

(b) Study the lecture and discuss in CSG.

(c) Record significant points in your notebook

(d) Reassemble in MG when the bell rings

S75 ASSIGNMENT 7.0 - STUDY - FINANCING

EXPANSION (75 MINUTES)

7.1 INSTRUCTIONS

(a) Re-assemble in new SG, and study the lecture and

discuss in SG.

(b) Record significant points on the flip chart.

(c) Review the glossary for any difficulties with new words

(d) Record significant points in your notebook and

re-assemble in MG when the bell rings an

S76 ASSIGNMENT 8.0 - LECTURE ON

FINANCING EXPANSION

8.1 METHOD

Read aloud, listen ,,,

and respond verbally ... to any questions.

S77 8.2 PLANNING FOR THE FUTURE

Need to plan the size, growth and profit stability of the

company.

Funds flow is the key to long term financing.

Cash flow is the key to short term financing.

Forecast forward both cash and funds to determine

whether financial needs are short term or long term.

S78 8.3 RISK AND THE CRITICAL FEW

Decide upon "critical few" factors which really make

for profit in the particular business. Analyze the industry,

economy, size of the business and finally the personal

values of the chief executive.

Determine the risk level the company will accept.

Evaluate the risk of various possible disasters.

Set financial policies to deal with the "critical few"

profit-making features at the appropriate risk level.

S79 8.4 EFFECT OF EXPANSION

Expansion of sales leads naturally to expansion

of current assets (receivables, inventory and the

minimum cash balance).

Management of receivables and inventory is the

cheapest "source" of finance, i.e. reduce the

investment.

S80 8.4 EFFECT OF EXPANSION (continued)

Suppliers may provide “cheap finance” with or without

cash discounts.

Loss of cash discounts is costly - i.e. 2% 10 days net 30 days, is

2% for the extra 20 days of credit or 36% per annum!!

Alternative sources of short term finance include: other

suppliers, factoring, loans. customer deposits,banks, etc.

Get suppliers to give 2% 30 days or take 9 months to pay or

change suppliers?

S81 8.5 BANK RELATIONSHIPS

Commercial banks serve customers by financing current

business (not like merchant banks which provide long term

capital)

Key to bank financing is the mutual confidence between

banker and customer.

Bankers like: short term financing which turns over regularly;

they like "accounts" that are actively going from red to

black to red, etc.

S82 8.5 BANK RELATIONSHIPS (continued)

Banks provide a widening range of services today.

Banks believe that "the customer does not have to tell

us all the truth but he must never deliberately lie or be

irresponsible".

Commercial banks have associates that do merchant

banking.

S83 8.6 CRITERIA FOR BANK FINANCE

Commercial banks lend not just against physical security

but on the following criteria:

(a) Personal relationship with banker

(b) purpose

(c) profitability

(d) payback (is it possible?)

(e) security.

Bankers may say "all loans are repayable on demand

if the rules are broken”, but in reality they never demand it ,

unless in danger. Banks hold security in the hope of NEVER

having to use it.

S84 8.6 CRITERIA FOR BANK FINANCE (continued)

Banks give information to each other in a special code which

is discreet and confidential.

Relationship with the bank manager is the key!

Banks sometimes insist that "equity base" be increased as a

condition for further loans.

Banks are normally conservative and tough!

S85 8.7 CONTROL OF WORKING CAPITAL

Frequent (monthly) reporting with reliable financial

statements to all managers (production, marketing,

finance etc,) to get them to “own” the WC problem..

Regular and effective forecasting of peak and duration of

cash needs.

Timely financial data.

Forecast forward the income statements, balance sheets,

cash and funds flow, and then evaluate risk.

S86 8.7 CONTROL OF WORKING CAPITAL

(continued)

Never go to the banker when you need money; go

when you don't need money and arrange to have it

available when you want it.

“I need ECU 500,000. Can you handle it or should I deal

directly with your general manager?"

S87 8.8 CONTROL OF RECEIVABLES

Make frequent aging of receivables to identify slow payers

and assess DOS (days of sales) performance.

For external causes: visit selected customers to identify

the reasons for delay which may include: invoice errors,

order errors, credit claim delays, non-delivery, quality

issues, INCORRECT DOCUMENTATION etc.

For internal causes: investigate, slow invoicing, pricing

complexities, credit note delays, shipment errors, poor

expediting, discount errors, failure to drop poor accounts etc.

