ppt version

advertisement

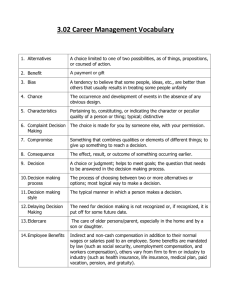

A drafting company employs 10 drafters at $800/week each. The CEO considers three alternatives: 1.Buy 8 low-end workstations at $2 000 each. Give two drafters 1 year’s notice. At the end of the year they each get $5 000 severance pay. Train the remaining eight in AutoCAD. The first training course is available in a year, and costs $2 000 per participant. After completing the course, each drafter gets a $100/week raise. 2.Buy 5 high-end workstations at $5 000 each. All the drafters get a year’s notice and $5 000 severance pay at the end of the year. Five new graduates are hired at $1 200 per week. They are trained in ProEngineer; to keep current, they will each need a $5 000 retraining session every six months. 3.Do nothing. A drafting company employs 10 drafters at $800/week each. The CEO considers three alternatives: 1.Buy 8 low-end workstations at $2 000 each. Give two drafters 1 year’s notice. At the end of the year they each get $5 000 severance pay. Train the remaining eight in AutoCAD. The first training course is available in a year, and costs $2 000 per participant. After completing the course, each drafter gets a $100/week raise. 2. Buy 5 high-end workstations at $5 000 each. All the drafters get a year’s notice and $5 000 severance pay at the end of the year. Five new graduates are hired at $1 200 per week. They are trained in Pro-Engineer; to keep current, they will need a $5 000 retraining session every six months. 3. Do nothing. Any of these options would allow the company to service its current customers. Any money saved can be invested at 10%, which is also the cost of borrowing money. What should they do? What time frame should we use? How do we represent `Do nothing’? Sketch the cash-flow diagrams. What non-monetary factors would matter? Option 1 $40,000 $16000 $16 000 $10 000 PW = -16,000 – (16,000+10,000)(P/F,0.1,1) + 40,000(P/A,0.1,N)(P/F,0.1,1) $40,000 P=F(P/F,i,1) $16 000 $10 000 PW = -16,000 - …. $40,000 26,000(P/F,i,1 ) PW = -16,000 – 26,000(P/F,i,1)… P’=40,000(P/A,i,4) P’ PW = -16,000 – 26,000(P/F,i,1) + … $40,000 P=F(P/F,i,1) P’=40,000(P/A,i,4) PW = -16,000 – 26,000(P/F,i,1) + … P=40,000(P/A,i,4)(P/F,i,1) PW = -16,000 – 26,000(P/F,i,1) + 40,000(P/A,i,4)(P/F,i,1) $100 000 Option 2 $25 000 $50 000 PW ($000) = - 25 – … $50,000 $100 000 P=F(P/F,i,1) $50 000 PW ($000) = - 25 – … $50,000 $100 000 $50,000 50,000(P/F,i,1 ) PW ($000) = - 25 – 50(P/F,i,1) $50 000 PW ($000) = - 25 – 50(P/F,i,1) + … P’=50,000(P/A,i,4) $50 000 PW ($000) = - 25 – 50(P/F,i,1) + … P=50,000(P/A,i,4)(P/F,i,1) PW ($000) = - 25 – 50(P/F,i,1) + … P=50,000(P/A,i,4)(P/F,i,1) PW ($000) = - 25 – 50(P/F,i,1) + 50 (P/A,i,4)(P/F,i,1) Some common variations on an annuity… 1. Your generous uncle gives you your age in dollars every birthday. 2. The cost of maintaining your car increases by $100 a month. There is one formula that fits both these cases: A = G(A/G,i,N) Take careful note of the starting time 3G 2G G 4G 3G 2G G A=G(A/G,i,N) A P=A(P/A,i,N) A 3. You get a regular salary and a $100 raise every year (or a $100 cut every year) We use the same formula, and add in your base salary: A = A/ + G(A/G,i,N) Sample problem: I get to choose between a job in industry with a starting salary of $50,000 and $5,000 raises every year. Or a job in academia where I get $70,000 right away, but never get a raise. If I can invest all my income at 5% interest, how long will it be before the present value of the industrial job exceeds the present value of the academic job? 4. You get a regular salary and a 10% raise every year (or a 10% cut every year) Too hard for Appendix A Define a growth-adjusted interest rate io: io = (1+i)/(1+g) - 1 Then (P/A, g, i, N) = (P/A, io, N)/(1+g) And if i = g, P =NA/(1+g) Sample problem: I get to choose between a job in industry with a starting salary of $50,000 and 5% raises every year Or a job in academia where I get $70,000 right away, but never get a raise. If I can invest all my income at 10% interest, how