Project Cost Management

advertisement

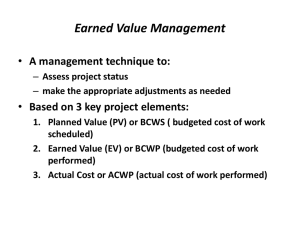

Project Cost Management Mohammad A. Rob The Importance of Project Cost Management IT projects have a poor track record for meeting cost goals 1995 CHAOS Report: – Average cost overrun was 189% of the original estimates – In 1995, cancelled IT projects cost the U.S. over $81 billion Cost of Software Defects When Defect is Detected User Requirements Coding/Unit Testing System Testing Acceptance Testing After Implementation Typical Cost of Correction $100-$1,000 $1,000 or more $7,000 - $8,000 $1,000 - $100,000 Up to millions of dollars It is important to spend money up-front on IT projects to avoid spending a lot more later. What is Project Cost Management? Project cost management is primarily concerned with the cost of the resources needed to complete project activities It includes several processes that ensure that the project is completed within an approved budget In most cases, predicting the financial performance of the project’s product (return on investment, cash flow, payback analysis) is done outside the project. Project Cost Management Processes Resource planning: determining what resources (people, equipment, materials) and quantities of them should be used Cost estimating: developing an estimate of the costs and resources needed to complete a project Cost budgeting: allocating the overall cost estimate to individual work items to establish a baseline for measuring performance Cost control: controlling changes to the project budget Project Cost Management Processes Basic Principles of Cost Management Benefits and costs can be tangible or intangible, direct or indirect – Tangible cost and benefits can easily be measured in dollars – Direct cost and benefits can be traced back (salary/salary savings, hardware/software cost) Sunk cost is money that has been spent in the past Life cycle cost means the cost of a project over its entire life (development + operation) Cash flow analysis is a method of determining the estimated annual costs and benefits for a project and the resulting cash flow 1. Resource Planning Resource planning involves determining: – what physical resources (people, equipment, materials) are needed – what quantities of each should be used, and – when they would be needed to perform project activities The nature of the project (construction, automobile, retail) and the organizational knowledge will affect resource planning 1. Resource Planning The inputs to the resource planning are: work breakdown structure, scope statement, historical information, and policies Expert judgment is the real tool for resource planning The main output is a list of resource requirement including people, equipment, and materials 2. Cost Estimating Cost estimating involves developing an approximation (estimate) of the costs of the resources needed to complete project activities The inputs to the cost estimating are: – WBS (list of task), resource requirement (type of resources for each task) and resource rate (cost per hour/item). 2. Cost Estimating There are several types of cost estimates: – Rough order of magnitude: It provides a rough idea of what a project will cost – Budgetary: It is used to allocate money into an organizational budget well ahead of time – Definitive: It provides an accurate estimate of project cost. (Most accurate) Types of Cost Estimates Type of Estimate Rough Order of Magnitude (ROM) Budgetary Definitive When Done Why Done How Accurate Very early in the project life cycle, often 3–5 years before project completion Early, 1–2 years out Provides rough ballpark of cost for selection decisions –25%, +75% Puts dollars in the budget plans –10%, +25% Later in the project, < 1 year out Provides details for purchases, estimate actual costs –5%, +10% Cost Estimation Techniques There are three basic techniques of cost estimation: – Analogous or top-down – Bottom-up – Parametric modeling Cost Estimation Techniques Analogous or top-down – Use the actual cost of a previous, similar project as the basis for the new estimate. – It is based on expert judgment and hence less accurate. – It is reliable for similar projects Cost Estimation Techniques Bottom-up – Estimate individual work items and summing them to get a total estimate. – If a detailed WBS is available, then cost can be estimated from the bottom of the WBS for each individual and then these estimates can be added in the higher-level WBS to get a total project estimate. – It is more accurate as individual items are considered – This method requires time and hence becomes expensive to develop Cost Estimation Techniques Parametric modeling – It uses project characteristics (parameters) in a mathematical model to estimate costs – Once popular parametric model is the Constructive Cost Model (COCOMO), which is used for estimating software development cost based on parameters such as the source lines of code or function points – Function points are technology-independent assessments of the functions involved in developing a system. For example, number of inputs and outputs, number of files/tables, number of processes – Barry Boehm helped develop the COCOMO models Cost Estimation Example Business Systems Replacement Project Category Objective Scope Assumptions Description Install a suite of packaged financial applications software which will enable more timely information for management decision-making, easier access to data by the ultimate end user, and allow for cost savings through productivity improvements throughout the company. The core financial systems will be replaced by Oracle financial applications. These systems include: General Ledger Fixed Assets Ops Report [AU: spell out Ops] Accounts Payable Accounts Receivable Project Accounting Project Management Oracle's software provides Cost/Benefit Analysis & Internal Rate of Return (IRR) Minimal customization No change in procurement systems during accounts payable implementation BSR was broken down into a three-year cash outlay without depreciation. Costs are represented in thousands. Capital and expenses are combined in this example. Cost Estimation