S88 8.8 CONTROL OF RECEIVABLES

Benchmark with other companies in collaboration with

marketing, production, quality, finance managers to

jointly: “own” the problem, set targets and monitor

progress.

S89 8.9 CONTROL OF INVENTORY

Make frequent aging of inventories to identify slow moving

high value items and to assess DOP (days of purchases)

and DOS (days of sales) performance.

For external causes: visit selected suppliers to identify

the reasons for high inventory which may include: excess

order quantities, long delivery lead times, poor

standardization, lack of JIT systems etc.

S90 8.9 CONTROL OF INVENTORY

(continued)

For internal causes: investigate delayed usage, excess

storage, lack of standardization, poor design specification,

failure to control high value items daily, excess storage

space/costs, poor standardisation, lack of JIT systems, poor

supplier selection etc.

Benchmark with other companies in collaboration with

marketing, production, quality, finance managers to

jointly: “own” the problem, set targets and monitor progress.

S91 8.10 INFLUENCE OF THE

CHIEF EXECUTIVE

Age. experience, reputation, skills, attitudes and knowledge

of the chief executive are key factors in the decision to

finance expansion by banks. suppliers or merely reduce

the working capital investment.

Overall expansion of sales involves increase in assets

employed in the business; financing of those assets is a

management decision; but there are always many

alternatives.

S92 8.10 INFLUENCE OF THE

CHIEF EXECUTIVE (continued)

"Bridging" of long term needs by short term finance

is cceptable provided the risk is clearly recognized

and there is an achievable long term plan to recover

financial health.

S93 8.10 INFLUENCE OF THE

CHIEF EXECUTIVE (continued)

May accept temporary high risk, and unhealthy financial

position provided: high profits, planned recovery of health

planned reduction of risk to "normal" level.

Note: Before every financial negotiation, always make other

contacts to work out what you could do WITHOUT the other

party ... then negotiate (gently) from strength ... not

weakness ... because you have good alternatives ...

without him/her ...

S94 8.10 INFLUENCE OF THE

CHIEF EXECUTIVE (continued)

Management have a high “ego” priority to use “excess cash”

for expansion and diversfication projects.

By contrast shareholders may have priority for EVA targets

in terms of dividends and SVA.

Thus the sharehiolders may insist that unless new acquisitions

or mergers can achieve EVA then the excess cash is bette

returned to shareholders as dividends or share buy-back

(equity reduction).

S95 8.11 LEARNING PATTERNS - REVIEW

1. BANK FINANCING

PPPP&S

S87 8.11 LEARNING PATTERNS - REVIEW

(continued)

2. CONTROL OF R & I

INTERNAL

EXTERNAL

S88 8.11 LEARNING PATTERNS - REVIEW

(continued)

3. CEO

CHIEF

CUSTOMERS

EXECUTIVE

EMPLOYEES

OFFICER

OWNERS

S89 8.12 INSTRUCTIONS (10 MINUTES)

(a) Reassemble in SG

(b) Study the lecture carefully

(c) Record key points in your notebook

(d) Discuss outstanding questions

(e) When the bell rings, carry on with the case study which

follows

S90 ASSIGNMENT 10.0 LECTURE ON LUMSDEN (A)

10.1 STORY OF THE CASE

Expansion financed by long term bank loan 140,000 capital

expenditure and 160,000 for working capital.

Lumsden commits for increased capital expenditure of about

400, 000 before consulting the bank and thus breaks the

agreement.

S91 10.2 HEALTH OF THE COMPANY

(a) Liquidity & Gearing

Quick ratio is a little weak, although stronger than previous

years; current ratio is strong.

Equity:debt ratio of 2.4: 1 is very strong indeed, both

compared with previous years and the industry.

Overall, fairly liquid and well able to meet its commitments

at the present level of operations.

S92 10.2 HEALTH OF THE COMPANY (continued)

(b) Activity

Turnover of assets and inventories fair.

Receivables better than industry average.

Payables settled with cash discounts; overall, a fairly active

company.

S93 10.2 HEALTH OF THE COMPANY (continued)

(c) Profitability

Gross profit percentage very high in the first seven months

(un-audited!).

Similarly net profit to sales higher than the industry (why?

manipulated?).

Overall return on equity is very good.

Subject to possible manipulation of inventory value (need an

audit), profitability seems very good indeed.

S94 10.2 HEALTH OF THE COMPANY (continued)

(d) Potential

Market potential good; management effective

but a little old and unreliable; production

expanding.