long will it be before the present value of the industrial job exceeds the present value of the academic job? 5. A generous but eccentric uncle gives you $1 000 every leap year Several alternatives to find present worth: a)Use (P/F, i, N) on each payment (tedious if there are a lot) b)Use j = (1+ i)4 – 1 to get a quadrennial interest rate, then use (P/A, j, N/4) c)Use (A/F, i, 4) to turn the first payment to an annuity, then use (P/A,i,N) Comparing projects based on Annual Worth If most of our cash flows are annual, it’s easier to convert one-time expenses to their annual equivalent. Also, you may want to know ``How much will I have to spend a week?’’ rather than ``What is the present worth of my annual salary?’’ Comparing projects on this basis will always give the same result as comparison based on present worth or future worth. Example A company wants to expand its capacity. It is considering two alternatives: 1.Construct a new building, at a cost of $2 000 000. Annual maintenance costs will be $10 000. The building will need to be painted every 15 years at a cost of $15 000. 2. Construct a smaller new building now, and another, smaller one in 10 years. The first building costs $1 250 000 to build and $5 000 a year to maintain. The addition will cost $1 000 000 to build, and once it’s built, the two buildings together will cost $11 000 to maintain. Fifteen years after the addition, and every fifteen years after that, the new buildings will be painted at a cost of $15 000. Assume an interest rate of 15%. Compare the annual cost of the two alternatives. Summary of comparison methods we know so far: Present worth Future worth Annual worth Still to come: Rate of return Cost/benefit Payback period Comparing Alternatives In comparing alternatives, any cost common to all the alternatives can be ignored. This will sometimes result in all the alternatives having negative present worth. Don’t worry – just choose the least negative. In many situations – for example, Question 2.5 – you will need to be careful to set up the comparison fairly. Study Period Part of setting up the comparison fairly is to choose the same study period for each alternative. For example: The Chopper lawnmower costs $100, requires $10 in fuel every year, and will last 4 years. The LawnBoy lawnmower costs $120, uses $15 in fuel every year, and lasts 6 years. If I expect to be cutting lawns for the rest of my life, which is the better buy? PW(Chopper) = -100 - 10(P/A, i, 4) PW(LawnBoy) = -120 - 15(P/A, i, 6) This is wrong! The Chopper lawnmower costs $100, requires $10 in fuel every year, and will last 4 years. The LawnBoy lawnmower costs $120, uses $15 in fuel every year, and lasts 6 years. If I expect to be cutting lawns for the rest of my life, which is the better buy? Either determine a salvage value: PW(Chopper) = -100 - 10(P/A, i, 4) PW(LawnBoy) = -120 - 15(P/A, i, 4) + S(P/F, i, 4) Or consider the lowest common multiple of lives: PW(Chopper) = -100 - 10(P/A, i, 12) – 100(P/F,i,4) – 100(P/F,i,8) PW(LawnBoy) = -120 - 15(P/A, i, 12) - 120(P/F, i, 6) Sets of Alternatives Alternatives may be independent, contingent, or exclusive Independent: Buying socks and buying a tie Contingent: Buying shoes and buying socks Exclusive: Buying a Lamborghini and buying a Ferrari In a complex situation, arrange the possibilities into mutually exclusive subsets and pick the best subset. Example: You can do A, B, C , D or E. If you do A, you can’t do B. To do D, you must do either B or C. If you do E, you must do A. You can’t do both B and C, and if you do D, you can’t do E. What are the possible subsets? Assignments These appear weekly at http://www.sfu.ca/~jones/ENSC201/index.html They are due on Thursdays, the first one on Thursday September 12. Majid will go through problems with slightly different numbers in the Wednesday tutorial sessions, starting next Wednesday Model answers will appear on the subsequent Friday. Only three of these assignments will contribute to your final grade; you’ll be warned of this in advance.