Solutions Guide: This is meant as a solutions guide

advertisement

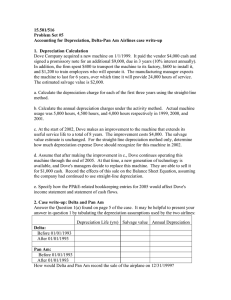

Solutions Guide: This is meant as a solutions guide. Please try reworking the questions and reword the answers to essay type parts so as to guarantee that your answer is an original. Do not submit as your own. (Depreciation Computation-Replacement, Nonmonetary Exchange) Goldman Corporation bought a machine on June 1, 2008, for $31,800, f.o.b. the place of manufacture. Freight to the point where it was set up was $200, and $500 was expected to install it. The machines useful life was estimated at 10 years, with a salvage value of $2,500. On June 1, 2009, an essential part of the machine is replaced, at a cost of $2,700, with one designed to reduce the cost of operating the machine. The cost of the old part and related depreciation cannot be determined with any accuracy. On June 1, 2012, the company buys a new machine of greater capacity for $35,000, delivered, trading in the old machine which has a fair market value and trade-in allowance of $20,000. To prepare the old machine for removal from the plant cost $75, and expenditures to install the new one were $1,500. It is estimated that the new machine has a useful life of 10 years, with a salvage value of $4,000 at the end of the time. The exchange has commercial substance. Assuming that depreciation is to be computed on the straight-line basis, compute the annual depreciation on the new equipment that should be provided for the fiscal year beginning June 1, 2012. Old Machine June 1, 2008 Purchase......................................................... Freight ............................................................ Installation ..................................................... Total cost............................................ $31,800 200 500 $32,500 Annual depreciation charge: ($32,500 – $2,500) ÷ 10 = $3,000 On June 1, 2009, debit the old machine for $2,700; the revised total cost is $35,200 ($32,500 + $2,700); thus the revised annual depreciation charge is: ($35,200 – $2,500 – $3,000) ÷ 9 = $3,300. Book value, old machine, June 1, 2012: [$35,200 – $3,000 – ($3,300 X 3)] = .......................................................... Fair value ...................................................................................................... Loss on exchange ......................................................................................... Cost of removal ............................................................................................ $22,300 (20,000) 2,300 75 Total loss ........................................................................................... New Machine Basis of new machine Cash paid ($35,000 – $20,000) Fair value of old machine Installation cost Total cost of new machine Depreciation for the year beginning June 1, 2012 = ($36,500 – $4,000) ÷ 10 = $3,250. $ 2,375 $15,000 20,000 1,500 $36,500