Chapter 3

External Analysis:

Industry Structure, Competitive Forces, and Strategic Groups

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

3-2

Chapter Outline

3.1 The PESTEL Framework

3.2 Industry Structure and Firm Strategy: The Five Forces

Model

3.3 Changes over Time: Industry Dynamics

3.4 Explaining Performance Differences within the Same

Industry: Strategic Groups

3.5 Implications for the Strategist

3-3

ChapterCase 3

Courtesy of Tesla Motors

Tesla Motors and the U.S. Automotive Industry

With high entry barriers, the BIG THREE – GM, Ford,

and Chrysler – dominated the U.S. car market until the

1980s.

There have been no new recent entrants due to the

HIGH industry entry barriers.

Tesla Motors’ Model S received outstanding market

reception, and was awarded the 2013 MotorTrend Car

of the Year.

3-4

EXTERNAL ANALYSIS

MACRO

• PESTEL Framework

INDUSTRY ANALYSIS

• Five Forces Model

MICRO

COMPETITOR ANALYSIS

• Strategic Group Mapping

3-5

3.1 The PESTEL Framework

KEY CONCEPTS

Managers mitigate threats and exploit opportunities

by analyzing the external environmental forces.

Factors are interdependent.

Framework to scan, monitor, and evaluate important

external factors/trends impacting a firm in its quest

for competitive advantage.

3-6

Exhibit 3.1 The Firm Embedded in

Its External Environment

3-7

Strategy Highlight 3.1

How the Eurozone Crisis Is Hurting Companies

The EU (European Union) began its formation in the

early 1950s.

Today – The euro is the common currency used by 17

of the 27 EU member states.

2009 – Several European countries took on too much

debt and were unable to repay their credit obligations.

Strict austerity programs were enacted.

Banks tightened credit hampering firms worldwide.

3-8

3.2 Industry Structure and Firm

Strategy: The Five Forces Model

Industry

• A group of (incumbent) firms that face the same set of

suppliers and buyers

Industry Analysis

• Identifies the industry's profit potential

• Derive implications for a firm’s strategic position within an

industry

Strategic Position

• A firm’s ability to create value (V) for customers while

containing costs (C)

Competitive Advantage = a large value gap (V - C)

3-9

Strategy Highlight 3.2

The Five Forces in the Airline Services Industry

Low Entry Barriers

Powerful Suppliers

Powerful Buyers

Strong Substitute Threat

Intense Rivalry

RESULTS – Low overall industry profit potential, thus

an “unattractive” industry for investment.

3-10

INDUSTRY FORCES IMPACT FIRM PROFITABILITY

ATTRACTIVE INDUSTRY

Sustainable Competitive Advantage Easier

• High profit potential

• The weaker the five forces

UNATTRACTIVE INDUSTRY

Sustainable Competitive Advantage Harder

• Low profit potential

• The stronger the five forces

3-11

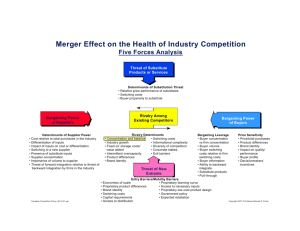

ANALYZING INDUSTRY STRUCTURE USING FIVE –

FORCES

Complementors

Number of complements

Relative value added

Barriers to complement entry

Engagement of complements

Buyer perception of

complements

Complement exclusivity

Supplier Power

• Supplier concentration

• Importance of volume to supplier

• Differentiation of inputs

• Impact of inputs on cost or

differentiation

• Switching costs of firms in the industry

• Presence of substitute inputs

• Threat of forward integration

• Cost relative to total purchases in

industry

Threat of New Entrants (and Entry

Barriers)

• Absolute cost advantages

• Proprietary learning curve

• Access to inputs

• Government policy

• Economies of scale

• Capital requirements

• Brand identity

• Switching costs

• Access to distribution

• Expected retaliation

• Proprietary products

Degree of Rivalry

• Exit barriers

• Industry concentration

• Fixed costs/value

added

• Industry growth

• Intermittent

overcapacity

• Product differences

• Switching costs

• Brand identity

• Diversity of rivals

• Corporate stakes

Threat of Substitutes

• Switching costs

• Buyer inclination to substitute

• Price-performance tradeoff of

substitutes

• Varity of substitutes

• Necessity of product or service

Industry value chain

– from raw materials

and other inputs, to

channel to end

consumer

Buyer Power (Channel and End

consumer)

