Importance of Project Cost Management

advertisement

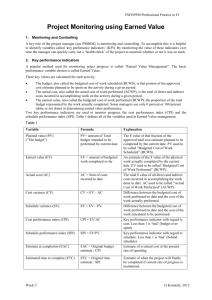

Project Cost Management Importance of Project Cost Management Cost management is a trouble spot for IT projects. According to the 1995 CHAOS study the average cost overrun on IT projects in the US was 89%, meaning that projects expected to cost $100,000 actually cost $189,000, and over 31% of IT projects were cancelled before completion, costing over $81 billion (yes, really!) In the 2001 study the cost overrun was 45% and most projects still went over their approved budget. Jim Johnson, “Chaos: the dollar drain of IT project failures” www.standishgroup.com/chaos.html (The IRS alone managed a series of project failures in the 1990’s that cost over $50 billion per year – as much as the annual net profit of the entire computer industry in a year.) It is usually not difficult for IT professionals to learn about project cost management; they just often are not interested in the subject. Many information technology professionals have a poor attitude toward project cost management because they have had bad experiences in the past, they think it is a job for accountants, and they have not been trained on creating and adhering to cost estimates. Most senior managers making IT project decisions know more about cost issues than they do about technology, and project managers need to learn to speak the language of cost management. Basic Principles of Cost Management Many people confuse profits and costs. Q Suppose you sell 10 widgets per day on average, and the average cost per widget is $10. If you sold 11 widgets one day, what would the affect on profits be? A There is not enough information to answer this question. You are given costs and asked to estimate profits. You do not know what the average profit is per widget. You might actually lose money by selling more widgets. Investment decisions for projects are usually based on projected life cycle costs and benefits. Project managers should have input into the budgeting process. An important part of a project manager's job is controlling project costs. Earned value management. Earned value analysis is a project performance technique that integrates scope, time, and cost data. It is the preferred method for measuring project performance because it includes all three dimensions of the triple constraint. It is not used more often because it is difficult to create a good baseline for cost, time, and scope estimates, and it is difficult to enter actual information (percentage of work complete and actual time and cost numbers) in a timely manner. There are many acronyms involved. These acronyms have changed from the PMBOK Guide – 1996 edition. Earned value used to be referred to as BCWP, but now it is EV. PV used to be BCWS, and AC used to be ACWP. Project 2000 still uses the 1996 acronyms. Even though this technique makes perfect sense, it is difficult to implement on most projects. The US government is a strong proponent of earned value management. Given a cost performance baseline, project managers and their teams can determine how well the project is meeting scope, time, and cost goals by entering actual information and then comparing it to the baseline. A baseline is the original project plan plus approved changes. Actual information includes whether or not a WBS (work breakdown structure) item was completed or approximately how much of the work was completed, when the work actually started and ended, and how much it actually cost to do the work that was completed. Earned value management involves calculating three values for each activity or summary activity from a project's WBS. The planned value (PV), formerly called the budgeted cost of work scheduled (BCWS), also called the budget, is that portion of the approved total cost estimate planned to be spent on an activity during a given period. Suppose a project included a summary activity of purchasing and installing a new Web server. Suppose further that according to the plan, it would take one week and cost a total of $10,000 for the labour hours, hardware, and software involved. The planned value (PV) for that activity that week is, therefore, $10,000. The actual cost (AC), formerly called the actual cost of work performed (ACWP), is the total direct and indirect costs incurred in accomplishing work on an activity during a given period. For example, suppose it actually took two weeks and cost $20,000 to purchase and install the new Web server. Assume that $15,000 of these actual costs was incurred during week 1 and $5,000 was incurred during week 2. These amounts are the actual cost (AC) for the activity each week. TERM FORMULA Earned Value EV = PV to date * percent complete Cost Variance CV = EV - AC Schedule Variance SV = EV - PV Cost Performance index CPI = EV/AC Schedule Performance index SPI = EV/PV Cost variance (CV) is the earned value minus the actual cost. In other words, cost variance shows the difference between the estimated cost of an activity and the actual cost of that activity. If cost variance is a negative number, it means that performing the work cost more than planned. If cost variance is a positive number, it means that performing the work cost less than planned. Schedule variance (SV) is the earned value minus the planned value. Schedule variance shows the difference between the scheduled completion of an activity and the actual completion of that activity. A negative schedule variance means that it took longer than planned to perform the work, and a positive schedule variance means that it took less time than planned to perform the work. The cost performance index (CPI) is the ratio of earned value to actual cost and can be used to estimate the projected cost of completing the project. If the cost performance index is equal to one or 100 percent, then the planned and actual costs are equal, or the costs are exactly as budgeted. If the cost performance index is less than one or less than 100 percent, the project is over budget. If the cost performance index is greater than one or more than 100 percent, the project is under budget. The schedule performance index (SPI) is the ratio of earned value to planned value and can be used to estimate the projected time to complete the project. Similar to the cost performance index, a schedule performance index of one or 100 percent