NOTE: Overall a healthy company, with cash and funds flow

adequate to finance current operations.

S95 10.3 FUNDS FLOW & OCF

Funds flow indicates major management decisions regarding

source and use of funds.

Only a small past increase working capital, since profits

mainly used for fixed assets and mortgage repayments.

Funds raised from the bank to finance fixed assets and

working capital expansion. Is this wise?

Substantial increase in assets financed largely by accruals

for taxes; no draining off of profits into dividends. Confirmed

by OCF.

S96 10.4 ORIGINAL BANK LOAN

Criteria for bank finance:

(a) Personal relationship with the bank Lumsden well known

to the bank for some years but a little old (health risk?).

(b) Purpose : expansion to meet outstanding orders;

market seems to warrant such expansion.

(c) Profitability : company very profitable and healthy.

S97 10.4 ORIGINAL BANK LOAN (continued)

(d) Payback no drain.off of profits into dividends;

profitability should enable payback in the time allowed.

(e) Security general security of the business including

property, inventory, etc. seems adequate for the loan.

NOTE: Lumsden well qualified for the original loan of 140, 000

for capital expenditure and 160, 000 for working capital; bank

acted wisely in making loan because it met the criteria.

S98 10.5 BANK AGREEMENT

Lumsden has broken the bank agreement because he has

committed for more than 140, 000 of new capital expenditure;

bank could call in loan immediately.

Bank only committed in Sept last year to 80, 000 outstanding;

could be repaid with no loss to the bank.

The substantial cash balance could be immediately offset

against the loan and Lumsden could get finance from

another bank or financial source.

S99 10.5 BANK AGREEMENT(continued)

New cash needed for fixed assets is 400, 000 and working

capital 160, 000, but no forecasts available for five years to

ensure these amounts will be adequate.

Is the estimate of 400, 000 reliable for a new plant? Will

160, 000 be adequate for working capital if sales increase

from 1 to 3 million?

Probably more money needed.

S100 10.6 FURTHER BANK FINANCE

(a) Criteria for a new loan:

Personal relationship with the bank :

Lumsden broke his agreement once and therefore can he

be relied upon in the future? Is the breach a serious one?

Probably not since only 80, 000 is outstanding at the moment.

Can Lumsden manage bigger plant? Labor problems? Can

he adapt to new scale of operations which is three times

what he is used to? He is quite old and may find it difficult.

S101 10.6 FURTHER BANK FINANCE (continued)

Purpose: additional plant to meet market need; Lumsden

only a "marginal supplier" and the economy might turn down.

Profitability: Lumsden still profitable but no audited

accounts available for last year.

S102 10.6 FURTHER BANK FINANCE (continued)

Payback: larger amount harder to pay back out of profits;

depends upon the general success of Lumsden and good

cash flow from profits.

Security: still fairly strong since the plant could be sold if

necessary; less security for a larger loan than a smaller one.

S103 10.6 FURTHER BANK FINANCE (continued)

NOTE: Overall, Lumsden still a good financial risk, subject to

his ability to work well with the bank and to restrain himself

from excessive expansion and meet new business

management problems!

Total money requirement probably higher because of the

uncertainty; loan terms should tryn to restrict Lumsden's

activities and require very close reporting and control.

Bank policy is to be aggressive in seeking and keeping

clients.

S104 10.6 FURTHER BANK FINANCE (continued)

(b) Alternatives open to Lumsden:

Get the money from another bank

Get loans from suppliers of equipment

Factor receivables

Lease rather than buy the plant

Raise new equity but keep control of the company

Don't expand

Sell out

NOTE: Many opportunities open to Lumsden if the bank

refuses.

S105 10.7 FINANCIAL POLICIES

(a) Lumsden

Recognize the risks involved in such extensive expansion;

play safe by increasing equity base now but keep control of

the company.

Set up alternative financial sources to avoid reliance on

one lender. Consider leasing the plant rather than buying it.

Achieve better relationship with the bank or with several

banks to provide flexibility (and strength!)

S106 10.7 FINANCIAL POLICIES (continued)

Overall accept the loan if offered, but keep to the terms

and seek equity soon while the company is still healthy

and profitable.

NOTE: ALWAYS SET UP ALTERNATIVE FINANCING ... BEFORE ...

NEGOTIATING WITH A BANK ... NEGOTIATE FROM STRENGTH ...

NOT WEAKNESS ...!!!

