visual #8-1

advertisement

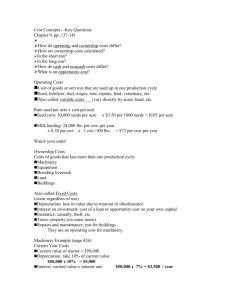

Chapter 08 - Accounting for Long-Term Assets VISUAL #8-1 FORMULAS FOR DEPRECIATION METHODS 1. STRAIGHT LINE Cost - Estimated salvage Estimated useful life = Annual Depreciation 2. UNITS OF PRODUCTION a) b) (Depreciable) Cost - Estimated salvage Cost per = Predicted units of production Unit CPU x units produced in period = Depreciation for PERIOD (In last year, depreciate to estimated salvage value; never depreciate below this amount.) 3. DOUBLE-DECLINING BALANCE Book Value (beginning of year) x RATE* = Depreciation (for that year) *RATE The rate used is constant and it is twice what the straight line rate would have been for this asset. (In the last year, depreciate to estimated salvage value; never depreciate below this amount.) 8-1 Chapter 08 - Accounting for Long-Term Assets Chapter Eight – Alternate Demonstration Problem #1 The New Times Company purchased a new machine on January 1, 2009. The new machine cost $120,000, had an estimated useful life of five years, and an estimated salvage value of $15,000 at the end of its useful life. It was expected that the machine would produce 210,000 widgets during its useful life. The company used the machine for exactly three years. During these three years, the annual production of widgets was 80,000, 50,000, and 30,000 units, respectively. On January 1, 2013, the machine is sold for $45,000. Required: 1. Calculate the depreciation expense for each of the first three years using: a. Straight-line b. Units-of-production c. Double-declining-balance 2. Prepare the proper journal entry for the sale of the machine under each of the three different depreciation methods. Solution: Chapter Eight – Alternate Demonstration Problem #1 1a. Straight-line: The depreciation expense each year is equal to cost minus salvage value divided by useful life. In this example the cost is $120,000, the salvage value is $15,000, and the useful life is 5 years. Therefore, the annual depreciation expense would equal: (120,000 - 15,000) ÷ 5 = $21,000 per year 8-2 Chapter 08 - Accounting for Long-Term Assets 1b. Units-of-production: The depreciation expense each year is equal to a rate [(cost minus salvage) divided by total production] multiplied by the actual number of units produced that year. In this example, the rate would be $0.50 per widget, (120,000 ÷ 15,000) ÷ 210,000, and the depreciation expense for each of the first three years would be: Year 1 Year 2 Year 3 1c. .50 .50 .50 x x x 80,000 50,000 30,000 = 40,000 = 25,000 = 15,000 Double-declining balance: The depreciation expense each year is equal to a rate (twice the straight-line rate divided by useful life) multiplied by the asset’s net book value (cost minus accumulated depreciation) at the beginning of the year. In this example the rate would be 2/5, or 40%, and the depreciation expense for each of the first three years would be: Year 1 Year 2 Year 3 = = = .40 x .40 x .40 x 120,000 (x) = 72,000 (1) = 43,200 (2) = Book value at beginning of year: (1) 120,000 – 48,000 = 72,000 (2) 120,000 – 48,000 – 28,800 = 43,200 8-3 48,000 28,800 17,280 Chapter 08 - Accounting for Long-Term Assets Solution: Chapter Eight – Alternate Demonstration Problem #1, continued 2. The journal entry for the sale of the asset will have the same general form regardless of the method of depreciation adopted, except that whether there is a gain or a loss on the sale may change according to the depreciation method used. The gain or loss on disposal of the asset is determined by comparing the sale price, in this case $45,000, with the net book value of the asset at the time of the sale. Straight-line: Cash .......................................... Accumulated depreciation ..... Loss on sale of machine ......... Machine .............................. 45,000 63,000 12,000 120,000 Units-of-production: Cash .......................................... Accumulated depreciation (40,000 + 25,000 + 15,000) ...... Machine .............................. Gain on sale of machine ... 45,000 80,000 120,000 5,000 Double-declining balance: Cash .......................................... Accumulated depreciation (48,000 + 28,800 + 17,280) ...... Machine .............................. Gain on sale of machine ... 45,000 94,080 120,000 19,080 8-4

![Quiz chpt 10 11 Fall 2009[1]](http://s3.studylib.net/store/data/005849483_1-1498b7684848d5ceeaf2be2a433c27bf-300x300.png)