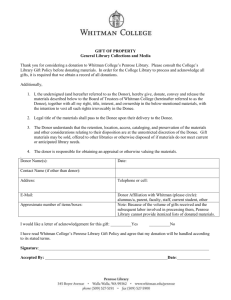

Gift Tax

Why

are gifts taxed?

o Gifts were made to avoid estate taxes

o Gifts were made to avoid income taxes

o Taxes in general are for social welfare

o Avoiding taxes through gifting reduced the

general welfare of the state (country)

Who

pays the gift tax?

o Usually it is the donor

o Can have arrangement where donee pays

Tax Rates on Gifts

o Exhibit 5.1 (page 135)

• Lowest rate 18% from $0 to $10,000 gift

• Marginal rate increases to 40% over $1,000,000

o Tax exclusions

• Annual exclusion now $14,000 per year per individual

• Lifetime exclusion currently $5,430,000 (federal)

• Tax credit is $2,117,800

• $345,800 for first $1,000,000 and 40% x $4,430,000

• No gift tax on charity gifts or to spouse (U.S. citizen)

o Rates now the same for estate, gift, and generation skipping

taxes but…Congress can always change rates…

Characteristics of a Gift

o Two parties involved, donor (giver) and donee (recipient)

o Voluntary transfer

o Less than full consideration

• Donor sells donee $1,000,000 worth of land to donee for $100,000

• Gift is the difference in FMV and consideration paid, $900,000

o Donor must be competent to make gift

o Donor must part with property (surrender all rights to property or

income from property)

o Donee must be capable of taking gift

o Donee must take delivery

o Donative intent present, donee must have conscious desire to make

the gift

Characteristics of a Gift (continued)

o Consideration

• Value transferred to Donor from Donor for the “gift”

• Consideration must be less than value of gift, otherwise just a sale

o Types of Gifts

• Direct gifts (direct payment of cash or property to donee)

• Indirect gift (payment of donee’s debt by donor, pay to third party)

• Indirect gift (property titled in donee’s name but purchased by donor)

o Complete or Incomplete Transfers

• Complete when donor releases all control

• Incomplete when donor has future recourse

• Gift to revocable trust

• Gift to revocable beneficiary

Interest Free Loan or Reduced Interest Loan

o Less than $10,000 – no gift tax

o Between $10,000 and $100,000 – no gift tax if “interest” would be

less than $1,000 per month

o Over $100,000 – gift is annual interest at difference between

Annual Federal Rate (AFR) and loan rate

Calculate the annual gift for the following loan:

o $250,000 principal

o AFR is currently 6%

o Loan rate is 2%

o Calculate annual payments under both, find annual interest, take

the difference and see if the loan is a partial gift…

Characteristics of a Gift (continued)

o Example of incomplete gift

• Donor sets up joint banking account

• Deposits funds in account

• Authorizes donee to make withdrawals

• Retains the rights to make withdrawals

• Gift becomes complete when donee withdraws funds

• Gift is complete because donee has taken delivery

• Amount of gift is the amount withdrawn

o Revisionary Interests

• Gift originally transferred to donee but reverts to donor in future

• Value of gift is present value of right to use property

• Revision interests determined by Treasury regulations

Characteristics of a Gift (continued)

o Net Gifts

• Normally the donor pays the gift tax but here the donee agrees to pay

the gift tax

• Donor must report taxable income for the gift tax that exceeds the

adjusted basis in the gift

• Example 5.11 page 141

•

•

•

•

•

•

Brianna gifts property worth $250,000 to Kenny

Kenny pays gift tax on receipt

Value of gift to Kenny is $250,000 – gift tax

Net Gift = $250,000 / (1 + 0.40) = $178,571

Assumes tax rate of 40%

Tax paid by donee is $250,000 - $178,517 = $71,429

• Issues for Financial Planner?