S107 10.7 FINANCIAL POLICIES (continued)

(b) Bank

Decide if Lumsden can be relied upon to remain a good

client; if not, reclaim the money immediately and seek

business elsewhere.

If Lumsden remains a client, give the loan provided he

also increases the equity base!

Set controls upon him in terms of monthly audited reporting

and inspection of the plant, to ensure that the bank is well

informed of developments in time.

S108 10.7 FINANCIAL POLICIES (continued)

(c) Justification

Expansion by bank finance is "bridging" until more

equity financing can be found.

In the future avoid commitment before providing

financial resources.

S109 10.7 FINANCIAL POLICIES (continued)

NOTE: Always do a PFD before activity major financial

decisions, to check again the underlying assumptions:

economic, marketing, technical, financial, management

etc. and the possible EI ...

S110 10.8

LEARNING POINTS

(a) Criteria for bank lending includes: personal relationship,

purpose, profitability, payback and security.

(b) Breach of a bank loan agreement, gives the bank the

right to reclaim money immediately and to offset all

balances.

(c) Bank confidence in the client is key to bank financing.

S111 10.8 LEARNING POINTS (continued)

(d) Many alternatives for financing of working capital

including reduction of activity, factoring, financing by

supp liers, leasing, etc.

(e) Set up alternative financial plans before negotiating a

final deal, so as to be flexible to negotiate from strength.

(f)

No need to own the whole business and keep all the

profits. Increasing the equity base of the business means

sharing: profits, risks and losses.

S112 10.8 LEARNING POINTS (continued)

(g) Financial control involves regular, reliable and timely

monthly or weekly data, audited when necessary.

(h) "Bridging" finance provides short term resources pending

long term financing arrangements.

(i)

Need financial forecasts for five years ahead to

determine whether problems are short term or long term.

S113 10.8 LEARNING POINTS (continued)

(j)

Unaudited financial statements are not reliable;

they may have been manipulated.

(k) Think creatively about financing problems and

seek out all (SEVEN) alternatives before

making a critical fianancial decision.

S114 10.8 LEARNING POINTS (continued)

(l)

Decide very carefully about the extent and

duration of the risk level to be accepted.

(m) Keep options and relationships open.

(n) Benchmark to help to set better standards for

working capital management.

S115 10.9 LEARNING PATTERNS

1. MAXIMISING GOALS

SALES

PROFITS

CASH FLOW

SVA ...

S116 10.9 LEARNING PATTERNS (continued)

2. INVESTMENT

MUST RETURN ABOVE C. OF C.

FIXED INVESTMENT - WELL CONTROLLED

WC INVESTMENT NOT CONTROLLED ...

S117 10.9 LEARNING PATTERNS (continued)

3. FINANCIAL MANAGEMENT SKILLS

TIMING ...

S118 10.10 INSTRUCTIONS

(a) Re-assemble in CSG

(b) Study the lecture and discuss in CSG.

(c) Record significant points in your notebook

(d) Reassemble in MG when the bell rings.

S119 ASSIGNMENT 11.0 - SUMMARY

LECTURE FOR PART I

11.1 FINANCIAL MANAGEMENT

(a) Deals with four major problems:

1.

2.

3.

4.

Size - what size should the firm be?

Growth - what rate of growth of sales, assets, profits. etc.?

Financing - how should the firm be financed, and at

what risk?

Investment - what kind of assets should be acquired,

and at what rate?

S120 11.1 FINANCIAL MANAGEMENT

(b) Financial health of the business depends upon

both its resources, the environment in which it operates

and its financial policies.

Financial management is dynamic and depends upon

flows or cash and funds not a static situation.

S121 11.1 FINANCIAL MANAGEMENT (continued)

(c) Most important is ... CASH FLOW and SURVIVAL ...

to increase the long term VALUE of the business for ALL

of the "stakeholders": customers, shareholders,

management, workers, suppliers, banks, communities,

government, trade unions, environmental groups etc.

S122 11.1 FINANCIAL MANAGEMENT (continued)

(d) To achieve EVA in a company, the manager of each

division must produce:

OP/NAE X 100% = above CoC

where:

OP = Operating Profit after tax

NAE = Net Assets Employed (FA & CA & OA less CL)

CoC = Cost of Capital

S122A 4.2

FINANCIAL MANAGEMENT

(continued)

(e) The value of a business or a share may be simply

computed as: OCF/(r-g) ,

(f

In quoted companies, shareholders may be powerful

pension funds, insurance companies and mutual

funds, who are highly skilled in finance ; they may

require management to provide both dividends

and increased share value ... or move over ... thus in

1995, SVA is becoming a key financial objective!