• Bargaining leverage

• Buyer volume

• Buyer information

• Brand identity

• Price sensitivity

• Threat of backward integration

• Product differentiation

• Buyer concentration vs. industry

• Substitutes available

• Buyer’s incentives

12

The Threat of Entry

Incumbent firms can benefit from several important

sources of entry barriers:

•

•

•

•

•

•

•

Economies of scale

Network effects

Customer switching costs

Capital requirements

Advantages independent of size

Government policy

Credible threat of retaliation

3-13

Strength & Degree of Competitive

Rivalry

Exit barriers in the industry

Quantity and variability of strength in competitive

dynamics

Stage if the industry life-cycle

Industry fragmentation vs. consolidation

Perceptions of customer switching costs

3-14

The Power of Suppliers

POWERFUL SUPPLIERS

Can demand higher prices for their inputs.

Capture part (sometimes a large part) of the economic

value created.

-

Signs of Strong Suppliers

Suppliers industry is concentrated.

They don’t depend heavily on the incumbent’s industry.

Incumbent firms face high switching costs.

Suppliers’ products are differentiated.

Limited substitutes

Suppliers have credible forward integration threats.

3-15

The Power of Buyers

The bargaining power of buyers impacts industry profit potential.

POWERFUL BUYERS

Can demand a lower price or higher product quality

Reduce industry profit potential:

•

•

•

•

Through price discounts (limited revenue)

Through increased quality / better service (higher costs)

As they capture part of the economic value created

Credible threat of backwards integration

3-16

The Threat of Substitutes

This threat derives from products/services fulfilling the

needs of current customers from outside the industry.

POWERFUL SUBSTITUTES: THE POWER OF

SUBSTITUTES is HIGH when:

• Price-performance: Has an attractive trade-off

• The buyer’s switching cost is low

• Breadth/availability of substitute options

Substitutes limit the price that industry competitors can

charge for their products/services.

3-17

Exhibit 3.3

Industry Competitive Structures Along

The Continuum From Fragmented To Consolidated

3-18

Adding a Sixth Force:

The Strategic Role of Complements

COMPLEMENT

• A product, service, or competency that adds value when

used in tandem with the original product offering

Complementor – A firm that provides a good/service

that leads customers to value your firm’s offering

more when the two are combined

Co-opetition – Cooperation by competitors to

achieve a strategic objective

3-19

3.3 Changes over Time:

Industry Dynamics

The static five forces model cannot determine the

speed of change for an industry.

As consolidated industries tend to be more profitable

than fragmented ones, firms tend to change their

industry structures toward being more consolidated

through (horizontal) mergers and acquisitions.

Industry Profitability

Consolidation

3-20

Exhibit 3.5

Strategic Groups and the Mobility

Barriers in the U.S. Domestic Airline Industry

3-21

3.4 Explaining Performance Differences

Within the Same Industry: Strategic Groups

Firms in the same strategic group follow a similar

strategy.

Strategic group differences identify business-level

strategies.

Direct competitors – same strategic group firms.

Intra-group rivalry exceeds inter-group rivalry:

• Rivalry among firms within a strategic group is more intense

than the rivalry between strategic groups.

3-22

3.5 Implications for the Strategist

PESTEL analysis guiding consideration: How the

external factors identified affect the firm’s industry

environment

Porter’s five forces model identifies industry profit

potential and firm positioning for gaining and

sustaining competitive advantage.

Strategic group map helps to find performance

differences within the focal industry.

3-23

ChapterCase 3

Courtesy of Tesla Motors

Consider This…

• Recent dynamics in the automotive industry have lowered the

profit potential, reducing its attractiveness.

• Tesla Motors has demonstrated how new technology can be

used to circumvent entry barriers.

• However, incumbent firms are also introducing hybrid or allelectric cars, further increasing rivalry in the industry.

3-24

3-25