Example Business Systems Replacement: Cash Flow Analysis Costs Oracle/PM Software (List Price) 60% Discount Oracle Credits Net Cash for Software Software Maintenance Hardware & Maintenance Consulting &Training Tax & Acquisition Total Purchased Costs Information Services & Technology (IS&T) Finance/Other Staff Total Costs FY95 FY96 FY97 ($000) ($000) ($000) 992 8 Year Internal Rate of Return Future Annual Costs/Savings ($000) 0 1492 0 250 270 0 50 570 0 (595) (397) 0 0 0 205 0 205 500 0 500 90 270 320 150 1330 1850 250 270 0 80 600 1200 (595) (397) 500 340 540 525 230 2135 3550 200 905 990 4170 580 2380 1770 7455 570 (101) (160) (88) 0 (349) (483) (1160) (384) (25) (2052) (584) (1320) (472) (25) (2401) (597) (2320) (800) (103) (3820) 3821 328 5054 (3250) Savings Mainframe Finance/Asset/PM IS&T Support/Data Entry Interest Total Savings Net Cost (Savings) 500 3 Year Total ($000) 905 35% 3. Cost Budgeting Cost budget involves allocating the project cost estimate to individual work items or work packages and providing a cost baseline The inputs are: – WBS: The work items are based on the project work breakdown structure – The project schedule is also required when cost is allocated over time Cost Budgeting Example For example, in the previous example of the Business Systems Replacement project, there was a total estimate of $1.8 Million for FY97: – Purchased cost: $600,000 – Information Services and Technology: $1.2 million Next we need to allocate the cost estimate to individual work items. Business Systems Replacement Project: $1.8 M Budget Estimates for FY97 and Explanations Budget Category Headcount (FTE) Cost Allocation to Individual Items Compensation Consultant/Purchased Services Travel Depreciation Rents/Leases Other Supplies and Expenses Total Costs Estimated Costs Explanation 13 Included are 9 programmer/analysts, 2 database analysts, 2 infrastructure technicians. $1,008,500 Calculated by employee change notices (ECNs) and assumed a 4% pay increase in June. Overload support was planned at $10,000. $424,500 Expected consulting needs in support of the Project Accounting and Cascade implementation efforts; maintenance expenses associated with the HewlettPackard (HP) computing platforms; maintenance expenses associated with the software purchased in support of the BSR project. $25,000 Incidental travel expenses incurred in support of the BSR project, most associated with attendance of user conferences and off-site training. $91,000 Included is the per head share of workstation depreciation, the Cascade HP platform depreciation, and the depreciation expense associated with capitalized software purchases. $98,000 Expenses associated with the Mach1 computing platforms. $153,000 Incidental expenses associated with things such as training, reward and recognition, long distance phone charges, miscellaneous office supplies. $1,800,000 4. Cost Control Project cost control includes: – monitoring cost performance – ensuring that only appropriate project changes are included in a revised cost baseline – informing project stakeholders of authorized changes to the project that will affect costs Earned value analysis is an important tool for cost control Earned Value Analysis (EVA) EVA is a project performance measurement technique that integrates scope, time, and cost data Given a baseline (original plan plus approved changes), one can determine how well the project is meeting its goals One must enter actual information (percent of work completed, how much it was cost) periodically to use EVA. Earned Value Analysis Terms Planned Value (PV): – Also called budgeted cost of work scheduled (BCWS) or budget, is that portion of the approved total cost estimate planned to be spent on an activity during a given period Actual cost (AC): – Also called actual cost of work performed (ACWP), is the total direct and indirect costs incurred in accomplishing work on an activity during a given period Earned Value (EV): – Also called budgeted cost of work performed (BCWP), is the percentage of work actually completed multiplied by the planned value (PA): EV = PV * Percent of Work Completed Earned Value Analysis Terms Cost Variance (CV): – It is the difference between the estimated cost of an activity and the actual cost of that activity (CV = EV - AC). – If cost variance is negative, it means that performing the work cost more than planned – If it is positive, it means that performing the work cost less than planned Schedule Variance (SV): – It is the difference between the scheduled completion of an activity and the actual completion of that activity (SV = EV - PV) – A negative schedule variance means that it took longer than planned to perform the work – A positive SV means that it took less time than planned to perform the work Earned Value Analysis Terms Cost Performance Index (CPI): – It is the ratio of earned value to actual cost (CPI = EV/AC) – It can be used to estimate the project cost of completing the project – If CPI is one or 100%, the planned and actual costs are actual – If it is less than 100%, the project is over budget – If it is more than 100%, the project is under budget Schedule Performance Index (SPI): – It is the ratio of earned value to planned value (SP = EV/PV) – It can be used to estimate the projected time to complete the project – An SPI of 1 means the project is on schedule, less than one mean behind the schedule, and more than one means ahead of schedule Earned Value Calculations for One Activity After Week One EV Activity PV AC Week 1 Week 2 Purchase web server 10,000 0 10,000 Weekly Plan (BCWS) Weekly Actual (ACWP) Cost Variance (CV) Schedule Variance (SV) Cost Performance Index (CPI) Schedule Performance Index (SPI) 10,000 15,000 -7,500 -2,500 50% 0 5,000 10,000 20,000 75% Total % Complete after Week 1 EarnedValue after Week 1 (BCWP) 75% 7,500 Earned Value Calculations for a One-Year Project After Five Months Earned Value Chart for Project After Five Months BAC 100,000 90,000 80,000 70,000 BCWS $ 60,000 50,000 ACWP 40,000 30,000 BWCP 20,000 10,000 1 2 3 4 5 6 7 8 9 10 Month BCWS or Cumulative Plan ACWP or Cumulative Actual BCWP or Cumulative EV 11 12