S123 11.2 OBJECTIVE, METHOD AND SKILLS

a.

Objective - increase the long term value of the

business with EVA (Economic Value Added) and SVA

(Share Value Added).

b.

Method - raise money and use it effectively to achieve

standards of financial performance

c.

Skills - timing to balance risk and reward

S124 11.3 SHORT TERM/LONG TERM FINANCING

(a) Short term finance used for: cash, receivables,

inventory. prepayments, etc.

(b) Sources of short term finance: suppliers, banks,

factoring, leasing, or reduction of the need for cash,

receivables and inventory.

(c) Long term financing deals with long term assets

and the financing of those assets by proportions

of equity and debt.

S125 11.4 FORECASTING

(a) Cash forecasting used to provide cash resources up

to one year ahead.

Concentrate on the duration and peak need within:

weekly, monthly, yearly, seasonal, etc. periods

S126 11.4 FORECASTING (continued)

Distinguish:

CF

EBIT - earnings before interest and taxes

OCF - operating cash flow - cash flow plus interest, less

working capital changes, less “normal” capital

expenditure. Often called “Free Cash Flow”

because it is cash availble for new profitable

investment opportunities.

- cash flow - net profit plus depreciation

S127 11.4 FORECASTING

(b) Funds flow reveals the key financial decisions of past

and future.

Sources of funds: profit. depreciation. new equity and

long term loans.

Uses of funds: fixed assets, dividends, repaymen

of long term loans and working capital.

Net working capital is:

current assets less current Liabilities.

S128 11.4 FORECASTING (continued)

(c) Forecasted income statements and balance sheets

reveal future financial health.

(d) Materiality is the key - concentrate on large amounts

and long time periods. Don't get involved with the

peanuts ...! Small errors don't matter at all ...!

S129 11.5 BANK RELATIONSHIPS

(a) Relationship with the banker is key to the management

of working capital.

(b) Criteria for bank loans: person, purpose, profitability,

payback, and then security.

(c) Many alternatives available to bank finance (they

may cost more): factoring, deposits. loans, leasing.

stretching creditors, other banks, etc.

(d) Old bank customers normally get better treatment

than new ones. Cultivate a relationship with your

bank manager.

S130 11.6 FINANCIAL ANALYSIS

(a) LAPP system of financial analysis: liquidity (and gearing),

activity, profitability, potential.

(b) Need to forecast cash and funds and provide

adequate flows to finance assets acquired and required.

(c) Be creative in seeking and using financial alternatives.

(d) Avoid "emotional investment"

S131 11.7 CONTROL OF WORKING CAPITAL

Frequent (monthly) reporting with reliable financial

statements to all managers (production, marketing,

finance etc.) to get them ALL to “own” the WC

problem..

Regular and effective forecasting of peak and duration of

cash needs.

Timely financial data.

Forecast forward the income statements, balance sheets,

cash and funds flow, and then evaluate risk.

S132 11.7 CONTROL OF WORKING CAPITAL

(continued)

Never go to the banker when you need money; go

when you don't need money and arrange to have it

available when you want it.

“I need ECU 500,000. Can you handle it or should I deal

directly with your general manager?"

S133 11.8 CONTROL OF RECEIVABLES

Make frequent aging of receivables to identify slow payers

and assess DOS (days of sales) performance.

For external causes: visit selected customers to identify

the reasons for delay which may include: invoice errors,

order errors, credit note claims, non-delivery, quality

issues, incorrect documentation etc.

S134 11.8 CONTROL OF RECEIVABLES (continued)

For internal causes: investigate, slow invoicing, pricing

complexities and errors, credit note delays, shipment errors,

poor expediting, discount errors, failure to drop poor

accounts etc.

Benchmark with other companies in collaboration with

marketing, production, quality, finance managers to

jointly:

1.

2.

3.

“Own” the WC problem

Set targets, and

Monitor progress.

S135 11.9 CONTROL OF INVENTORY

Make frequent aging of inventories to identify slow moving

high value items and to assess DOP (days of purchases)

and DOS (days of sales) performance.

For external causes: visit selected suppliers to identify

the reasons for high inventory which may include: excess

order quantities, long delivery lead times, poor

standardization, lack of JIT systems etc.