means the project is on schedule. If the schedule performance index is greater than one or 100 percent, then the project is ahead of schedule. If less than 1 or 100%, the project is behind schedule. There are some general rules of thumb for deciding if cost variance, schedule variance, cost performance index, and schedule performance index numbers are good or bad. Negative variance numbers are bad (e.g. a cost variance of -$1000 means it cost more than planned.) A performance index below 100 percent is bad. (e.g. a schedule performance index of 80 percent means the project or activity is behind schedule. Viewing earned value information in chart form helps you to visualize how the project is performing. Senior managers overseeing multiple projects often like to see performance information in a graphical form. Earned value charts allow you to quickly see how projects are performing. If there are serious cost and schedule performance problems, senior management may decide to terminate projects or take other corrective action. The estimates at completion are important inputs to budget decisions, especially if total funds are limited. Earned value management is an important technique because, when used effectively, it helps senior management and project managers evaluate progress and make sound management decisions. However, earned value management is not used on many projects outside of government agencies and their contractors. Two reasons earned value management is not used more widely are its focus on tracking actual performance versus planned performance and the importance of percentage completion data in making calculations. Many projects, particularly information technology projects, do not have good planning information, so tracking performance against a plan might produce misleading information. Several estimates are usually made on information technology projects, and keeping track of the most recent estimate and the actual costs associated with it could be cumbersome. In addition, estimating percentage completion of tasks might produce misleading information. What does it really mean to say that a task is 75 percent complete after three months? Such a statement is often not synonymous with saying the task will be finished in one more month or after spending an additional 25 percent of the planned budget. To make earned value management simpler to use, organizations can modify the level of detail and still reap the benefits of the technique. For example, you can use percentage completion data such as 0 percent for items not yet started, 50 percent for items in progress, and 100 percent for completed tasks. As long as the project is defined in enough detail, this simplified percentage completion data should provide enough summary information to allow managers to see how well a project is doing overall. You can get very accurate total project performance information using these simple percentage complete amounts. Earned value management/analysis is the primary method available for integrating performance, cost and schedule data. It can be a powerful tool for project managers to use in evaluating project performance. Example Given the following information for a one-year project, PV = $23,000 EV = $20,000 AC = $25,000 BAC = $120,000 … answer the following questions: (Recall that BCWS is the budgeted cost of work schedule, BCWP is the budgeted cost of work performed, ACWP is the actual cost of work performed, and BAC is the budget at completion.) What is the cost variance, schedule variance, cost performance index (CPI), and schedule performance index (SPI) for the project? ANSWER: Cost variance = EV-AC=$20,000 - $25,000 = -$5,000 Schedule variance = EV-PV=$20,000-$23,000=-$3,000 CPI=EV/AC=$20,000/$25,000 =80% or .8 SPI=EV/PV=$20,000/$23,000=87% or .87 How is the project doing? Is it ahead of schedule or behind schedule? Is it under budget or over budget? ANSWER: The project is over budget and behind schedule. Use the CPI to calculate the estimate at completion (EAC) for this project. Is the project performing better or worse than planned? ANSWER: EAC=BAC/CPI=$120,000/.8=$150,000 The project is performing worse than planned since the new estimate to complete it is $30,000 more than planned. Use the schedule performance index (SPI) to estimate how long it will take to finish this project? ANSWER: Estimated time to complete=12montsh/.87=13.8 months. The project is projected to take 1.8 months longer than planned. Using Software to Assist in Cost Management e.g. Project 2000 and Excel can help in preparing cost estimates, budgets, and earned value charts. Q Suppose you were asked to prepare a cost estimate for a project to purchase laptops for all Informatics staff at your college or university. How would you start? How long would it take you to prepare a good estimate? A You should first ask what type of estimate is required - rough order of magnitude, budgetary, or definitive. How you start and how long it would take depends on the answer. A rough order of magnitude estimate for providing new laptops for 100 people might be $250,000. A budgetary estimate would break down the estimate to include hardware, software, detailed assumptions (for example, if the estimate is just for the purchase cost or is for a 2 to 4 year project life), and so on. A definitive estimate would be much more detailed and accurate than a rough estimate or budgetary estimate and would include vendor quotes. Q Give an example of using each of the following techniques for creating a cost estimate: analogous, parametric, bottom-up, and computerized tools. A Answers will vary. Using the example of providing new laptops for 100 people, one possible response is as follows: Analogous estimate: You could research similar organizations that recently purchased about the same number and type of laptops. Parametric estimate: You could decide on key factors, such as the basic category of laptop required and other requirements, and estimate costs using those parameters. For example, you might estimate that the laptops would cost about $2,000 each and that another $500 per unit would be required for support costs. Bottom-up estimate: You could determine detailed hardware and software requirements, training, and support costs to create an estimate. Computerized tools: You could use a spreadsheet to help prepare a cost estimate.