Exclusions and Exemptions

o Annual Exemption -- $14,000 from one individual to another

o Lifetime Exemption -- $5,430,000 Federal Exemption in 2015

o Non Citizen Spouses -- $145,000

o Split Gift (with spouse) -- $28,000 annual exemption

• Donor uses their $14,000 annual gift exemption and

• Spouse consents to use their annual gift exemption for same donee

• Form 709 is required of all split gifts and both spouses must sign

o For gifts from “community property” both spouses are deemed to

have donated the gift as they are 50/50 owners of the property

Deceased Spouse Unused Exemption Amount (DSUEA)

o A spouse can use the deceased’s exemption if transferred at death

Gifts of Present and Future Interests

Present Gifts are ones that transfer immediately and qualify at that time for annual

exclusion

o Future Gifts need a future event to take place before property transfers

o

• Usually gifts into revocable trusts are future gifts

• But if trust has mandatory income interests then…

Crummey Provision – explicit right of trust beneficiary to immediate withdrawal from trusts

for up to 30 days following contribution

o

o

o

Qualifies gift as present interest

Creates general power of appointment for estate tax purposes

Typically only the annual exemption amount can be withdrawn from trust

Five and Five Lapse Rule (can withdraw the maximum of five thousand dollars or five

percent of trust assets ) within 30 days

o Example 5.29, pages 154 -155

o Failure to withdraw by one of the three individuals distributes funds to all

beneficiaries (assumes other beneficiaries withdrew maximum amount of available

funds at contribution)

Transfers with No Gift Tax

o To Political Organizations

• Party Committee, Association, Fund, etc. for exempt purpose

• Exempt purpose to select, nominate, elect, or appoint individual to federal state

or local public office or in political organization

• Qualified Transfers

• Payments directly to educational institutions for tuition

• Payments directly to medical care provider

• Not part of annual exclusion or lifetime exclusion

• Payments for Support (i.e. child support, graduate school or

professional education, divorce payments)

• Business Settings

• Spouse (U.S. Citizen) unlimited, Non citizen spouse only $145,000

• Charities – Federal, State or Local and 501(c)(3) and 501(c)

Gift Tax Calculations – Over the years

o Lifetime exclusion now $5,430,000 (Federal Tax Only)

o Annual tax exclusion at $14,000 per individual donee

Example 5.33 – Pages 160 – 162

o Gift of $611,000 in 2005 (annual exclusion for 2006, $11,000)

o Gift of $712,000 in 2006 (annual exclusion for 2007, $12,000)

o Gift of $4,054,000 in 2014 (annual exclusion for 2014, $14,000)

Tax calculation for 2005 yields no gift tax

Tax calculation for 2006 yields gift tax of $124,000

Tax calculation for 2014 yield gift tax credit of $124,000

Overall gift tax for 2005 to 2014, $0

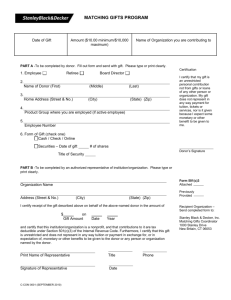

Income Tax Issues Related to Gifts – File Form 709 (page 163)

o Filed Annually if over annual exemption or lifetime exemption

• If donor cannot pay taxes, IRS may seek taxes from donee

o Adjusted Basis

• Donee’s basis is the donor’s basis and includes the donor’s holding period

• Gift just continues the asset from it’s original acquisition by the donor to the

donee

o Example of Adjusted Basis

• Donor gifts property purchased on in 1995 at $400,000 to child

• Current fair market value is $690,000

• Donee has basis of $400,000 but current holding period of 20 years

o Double Basis for Holding Period

• When FMV below adjusted donor’s basis use date of transfer if loss occurs

• If eventual gain on sale use the donor’s acquisition date for holding period

Gift Strategies (Client Goals)

o Gifts to Spouse – no taxed but

• Can provide additional tax breaks when spouse gifts the assets

• A-B By Pass Trust…

o Appreciated Gifts

• To Charities so that tax is avoided on the appreciated asset

• Charities do not pay taxes so it increases total cash flow

o Gifts to Minors

• Through a trust to minimize “bad” spending

• But administrator of trust can spend “badly” so appointment of

administrator also important

o Example 5.41 on Page 172 - 173

What are the implications for Financial Planning?

o Timing of gift? During life or as bequest?

o What property best for gifting?

o Tax law changes and planning for future gifting?

o Future gifting (to trusts)

o Changing beneficiaries of gifts over time

o Changing amount of gifts over time

o Other issues?

0

0