S136 11.9 CONTROL OF INVENTORY

(continued)

For internal causes:

Investigate delayed usage, excess storage, poor

standardization, poor design specification, failure to control

high value items daily, excess storage space/costs, lack of

JIT systems, poor supplier selection etc.

Benchmark with other companies in collaboration with

marketing, production, quality, finance managers to

jointly: “own” the problem, set targets and monitor progress.

S137 11.10 SIMPLIFIED COST OF CAPITAL, EVA AND

SVA

(a)

In very simple terms, the Cost of Capital is the average

after-tax cost of raising long term funds for the business.

(b) Such funds can be either from long term debt (liabilties)

or equity. Normally debt (say 8%) costs less than equity

(say 16%).

(c) Hence the E:D ratio set by Management (2:1 or 1:1 or

1:2) can affect the average Cost of Captial (say 13.3%

or 12% or 9.3%).

S138 11.10 SIMPLIFIED COST OF CAPITAL, EVA

AND SVA (continued)

EVA (Economic Value Added) is produced when the net

assets employed (A-CL) produce an OCF (Operating Cash

Flow) (say 11%) which is greater than the CoC (Cost of

Capital) (Say 9.3%).

EVA may be simply computed as V = OCF/(r-g), where:

OCF

r

g

V

=

=

=

=

Operating Cash Flow (say 100)

Cost of Captal (say 9.3%)

Growth Rate (say 5.3%)

100/(0.93-0.53) = 250

S139 11.10 SIMPLIFIED COST OF CAPITAL, EVA

AND SVA (continued)

(e)

SVA (Share Value Added) is produced when the

sustainable cash flows and dividends lead to

increased short term and long term share value.)

(f)

Working capital management is critical to achieving

EVA and SVA.

(g) And thus any INCREASE in working capital is an

INVESTMENT that must be justified, like any other capital

investment or acquisition, by a return, that exceeds the

Cost of Capital.

S140 11.11 DIAGNOSIS AND DECISION

(a) Recognize that every industry and trade and country

has a special tractional environment and standards of

financial management.

(b) Knowledge, attitudes, and skills, force the financial

manager to be creative.

S141 11.11 DIAGNOSIS AND DECISION

(continued)

(c) Diagnosis helps the financial manager to distinguish

short term from long term problems.

(d) Ensure that short term financial policies arc

consistent with long term goals.

(e) Provide for both short term and long term financial

health at appropriate risk levels.

S142 11.11 DIAGNOSIS AND DECISION

(continued)

(f)

Manage the working capital ............ or it will manage

itself - very badly!

(g) Seek all (seven) alternatives before setting financial

policies.

S143 11.11 DIAGNOSIS AND DECISION (continued)

NOTE:

Past attitudes may deter new financial policies for reducing

assets or using increasing NEW sources of finance.

S144 11.12 LEARNING PATTERNS - REVIEW

1. FINANCIAL MANAGEMENT

S, G, F & I ........... CASH FLOW .......... EVA/SVA

S145 11.12 LEARNING PATTERNS - REVIEW

(continued)

2. COST OF CAPITAL

AVERAGE COST OF EQUITY AND DEBT

(LIABILITIES)

HURDLE RATE FOR EVA

S146 11.12 LEARNING PATTERNS - REVIEW

(continued)

3. OPERATING CASH FLOW

PROVIDES CASH FOR:

WC & “NORMAL” CAPITAL INVESTMENT

AND NEW PROFITABLE INVESTMENT

OPPORTUNITIES FOR EVA

INCREASED WC IS AN INVESTMENT!

S147 11.13 INSTRUCTIONS (20 minutes)

Reassemble in SG

Review the Summary Lecture for Part I in the course

diary and discuss questions arising

To get the best out of Part II of the program, try to

complete ALL of the following ... homework tonight ...

S148 11.13 INSTRUCTIONS (continued) ...

homework tonight ...

Read the articles on finance

In the ASS text, review the chapter summaries and the

glossary

Do the optional exercises in the course diary and check the

answers

Review the summary lecture for Part I in the course diary

Review your notes for Part I of the course and list outstanding

questions to be resolved in Part II

S149

S20111.13

AUTOMATED

INSTRUCTIONS

GROUP(continued)

LEARNING

Final Note

(AGL)

for Part I ...

AGL NO.

Thank

you 10

for- working so hard

today

....

FINANCIAL MANAGEMENT

Tomorrow .... it’s downhill all the

OF

WORKING

CAPITAL

way ....

DAILY WORK PACK - PART 2

Copyright: RGAB/PW 2005/3

AGL